- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Don’t Make Taxpayers Bail Out Pension Plans

Reports are that America’s pension plans may be on the agenda as President Trump and the Congressional leadership work out an end-of-year deal to keep the government running beyond the two-week stopgap measure passed last week. It is yet unclear what such pension discussions might involve, but the financial stakes in this policy area are enormous. Massive underfunding currently threatens the solvency of workplace pension plans, in turn threatening pensioners with severe benefit cuts, employer sponsors with crushing obligations, and insolvency of the entire pension insurance system operated by the Pension Benefit Guaranty Corporation (PBGC).

There are no easy answers to the pension crisis, especially now that it has grown so vast. There is, however, one very bad answer to be avoided now and in the future: anything that would put taxpayers on the hook for an expensive bailout.

Background

The PBGC, a federally-chartered corporation, insures two types of defined-benefit (DB) pensions that some employers provide to their workers: respectively, single-employer and multiemployer pensions. These two different pension types are as their names imply. A single-employer plan is simply a pension provided by one company to its workers, for which the company assumes funding responsibilities. If that employer goes out of business, the plan is typically terminated and its assets and benefit payment obligations are both assumed by the PBGC.

Multiemployer plans are more complex. These are collectively bargained plans to which multiple employers contribute, so that a worker can remain covered by the plan if he/she changes jobs from one participating employer to another. The plan is run by a board of trustees consisting of representatives of both management and labor. Labor and management negotiate a rate at which participating employers will contribute to the plan, which the trustees then convert into a benefit structure they believe the contributions will be adequate to finance.

An important difference between single- and multiemployer plans is that if a multiemployer plan sponsor goes out of business, the plan doesn’t necessarily terminate. Instead, the remaining employers in the plan inherit responsibility for financing the benefits of the withdrawing sponsor’s workers (sometimes referred to as “orphan liabilities”). Thus, instead of the PBGC immediately taking the hit if a plan sponsor goes under, the other participating employers do. In effect, an employer’s pension promises are insured first by other sponsors in the same plan, while the PBGC provides backup insurance.

Other differences between plan types are important. For example, whenever PBGC takes over a pension plan, it pays benefits up to a statutory limit that is often far less than what the worker was previously promised. A worker in the terminated plan simply loses any benefits above these amounts. These limits are quite different between the single- and multiemployer sides and automatically change each year. For 2017, the largest single life annuity PGBC guarantees is just over $64,000 a year for someone retiring at 65 in a single-employer pension plan. Guarantee limits for multiemployer plans vary significantly with years of service but are far lower. For someone who has worked for 30 years under a multiemployer plan, the annual benefit guarantee might be a mere $12, 870.

Importantly, PBGC insurance is not taxpayer-financed. It is financed by premiums paid by participating employers (along with any assets of terminated plans that the PBGC takes over). Most Americans do not have the benefit of these DB pensions. The single-employer system has 30 million participants and the multiemployer system another 10 million. The benefits promised to these select workers were promised by specific employers, not by the federal government. Accordingly, those employers are responsible for financing the benefits as well as the premiums required to insure them. As it happens, the premiums assessed on employers under law are substantially lower than a private insurer would charge for PBGC’s insurance coverage, and are thus inadequate to keep the system afloat.

The Worsening Problem

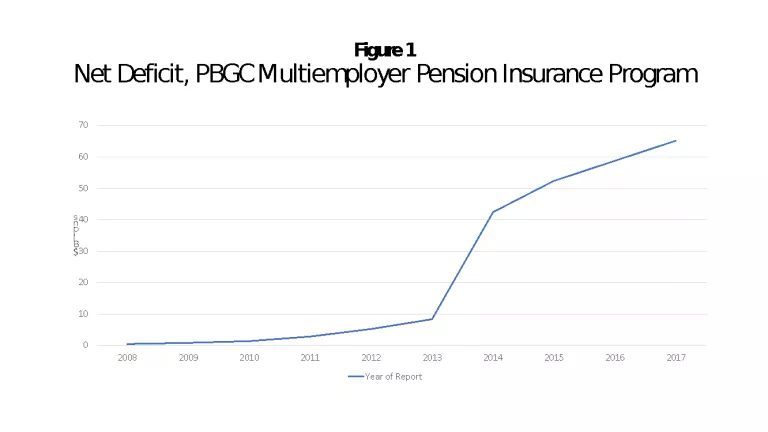

Both the single-employer and multiemployer insurance systems project a substantial deficit, meaning that each faces the threat of eventual insolvency. But the threat is far more dangerous and certain on the multiemployer side. The latest PBGC report projects a multiemployer program deficit of $65 billion – a stunningly bad number considering that it consists of $67 billion in projected liabilities against only $2 billion in assets. PBGC estimates the multiemployer insurance system will go under by 2025, with a substantial risk of insolvency before then.

Another important lesson of Figure 1 is that this is not a problem that will fix itself if the economy just gets a boost. While the great recession of 2007-09 took its toll on pension funding, the multiemployer program entered its current dire straits sometime between the 2013 and 2014 annual PBGC reports, largely due to two very large multiemployer plans entering probable termination status. Even a recently booming stock market has not put these plans on sound footing, and there is little realistic prospect of financial stabilization without substantial changes to both future pension payments and employer contribution requirements. As PBGC director Tom Reederrecently testified, these plans are in trouble because “the ratio of active to inactive (retired) participants is at its lowest point ever” (a situation that will only grow worse) and because many of these plans increased benefits during the 1990s market bubble, to levels that could not be sustained after subsequent market corrections.

Principles for Reform

At this point the problem is so severe that there are no clear answers, irrespective of one’s policy predispositions. The ideal outcome – that employers adequately fund the benefits they promise, and that they don’t promise benefits they can’t fund – is no longer easily enforced without causing many employers to dump their plans on the PBGC, thereby worsening the problem. Moreover, it’s not even clear what is fair. In the single-employer pension world it seems obvious that a company is ethically responsible for funding the pension promises it has made. But in the multiemployer world it’s typically the case that the employers facing the bill for orphaned pension liabilities are not the same ones who bailed on their pension obligations when they went out of business or otherwise withdrew from the plan. Someone will undeservingly be stuck with a substantial monetary loss no matter what we do. Nevertheless, certain principles can guide our policy responses.

Measurement accuracy: We cannot make informed policy choices without accurate reads on pension liabilities and net financial positions. This means that each plan’s projected benefit obligations should reflect up-to-date mortality tables and participant claiming behavior, and should be discounted using interest rates reflecting market conditions and the timespans over which benefits are to be paid. Under no circumstances should plans be allowed to assume away a large portion of their liabilities as many state and local pension plans have done to disastrous effect, by employing inflated discount rates reflecting their projected (i.e., hoped-for) investment returns rather than the rates economists would use to calculate their liabilities’ true present value.

Economists are virtually unanimous that discounting away pension liabilities is a corrupt practice of too many public pension plans. Unfortunately Congress also recently allowed private single-employer plans to use above-market discount rates to paper over the true sizes of their liabilities, a policy mistake that should not be repeated. It is one thing to knowingly give plan sponsors relief from their financing obligations. But this should never be done by pretending those liabilities don’t exist.

No taxpayer bailout: It would be both unfair and a damaging moral hazard to introduce the prospect of a taxpayer bailout of pension plans or pension plan insurance. Most taxpayers don’t have access to such pension benefits. These benefits were promised by employers, not by the federal government, only to certain workers. There would be no incentive for employers to honor obligations to fund their benefit promises once it becomes known that taxpayers are standing by to pick up the tab. Taxpayers should neither be made to pay for these pension benefits directly, nor should they be made to finance them with loans almost certain not to be repaid. It would specifically violate the ethic underlying PBGC insurance for taxpayers to subsidize any pension benefits in excess of PBGC’s statutory benefit guarantees, whether through direct grants or artificially-low-interest loans.

Protect the pension insurance system first: The critical near-term objective is to ensure that the PBGC insurance program doesn’t go under. Roughly 900,000 Americans are collecting their pension benefits via PBGC. Lawmakers should ensure PBGC remains able to perform this vital function. Note that it will be difficult enough to maintain the solvency of the PBGC insurance system; it would be several times more expensive (see Figure 2) to make all workers whole for the benefits they have been promised. Such a bailout of the multiemployer system would cost more than half a trillion dollars.

The benefits guaranteed by PBGC have deliberately been set in law to be substantially lower than the total pension benefits offered by employers. Hence, the chain of responsibility is that lawmakers are responsible for ensuring that the PBGC insurance program remains sound, while any obligations above and beyond those guarantees are solely the responsibility of sponsoring employers. The focus of lawmakers should be on ensuring the insurance system isn’t hit with liabilities it can’t cover.

Don’t dig the hole deeper: A multiemployer plan is in “critical” status if its funded percentage is below 65%. It is “critical and declining” if it is projected to be insolvent within the next 15 years. For such plans, no rapid fix is possible. It will require substantial additional contributions to repair such a plan’s funding status, which if made immediately could jeopardize the employer’s viability. Lawmakers must cautiously balance the goals of improving plan funding against avoiding near-term terminations that drop more plans onto the PBGC’s books.

The first rule when in such a hole is to stop digging. Legislation enacted in 2014 allows sponsors of “critical and declining” multiemployer plans to reduce benefits under certain specific circumstances. These reforms could be built upon to require benefit freezes, suspensions or reductions if a plan’s funding status dips low enough, similar to what was done for single-employer plans under the 2006 Pension Protection Act. Though benefit reductions would be painful for workers, outright plan termination would be substantially more painful for most, due to the low benefit levels guaranteed by PBGC in that scenario.

The goal is full funding; the key question is when. Ideally, plan funding rules would require that plans make steady progress towards full funding, with an eventual target of 100% funded status. But with average funding levels down around 40%, the contributions required to get plans moving toward full funding would be so onerous they would almost certainly induce sponsors to terminate their plans. On the other hand, funding requirements that are too lax or slow-acting will only lead plans to dump even larger liabilities on PBGC when they eventually terminate. Lawmakers should ask PBGC’s actuaries to estimate the contribution timetable that would minimize the insurance system’s projected exposure.

Be creative. Lawmakers and administrators alike will need to employ a wide array of tools to avert a crisis in the multiemployer system. The president’s latest budget puts forth ideas worthy of lawmakers’ serious consideration, including specific proposals “to create a variable-rate premium (VRP) and an exit premium.” The VRP would require higher premiums of sponsors of badly underfunded plans, a principle already applied in the single-employer system. This would give the insurance program additional revenue to stave off insolvency, while also improving funding incentives and protecting sponsors who have responsibly funded their plans. Under the proposal, PBGC would have the authority to waive the VRP if its application would increase the risk of a plan’s termination.

PBGC should also make creative use of its recently-established powers to facilitate both plan partitions as well as mergers, wherever doing so reduces exposure to the insurance system. One such partitionapproved this summer provides a potential model for future actions to combine limited financial assistance from PBGC with a substantial reduction in its potential liabilities. Lawmakers should further PBGC’s authority to facilitate such actions, providing that they split or combine plans in ways that lower the insurance system’s long-term deficit. And finally, lawmakers should consider enhancing plans’ standing to collect missed contributions in bankruptcy proceedings, though historically lawmakers have been reluctant to make significant changes in this area of law.

Underfunding in America’s multiemployer system is likely to threaten workers, taxpayers, employers, and the entire pension insurance system for the foreseeable future. A primary focus of lawmakers should be to ensure that the vital pension insurance system remains viable, and that taxpayers are not left holding the bag for benefits most of them are not eligible to receive.