- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Federal Budget Update: The Future Is Here, and It's Full of Red Ink

Those who fear to take steps that may rock the boat today shouldn't ignore that when a debt crisis occurs down the road, as we know it will, the size of the rocking will be exponentially bigger and meaner. So let's start to make changes today to avoid massive pains tomorrow.

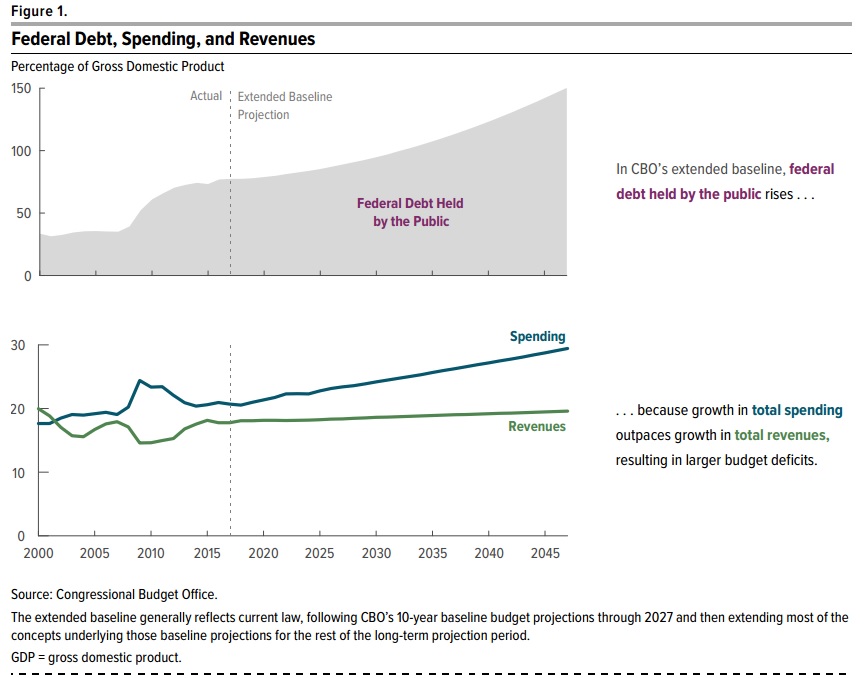

The Congressional Budget Office released an update to its long-term federal budget outlook on Thursday. As always, it shows that no matter how you look at it, the United States has already accumulated more debt and red ink than at any other time besides a major world war.

Our public debt stands at 77 percent of GDP, while our gross debt (the money the government owes to foreign and domestic investors as well as other accounts in the government) is well past 100 percent of GDP. Gross debt is about to breach the $20 trillion mark, a record that should worry those who believe in fiscal accountability.

CBO also shows that our debt problem, far from stabilizing, is getting worse very quickly. First, CBO projects that in 2047, our public debt will reach 150 percent under the current law. That's 5 percent higher than the CBO projected in January.

Let me repeat this: In the course of 3 months, our debt situation has deteriorated by 5 percent under what can be described as unrealistically favorable conditions. Imagine what a whole year or a decade could do to that number.

Importantly, CBO continues to make the case that 1) our growing debt levels are caused by continued and accelerating overspending (spending is projected to increase faster than revenue) and 2) in particular, overspending on mandatory spending: Social Security, the major healthcare programs, and net interest.

{kind=link}

Net interest is worth spending a little time on. According to the CBO, in the next 10 years alone, interest on the debt will go from $270 billion in 2017 to $768 billion 2027. And what do you get for that money? Nothing, because it's the actual price for the overspending done by the government.

As our deficit and debt grows, so will our interest payments. As a share of GDP, net interest will grow from 1.4 percent in 2047 to 6 percent in 2047. As this CBO chart shows, interests as a share of total spending will grow too.

{kind=link}

Finally, CBO has a chart that looks at what fiscal measures can be put in place to reduce the debt to GDP ratio in 2047 to its 50-year-average of 40 percent or to stabilize the debt at its current levels of 77 percent. It also looks at how much would be needed to either reduce or stabilize government debt.

<chart>

It shows that non-interest spending would have to be lowered by 3.1 percent of GDP or 15 percent and maintain it each year to put the nation on a good fiscal path of 40 percent debt-to-GDP ratio. Non-interest spending would have to be lowered by 1.9 percent of GDP or 9 percent and maintain it each year to stabilize the nation's debt-to-GDP ratio at 77 percent.

CBO argues that, alternatively, you could raise taxes by 3.1 percent of GDP or 17 percent and maintain it to get to a 40 percent debt-to-GDP ratio in 2047. Taxes would have to go up by 1.9 percent of GDP or 10 percent to maintain our debt at 77 percent all the way to 2047.

The revenue increase numbers are wishful thinking because there is no way the government can or even should try to raise that much revenue. Also, we have a spending problem and we should address it with spending cuts.

The bottom line is that doing nothing isn't an option, because we are heading toward a real debt crisis at some point. But more importantly, it is vital that we start addressing this issue now: the longer we wait, the bigger the adjustment needed to stabilize our debt will have to be.

This brings me to the debt ceiling. On March 16, the debt ceiling was reinstituted and it will have to be raised very soon. Congress never implements any fiscally-responsible measures unless it has no choice. The debt ceiling debate should be used responsibly to demand that some changes be made to our long-term trajectory.

We still have some time to make these arrangements. During the 2011 and 2013 debt ceiling debates, my colleague Jason Fichtner and I wrote a paper that explained that when government reaches the debt ceiling, the Treasury can no longer issue federal debt. It would still have ways to stage off a regrettable default while giving time for Congress to reach an agreement about the implementation of fundamental reforms that would get us on a more sustainable fiscal path.

At the time, we explained that the Treasury Department had several financial management options to continue paying the government's obligations including (1) prioritizing payments; (2) liquidating some assets to pay government bills; and (3) using the Social Security Trust Fund to continue paying Social Security benefits.

The previous administration denied these options were even available. But now they are recognized as acceptable procedures by Treasury, the Congressional Budget Office and the Federal Reserve of New York.

While we never advocated for any particular measures, we often lamented that this path had to be pursued because they are far from costless. However, we noted, and continue to argue today, that it was much more reasonable than defaulting on our debt or raising the debt ceiling without making any fundamental changes to the state of our finances.

Those who fear to take steps that may rock the boat today shouldn't ignore that when a debt crisis occurs down the road, as we know it will, the size of the rocking will be exponentially bigger and meaner. So let's start to make changes today to avoid massive pains tomorrow.

As I told Congress on Thursday, there is more than one way to tackle this problem.