- | Corporate Welfare Corporate Welfare

- | Expert Commentary Expert Commentary

- |

Government Privilege: Bailouts

[This is the fourth in a series of short commentaries on the Bridge that discusses the various types of privileges that governments bestow on particular businesses or industries.]

As the 10th anniversary of the historic bailout of 2008 looms, many people will undoubtedly say —as President Bush said at the time—that it was necessary to abandon “free market principles to save the free market system.” They will tell us that the government had no alternative. And they will say that the bailout “worked” because the economy didn’t go from a recession to a depression.

The truth is that there were alternatives. As our George Mason University colleague Garett Jones has written, a process known as “speed bankruptcy”—endorsed by economists on the left and the right—would have permitted quick conversion of bank debt into bank equity, recapitalizing the banks while avoiding the use of taxpayer funds.

We can’t be certain of what would have happened had something like speed bankruptcy been tried. But we do know that even with the bailout, the economy fell into the deepest and longest-lasting recession since the Great Depression. That is hardly proof positive that it “worked.”

Moreover, we know from the history of bailouts that the true cost of a bailout is not the taxpayer expense (which is often recouped) but the expectation it sets for future bailouts, an expectation that invites future disaster.

In 1971, the US government gave Lockheed Aircraft Corporation $250 million in emergency loan guarantees. It was the first time the federal government ever came to the rescue of a single firm. Shortly thereafter, the bankrupt Penn Central Railroad and other struggling railroads received hundreds of millions of dollars in emergency grants and loan guarantees. That was followed by $1.5 billion in loan guarantees for the ailing Chrysler Corporation in 1979.

The phrase “too big to fail” entered the American lexicon in the wake of a federal bailout of Continental Illinois Bank in 1984. Next, the federal government bailed out the creditors of hundreds of savings and loan (S&L) associations in the late 1980s and early 1990s at a cost to taxpayers of around $150 billion. In the late 1990s, the Fed orchestrated the private bailout of hedge fund Long-Term Capital Management. No taxpayer money was involved, but the Fed’s keen interest in the case led many industry observers to believe that the Fed would not let large institutions—or their creditors—fail.

The record-setting federal bailout of 2008-09 showed that these expectations were accurate. First, the New York Federal Reserve made a $30 billion loan to J. P. Morgan Chase so that it could purchase Bear Stearns. Next, in order to save them from bankruptcy, the federal government took over mortgage giants Fannie Mae and Freddie Mac. Then the government paused, allowing Lehman Brothers and its creditors to fall on September 15, 2008. Two days later, bailouts resumed and the Federal Reserve made an $85 billion loan to the insurance firm American International Group. The culmination of this series of bailouts was the Troubled Asset Relief Program (TARP), a $700 billion bailout that gave hundreds of financial firms and auto companies emergency government assistance.

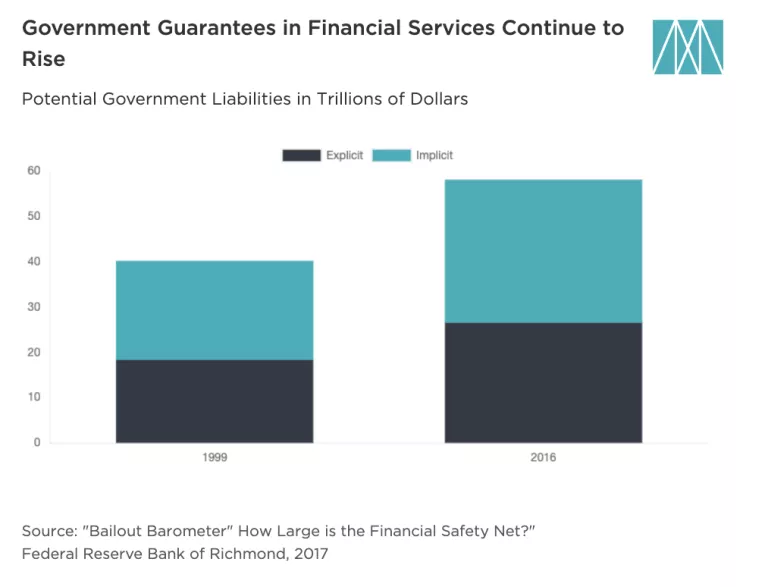

Although proponents of the Dodd-Frank financial reform legislation, passed after the 2008 meltdown, claimed it would help avoid future government bailouts, the perception that major financial interests are “too big to fail” remains an unfortunate reality. The Federal Reserve Bank of Richmond’s “Bailout Barometer” periodically estimates the extent to which the financial industry’s liabilities are explicitly and implicitly backed by the federal government. According to the most recent estimate, the share of financial sector liabilities subject to implicit or explicit government protection from losses grew from 45 percent in 1999 to 60 percent in 2016, by which time they amounted to $26 trillion. The authors succinctly note that “This protection may encourage risk-taking, making financial crises and bailouts more likely.”

Take, for example, Fannie Mae and Freddie Mac. Well before they were rescued by the federal government, Fannie and Freddie benefited from the expectation of government assistance. The firms were chartered by Congress and widely assumed to have its financial support. This assumption meant that compared with firms lacking support from the federal government, Fannie and Freddie appeared to be safer investments. As the Congressional Budget Office explains, this expectation, in turn, provided the companies a competitive advantage against private competitors:

"Because of their implicit federal guarantee, Fannie Mae and Freddie Mac could borrow to fund their portfolio holdings at much lower interest rates than those paid by fully private financial institutions that posed otherwise comparable risks, and investors valued the GSEs’ credit guarantees more highly than those issued by fully private guarantors ... The advantages of implicit federal support allowed Fannie Mae and Freddie Mac to grow rapidly and dominate the secondary market for the types of mortgages they were permitted to buy (known as conforming mortgages). In turn, the perception that the GSEs had become “too big to fail” reinforced the idea that they were federally protected."

The federal government’s history of bailing out creditors made this expectation especially strong.

Now that the summer of 2008 is a decade in the rearview mirror, we should be mindful that bailouts– and expectations thereof–encourage risky behavior, inviting crisis and further bailouts. Notwithstanding Mr. Bush’s assertion, one cannot save free enterprise by abandoning free enterprise. And free enterprise runs on market signals. Just as firms need profit signals to encourage good decision making, they need loss signals to discourage mistakes.

Unfortunately, just as the bailouts of the ‘70s, ‘80s, and ‘90s begat the massive bailouts of the 2000s, the likelihood of further–and perhaps even larger–bailouts in the future remains disconcertingly high.

Learn more: In The Pathology of Privilege: The Economic Consequences of Government Favoritism, Matthew D. Mitchell identifies multiple forms of government granted privilege (including tax privileges, contracting abuses, and trade privileges), and explains their consequences. The full special report is free of charge via pdf and is available as an ebook and paperback for purchase at Amazon.com.

Photo credit: Susan Walsh/AP/Shutterstock