- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

How Did Federal Surpluses Become Huge Deficits?

Non-partisan analysts agree that the federal government faces an enormous budget shortfall. This shortfall cannot be resolved unless we accurately diagnose its causes and devise solutions that address them.

Non-partisan analysts agree that the federal government faces an enormous budget shortfall. This shortfall cannot be resolved unless we accurately diagnose its causes and devise solutions that address them.

Discussions of federal deficits too often feature partisan blame-laying when what is needed is problem-solving analysis. To prevent a future fiscal meltdown, we must address the causes of unsustainable future deficits. On this question there is little disagreement among non-partisan scorekeepers. The Congressional Budget Office (CBO) projections show that future fiscal strains will be driven almost entirely by growth in federal entitlement spending, driven in turn by population aging and by the growth of federal health benefits per capita. Under current law, the projected problem is not one of insufficient taxes (which would grow to far exceed historical norms) or appropriated spending (which would shrink relative to the economy). Seriously addressing the long-term fiscal problem means restraining entitlement spending growth, plain and simple.

We spend a great deal of time, however, debating not the future of the budget but past policy choices. How is it that we have such large deficits already? The two parties debate this in part to establish their own relative credibility as future stewards of the nation’s finances. This debate also affects perceptions of which policies are thus far “at fault,” and thus of who can fairly be asked to sacrifice going forward.

This discussion often intensifies when it comes time to decide whether to continue a current policy, repeal it, or allow it to expire. Two prominent examples are current income tax rates (which many Democrats argue should rise via expiration), or the 2010 health reform law (which many Republicans argue to repeal). Even in this context, however, there’s a limit to how useful a debate about the past can be. Most of the 2010 health reform law’s costs, for example, haven’t yet begun to show up on the federal ledger. But the debate over the past will always continue. As long as it does we all have a stake in having an accurate picture of how things have played out so far.

One of the most common narratives about the federal budget is as follows: that back in the halcyon days of early 2001 we were facing large surpluses lasting as far as the eye could see, which by a series of policy blunders were transformed into the gargantuan deficits we see today. The two parties naturally blame one another for the fiscal deterioration. But objectively, what happened to turn those projected surpluses into huge deficits?

Thanks to a recent report from CBO, we now have a comprehensive, non-partisan answer to that question. I will walk through it step by step, using graphs to illustrate the CBO findings.

The order in which one does this can affect one’s impressions of the analysis. So first I will do it one way, then at the end of this piece I’ll show the reverse view. On the first run-through I’ll hold the 2001/03 tax reductions (the so-called “Bush tax cuts”) for last, to isolate their effects. I do this in deference to the rhetorical attention that this tax relief has received as a possible contributor to our current fiscal problem.

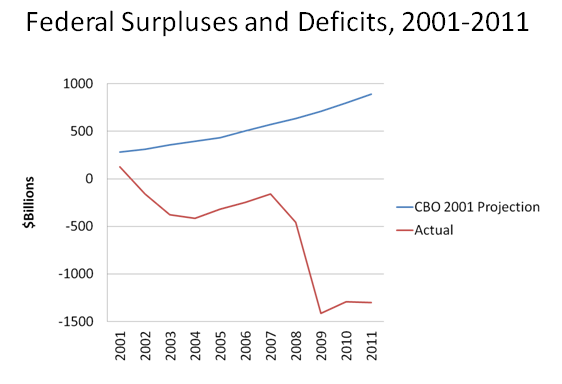

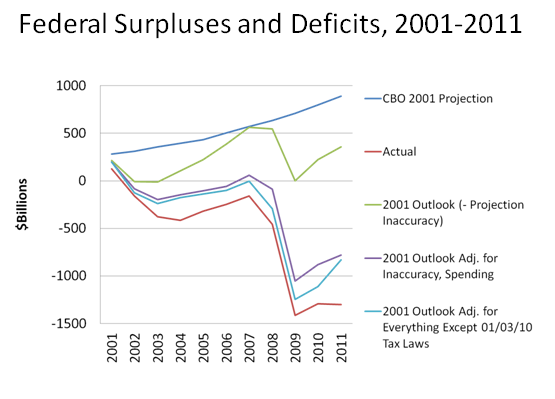

First, let’s compare the 2001 projections as a whole to what actually happened:

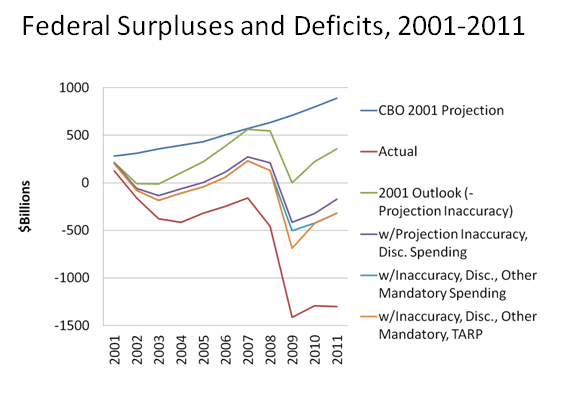

As shown above, in 2001 CBO was anticipating a total of $5.6 trillion in surpluses from 2001-11, including a surplus of nearly $900 billion in 2011 alone. Instead we ran $6.1 trillion in deficits, including deficits exceeding $1 trillion in each of 2009-11. This was a dramatic worsening of our fiscal outlook.

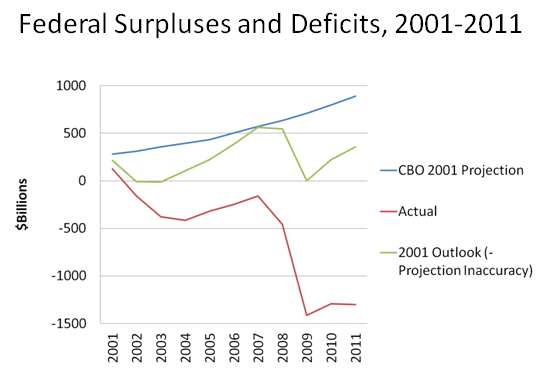

The first thing to understand is that, like most projections, the 2001 projections were simply wrong. CBO now identifies over $3.2 trillion in “economic and technical changes” in the subsequent projections, a polite way of saying “correcting for prior projection inaccuracy.” So even if there had been no tax relief or additional spending, a good portion of 2001’s projected surpluses would never have materialized. Had this then been known, the 2001 outlook would have looked like the green line in the following graph (in all of these graphs, for consistency, the bottom “actual” line will be kept red):

Forecasters in early 2001 failed to anticipate the bursting of the 1990s dot-com stock bubble, which by itself eliminated the surpluses projected for 2002 and 2003. The 2001 projections also contained other inaccuracies, and (understandably) failed to anticipate our most recent recession.

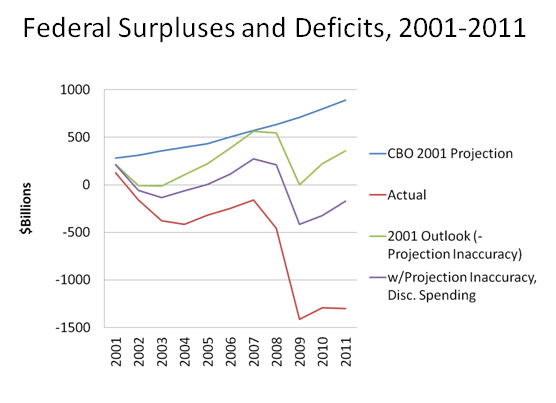

One major factor that worsened the fiscal outlook was a large increase in federal discretionary spending. Much of this, of course, happened after the United States was attacked on September 11, 2001. The U.S. thereafter conducted major military operations in Afghanistan and Iraq, and also increased expenditures on homeland security. These policies were enacted with bipartisan support, including bipartisan decisions to add their costs to the federal deficit. Discretionary spending increases further accelerated in 2009-11.

There were other spending increases as well, in mandatory spending. Three significant increases involved the Medicare prescription drug benefit, the TARP financial sector bailout, and the 2009 stimulus. First I’ll add the effects of all mandatory spending increases other than these three big-ticket items.

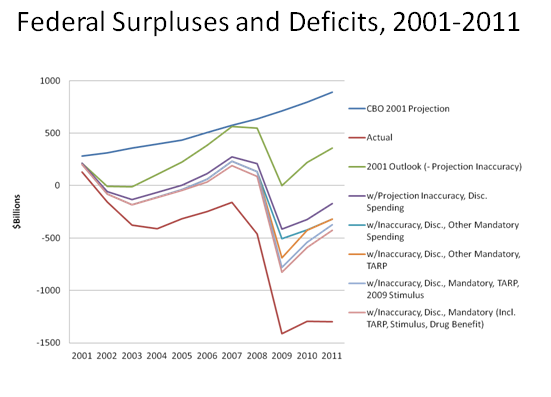

Now we’ll add in TARP (the financial sector bailout), which mostly just moves the 2009 number:

Next let’s include President Obama’s 2009 stimulus package, which added to the 09-11 deficits (see how the light blue line is below the orange line in 2009-11):

I’ve held the Medicare prescription drug benefit for last among the spending items because of the attention it has received as a contributor to deficits. Including it completes the changes in the outlook due to non-interest spending:

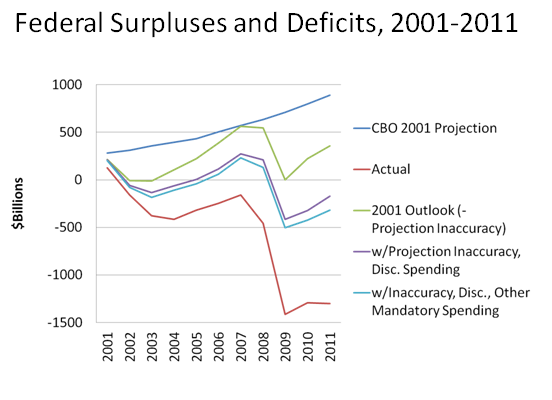

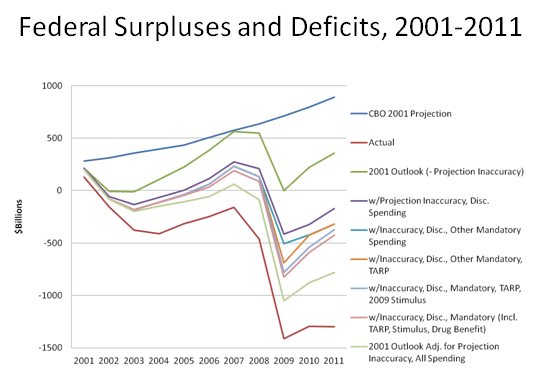

We have another spending component to add: interest on the debt. Though both spending and revenues affect the size of the debt, interest payments are classified as mandatory spending. Adding in its effects, we have thus incorporated all the subsequent worsening of the 2001 outlook arising from projection errors and additional federal spending:

That’s a lot of lines for one graph, so I’ll clean it up. The graph below summarizes all changes to the 2001 fiscal outlook arising from increased federal spending and correcting projection inaccuracy. Again, the red line at the bottom is what actually occurred, while the purple line just above it is where we would have been based on spending increases and projection corrections alone.

Let’s look a bit closer at this graph before moving on. A few critical points are clear. One is that the purple and red lines are qualitatively similar: that is, the vast majority of the deterioration in the fiscal outlook would have occurred even if there had been no tax relief in 2001 or 2003. This is first because the 2001 projections were quite wrong, and second because federal spending increases were more than sufficient to eliminate projected surpluses.

Let’s now look at the often-discussed effect of the 2001/03 tax relief laws, and of their extension in 2010, on the deficit. I’ll isolate the effect of the 01/03/10 laws by first incorporating the effects of all other tax legislation enacted since 2001 – including the 2004 working families relief act, the 2008 stimulus, and the tax portion of the 2009 stimulus. The result is below:

So, how much did the 2001/03 tax cuts contribute to our current budget predicament? The difference between the bottom two lines on the above graph represents the maximum possible answer. The bottom red line shows the deficits we’ve had. The light blue line just above it shows the deficits we would have had without the 2001, 2003 and 2010 tax relief laws. Clearly, the post-2001 fiscal deterioration had comparatively little to do with the 2001/03 tax cuts.

A few words of clarification on the difference between the bottom two lines on the above graph. The tax rates created in 2001 and 2003 were extended by another law in 2010. That law also contained other unrelated tax reductions, including a significant Social Security payroll tax cut. Thus even if one counts the 2010 extension as part of the “cost” of the 2001/03 tax cuts, the narrow difference between the bottom two lines above is actually somewhat larger than the 2001/03 tax relief’s total fiscal effects.

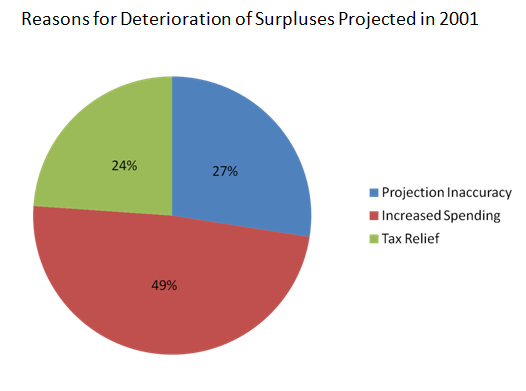

The CBO report allows us to sum the reasons that the surpluses projected in 2001 never transpired. The pie graph below summarizes CBO’s findings.

Roughly half of the reason the surpluses never materialized is that federal spending was subsequently increased (over half of this total increase was concentrated in the three years of 2009-11). A little over one-quarter disappeared because of subsequent corrections to the 2001 projections. Less than one-quarter was due to tax relief of any kind – and only a little more than half of that small fraction is directly attributable to the 2001 and 2003 tax relief packages.

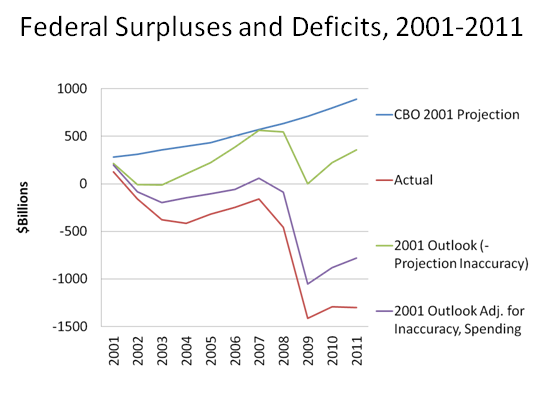

My goal in the above analysis has been to isolate the effects of the 2001/03 tax cuts by showing where we would have been without them. Now I’ll take exactly the opposite perspective. Let’s assume that only the 2001/03 tax cuts had been enacted, with no other changes in spending or in the underlying projections. Had that been the case, our budgetary situation would have looked like this:

As before, the red line on the bottom is what actually happened. The green line, rising nearly as rapidly as the blue one, shows the rising surpluses that would have occurred if tax relief had been the only change to the 2001 outlook.

There are thus two opposite ways we can look at the effect of the 2001/03 tax relief on our current fiscal situation:

- Had the tax relief never been enacted but everything else happened as it has, we still would face enormous deficits today.

- Had only the tax relief been enacted, we would still have enjoyed large and growing surpluses.

Various advocates have their own reasons for wanting the tax rates established in 2001 and 2003 to either be extended or to expire. But the CBO analysis should finally put to rest any misperception that tax cuts were the leading driver of our currently enormous budget deficits.