- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

- |

Jerome Powell, Trump's Nominee for Fed Chair, Will Have This Big Banking Issue to Tackle

President Trump nominated Jerome Powell as the new head of the Federal Reserve Board Thursday afternoon. Among the first big questions Powell should tackle is what to do about generous, essentially taxpayer-funded payments the Fed is making to banks.

In 2016, the Fed paid member banks $12 billion in interest earned on excess reserves it held for them. Member banks include virtually every bank you have ever heard of, as well as foreign banks that operate in the United States. Indeed, some 40 percent of the interest paid went to the latter — more than enough to make foreign bankers smile.

The Fed interest payments started in 2008, during the throes of the financial collapse and Great Recession. Prior to that, the Fed had never paid interest on excess reserves. More on that later.

Here’s the important thing to remember: If the Fed’s money faucet were closed, the funds sent to banks would go instead to the U.S. Treasury, and indirectly to U.S. taxpayers. Should Powell advocate ending this taxpayer-funded 100 percent sure thing for banks?

To address the question, we must look a bit closer.

To begin, member banks are required to place in reserve with the Fed a share of the checking and savings accounts they hold. This, after all, is the essence of reserve banking. Excess reserves are just what it sounds like — reserves that exceed what the Fed requires.

But why would a bank have excess reserves in the first place? Until 2008, banks generally held no excess reserves at all. After all, excess reserves form the basis for making loans. Loans generate interest, and that’s how banks make money.

But so do excess reserves held by the Fed.

In late 2016, the Fed held $1.9 trillion in excess reserves. Banks earned 0.5 percent on their balances, which was a 100 percent, guaranteed sure-thing. In December 2016 the rate was raised to 0.75 percent, in March 2017 to 1 percent, and in June 2017 to 1.25 percent — all still 100 percent guaranteed.

Fasten your seatbelt; this is getting interesting.

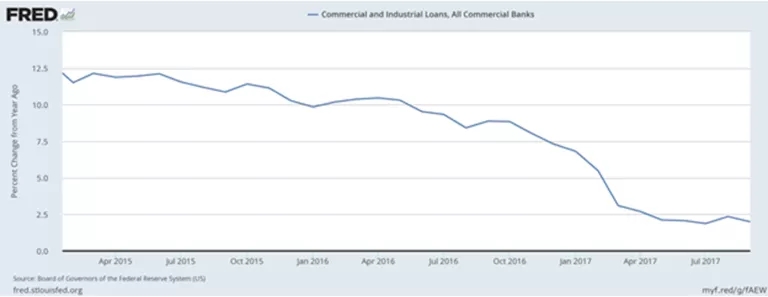

Of course, there is more going on here than just the interest rate story, but the evidence suggests that, at the margin, banks prefer a taxpayer-funded 100 percent sure thing to making risky loans.

But bank lending drives the economy.

Does this suggest Mr. Powell should advocate closing the Fed’s money spigot? Perhaps we need to know more. But it does suggest that Congress should investigate the matter, and the new Fed chairperson should urge a strong review.