- | Financial Markets Financial Markets

- | Expert Commentary Expert Commentary

- |

Let's Think Again about Dodd-Frank

[Dodd-Frank] covers so many complex issues that an improvement just isn’t going to be that simple, and yes, something did need to be done after 2008.

Six years after the U.S. Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act in response to the 2008 financial crisis, it is not obvious that it made the U.S. economy safer and sounder.

Take the slow recovery in the real estate market. Some of the weak housing demand is due to high student debt and slow rates of household formation, but tighter regulations on mortgage lending also have held it back.

Evidence of this comes in a recent paper by Francesco D’Acunto and Alberto G. Rossi at the University of Maryland Business School, who show that the lending regulations of Dodd-Frank redistributed credit away from the middle class toward wealthier Americans. After adjusting for economic conditions, mortgage credit to the middle class went down by 15 percent. It went up 21 percent for wealthy households. Mortgage credit also has been tight for poorer borrowers, in part through the deliberate intent of the law. It seems we shot ourselves in the foot by slowing down an already lagging economic recovery.

Looking at a broad swath of history, I see three major forces that can make financial systems safer: people being scared by recent events, solid economic growth and reduced debt in comparison to the value of equity. The financial crisis gave us the first on that list as perhaps its main “gift” (for now), but Dodd-Frank may have worsened economic growth problems.

On the plus side, we might like to think that Dodd-Frank improved the debt-equity balance by pushing banks to raise more capital. But that, too, now stands in doubt.

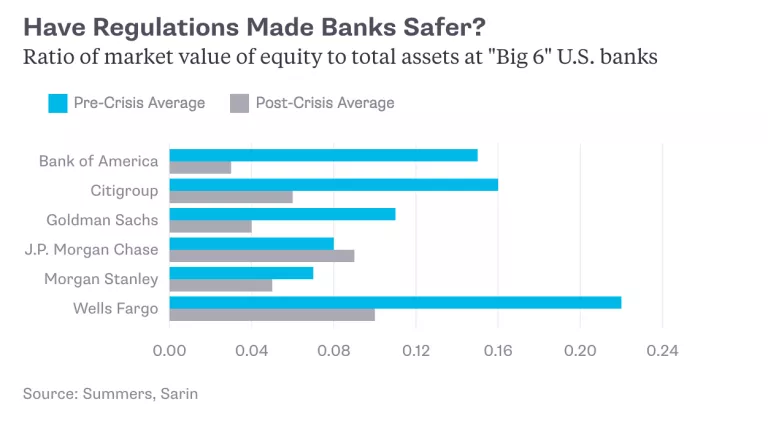

Last week Natasha Sarin and Lawrence H. Summers of Harvard University released a paper questioning whether Dodd-Frank has made big U.S. banks safer at all. The authors look at a variety of measures, including options prices, the ratio of market prices to book values, bank share volatility relative to overall market volatility, credit-default swap spreads and the value of preferred equity shares for banks. In every metric, it seems that the big banks are at least as risky as they were before the crisis, in part because they have lower capital values.

A critic might charge that pre-crisis price mismeasurements underestimated the risk to banks at that time, and in this sense the new realization of higher measured risks is more an acknowledgement of sad reality than a critique of Dodd-Frank. Still, when examined from other angles, the numbers on current bank safety are not reassuring. For instance, Sarin and Summers found that the prices of options implied that for major banks, the chance of a 50-percent price decline over the course of a year is 4.6 percent. Since that is almost a 1-in-20 chance, might the next crisis actually not be so far away?"

Furthermore, insurance against defaults has gotten more expensive as measured by credit-default swap spreads for the big banks. They’re now about three times higher than before the financial crisis. Does that indicate greater bank risk or a stronger belief that if there were another crash a government bailout might not come? We don’t know, but neither is reassuring. A no-bailout rule might work if banks respond by upping their capital values, but Sarin and Summers show that is exactly what has not happened.

Have Regulations Made Banks Safer?

Ratio of market value of equity to total assets at "Big 6" U.S. banks

It’s a common economic prescription that regulation should insist that banks carry high levels of capital to withstand losses in bad times. But although Dodd-Frank raised statutory capital requirements, it may have drained banks of some of their true economic capital by regulating and sometimes prohibiting valuable banking activities. The ratio of market price to book value has declined for the biggest banks, and that is one sign of falling values for true economic capital, even though banks have met the letter of law by increasing capital as the regulations specified. Sarin and Summers note that measures of bank capital, as defined by regulators rather than the market, have little predictive power for bank failures.

The core problem is this: The franchise value of banks fell after the crisis, which pushed banks closer to insolvency. As recovery proceeded, however, Dodd-Frank pushed down the value of banks once again. If your reaction to this problem is, “Regulation needs to be tougher yet,” that’s going to worsen the dilemma by bringing banks that much closer to insolvency. Maybe it was factors separate from Dodd-Frank, such as lower interest rates, that have had the biggest role in reducing the value of banks. Still, that means regulation isn’t addressing the most significant threats to bank solvency.

On top of all that, non-bank financial institutions like hedge funds, insurance companies and investment banks now have a much larger role in originating mortgages. They’re not covered by Dodd-Frank at all. So it’s not tougher regulation alone that we need, but smarter regulation.

Yet nobody really knows what a smarter version of Dodd-Frank should look like. The bill covers so many complex issues that an improvement just isn’t going to be that simple, and yes, something did need to be done after 2008. Sarin and Summers, among many others, are not looking to roll back bank regulation. Still, the weight of evidence is indicating that this one needs to be rethought.