- | Expert Commentary Expert Commentary

- |

New Research on Nonbank loans, the Federal Reserve, and the Export-Import Bank

Research Round-Up: April 29, 2019

How Do Small-Dollar, Nonbank Loans Work?

Thomas W. Miller, Jr. | Book

From the summary: "Millions of Americans rely on small-dollar, non-bank-supplied credit products: payday, pawn, vehicle title, and personal installment loans from finance companies. Many features of these vital products, however, are not well understood. This book contains explanations of how these loans work, what features they share, and how they differ. Readers seeking to understand these products might learn something surprising. For example,

- Pawn transactions are not loans in the traditional sense.

- Interest rate caps influence the size of installment loans.

- The length of a payday loan affects its annualized interest rate.

This objective guide is a must-read resource for legislators, regulators, journalists, and anyone else who cares about access to, and regulation of, small-dollar credit.”

Understanding the Federal Reserve

Scott Sumner | Policy Brief

From the brief: "The Fed influences macroeconomic variables such as inflation, unemployment, GDP, and interest rates by adjusting the supply and demand for base money. Because the Fed has a monopoly in the production of base money, it has almost unlimited ability to influence its value, which is why Congress gave the Fed the duty of stabilizing the price level. After all, the price level is merely the inverse of the value of money. Controlling inflation means stabilizing the value of money.

Because the Fed sets a short-term interest rate target, changes in that target are often a headline story in the financial press. However, there are actually many different forces that impact market interest rates, and low interest rates do not necessarily imply that an easy money policy is in effect. Some economists believe that the underlying movement in nominal GDP growth may provide a better indication of whether policy is easy or tight, relative to the underlying goals of Fed policy.”

Ex-Im Bank: A Comparative Analysis of Pre- and Post- Quorum Lending

Veronique de Rugy and Justin Leventhal | Policy Brief

From the brief: "Since the loss of quorum, the Bank has shifted its focus from large businesses to small ones. Instead of a few large companies representing the majority of the Ex-Im Bank’s financing, aid to small businesses is now dominant. Meanwhile, the prior large beneficiaries are nevertheless finding financing, and new methods are being created to serve these companies.

Importantly, Ex-Im Bank exposure to risk is down from its peak. This means US taxpayers are less exposed to the bank’s credit risk. Also, the share of the Bank’s portfolio with foreign firms that themselves receive subsidies from their own governments has decreased. What’s more, the Ex-Im Bank has had a negligible effect on total US exports.”

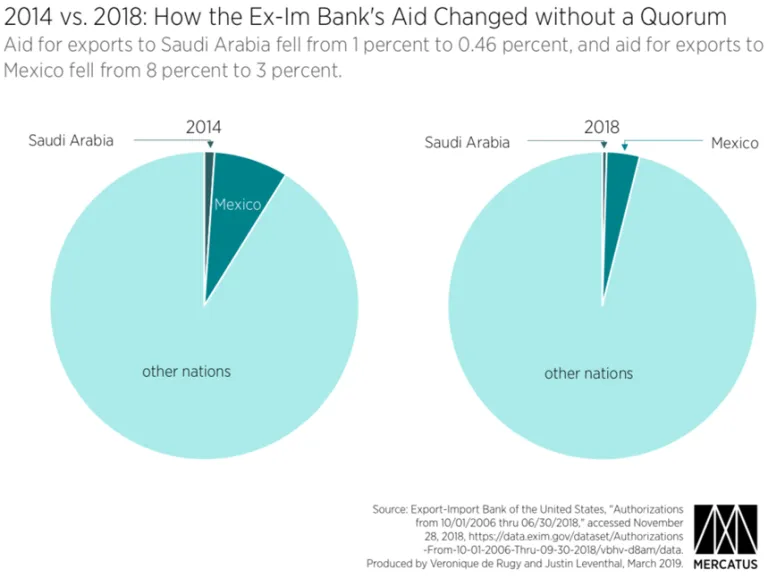

Accountability and the Ex-Im Bank: Country-Level Data

Veronique de Rugy and Justin Leventhal | Charts

From the publication: "Between FY 2014 and FY 2018, aid for exports to Mexico and Saudi Arabia fell to a share of the Ex-Im Bank’s total aid that more appropriately fit the size of those countries’ economies and the relative safety of exporting to them. The decreases in total aid for exports to companies in these nations outpaced the overall decrease in the Ex-Im Bank’s authorizations as a whole. This represents a rebalancing of the Ex-Im Bank’s actions away from prosperous and relatively stable nations to those where US exporters may actually face higher risk, putting the bank’s actions in line with its own charter. However, it should be noted that both Mexico and Saudi Arabia remain on the list of the Ex-Im Bank’s top beneficiaries, with Mexico remaining as the top foreign nation whose companies were identified as receiving Ex-Im Bank–aided exports.”