- | Monetary Policy Monetary Policy

- | Expert Commentary Expert Commentary

- |

A New Way to Manage Inflation

While the Fed’s new inflation target involves risks, it offers even greater opportunities

In a historic move, Federal Reserve Chair Jay Powell today announced a new framework that will govern how the US central bank conducts monetary policy. Powell, speaking at a virtual conference, outlined the Fed’s plans to change how it approaches inflation, replacing its current policy, which raises interest rates as inflation nears its target, with the adoption of a “make-up policy” that relies on an average inflation target to determine whether to raise interest rates or not. This new approach, if credibly implemented, would be a big change from what the Fed is currently doing and could potentially dampen the business cycle.

This announcement, in short, could be very consequential for the US economy. To understand why, it is useful to take a close look at the key parts of this new monetary policy framework and consider the benefits and challenges it may create.

Make-Up Policy

The first part of this new framework tasks the central bank with making up for past misses in its inflation target—the so-called make-up policy. The intuition behind make-up policy can be illustrated by imagining the economy as traffic on a highway. Traffic is traveling according to a speed limit of 65 miles per hour, and trips are planned accordingly. If an unexpected traffic jam—a recession—occurs, then vehicle speeds will temporarily fall below 65 miles per hour. Consequently, if motorists want to get to their destinations on time, they will have to temporarily drive faster than the speed limit after the traffic jam to make up for lost time.

This making up for lost time on the highway is equivalent to temporarily running the economy hot after a recession so that its total dollar size is fully restored to where it would have been in the absence of the downturn. Doing so, however, may cause inflation to briefly surge above the Fed’s 2 percent speed limit. Incorporating make-up policy into the Fed’s inflation target would allow this to happen in a systematic way. The announced average inflation target aims to do just that.

Average Inflation Targeting

The second part of the new framework involves the actual implementation of make-up policy through an average inflation target (AIT). This mechanism requires that the average inflation rate over a certain number of periods equal the target inflation rate. Consequently, if inflation has been below target in one period, then it has to be above target in a subsequent period. This creates a stable price level path.

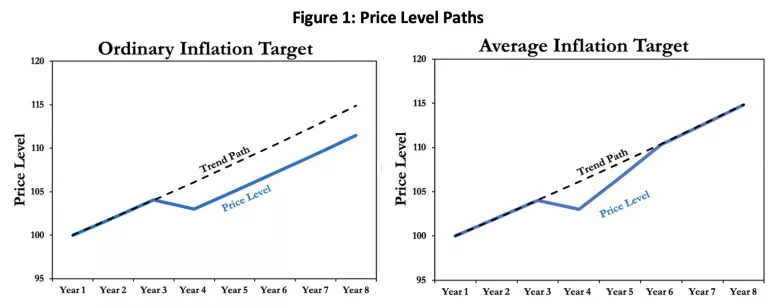

Table 1 illustrates AIT and how it is different from the Fed’s current framework or an ordinary inflation target (OIT). Both targets aim for 2 percent inflation and in this scenario are successful during their first two years. But when deflation of negative 1 percent occurs in year 3—say, owing to a recession—the way the Fed responds under each mechanism diverges.

Under the OIT, bygones are bygones and there is no need to make up for the missing inflation. The strategy is to get back on track and shoot for 2 percent inflation in year 4.

By contrast, the AIT recognizes that inflation was 3 percent below target in year 3 and corrects for it in subsequent periods. In this case, the missing 3 percent inflation is split in half and added to years 4 and 5, raising inflation in those years to 3.5 percent, or 1.5 percent over the 2 percent target for each of the next two years. Note that in this scenario the AIT results in an average inflation rate of 2 percent over the entire 7 years. The OIT, however, results in average inflation rate of 1.57 percent since there was no make-up for the inflation shortfall in year 3.

As Figure 1 shows, the OIT would cause the price level to drift away from the trend growth path of 2 percent. Over time this drift could become significant. For example, the Fed introduced its 2 percent Personal Consumption Expenditures Price Index (PCE) inflation target in 2012, and since then, the actual PCE price level has drifted about 6 percent below a stable 2 percent trend path. The OIT has real-world implications.

The AIT, on the other hand, returns the price level to its trend growth path of 2 percent in figure 1. An AIT, therefore, would create an outcome identical to a price level target (PLT). As long as the Fed reacted promptly to below-target misses in practice, an AIT and PLT would be identical in the real world too.

Benefits of Average Inflation Targeting

These different price level paths for the OIT and the AIT can have significant economic consequences coming out of a recession. First, the permanent below-trend decline in the OIT price level means a permanent below-trend decline in the dollar size of the economy. In turn, that implies a permanent below-trend decline in total dollar incomes. This shortfall would create problems for households and businesses holding mortgages, leases, and loans under the prerecession expectation of stable dollar income growth. Since the AIT’s make-up policy restores the originally expected price level path, it also would restore the originally expected dollar incomes and avoid this possibility of additional financial stress.

Second, if the public believes the AIT is credible so that the price level path and total dollar size of the economy will be quickly restored, then this belief can become a self-fulfilling prophecy and help dampen the business cycle. With the confidence created by AIT, households and business would be less likely to cut back on spending in the first place, and thus the economy would be less likely to go into a recession. But this requires credibility, and that may a be a problem for the Fed.

Challenges Created by Average Inflation Targeting

Fed Chair Jay Powell’s unveiling of the AIT was the culmination of a year and a half of review by the Federal Reserve of its framework. But is it credible? Will the public actually see this announcement as ushering in a new approach to monetary policy, or will the announcement be seen as just a minor tweak to the existing inflation target?

One obstacle to its credibility is that the AIT requires the Fed to allow inflation to temporarily run above its target coming out of a recession. This may be a tough sell to the public after suffering through the COVID-19 downturn. A better sales pitch for make-up policy is that the Fed wants the economy to temporarily run hot so that total dollar income can be rapidly restored to its prerecession growth path. This would be much easier to explain to the public than telling them higher inflation is in their best interest.

Another potential obstacle to credibly implementing the AIT is supply shocks. These affect the productive capacity of the economy and, as result, can temporarily cause movements in inflation. Negative supply shocks, in particular, such as oil shortages, trade disruptions, and wars, can cause inflation to briefly go up. The logic of the AIT says that any above-target inflation created by such shocks would have to be offset by lower inflation at a later time. It is hard to see the Fed, however, tightening monetary policy in an environment where negative supply shocks have already weakened the economy. A better approach would be for the Fed to see through temporary inflation caused by supply shocks.

While this latter obstacle is not an issue now, the former one is a real concern for the credibility of the Fed’s new AIT. The Fed will need to get buy-in from the public relatively soon if its AIT is to make a difference coming out of the current COVID-19 crisis.

Still, if Powell and other Fed officials can credibly implement their AIT, it will be a historic step not only for the Federal Reserve, but for central banking in general. For it will be the first time a major central bank has implemented make-up policy. This precedent may cause other central banks in other countries to follow the Fed’s lead. There will probably be kinks to be worked out in this new framework as it emerges, but it could be a first step toward an even better form of make-up policy, nominal GDP level targeting. Here’s hoping to a successful road ahead for AIT.

Image credit: Lance Nelson/Getty Images