- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Taxpayers Shouldn’t Pay for Corporate and Union Pension Promises

My recent column for Economics21 provided a factual overview of the worsening crisis in multiemployer pension plan underfunding, and a general explanation of why using taxpayer dollars to bail out these plans is a bad idea. Since then, rumors have swirled that lawmakers may try to jam a massive taxpayer-financed bailout of multiemployer pensions into an end-of-year budget deal. This would be an unusually horrible policy choice even by government standards, and lawmakers would do well to immediately extinguish any expectation that such an action might occur.

In this column I list specific reasons why a taxpayer-financed bailout would be damaging and irresponsible. For deeper understanding and background I direct readers to my previous column, as well as Rachel Greszler’s excellent issue brief. It is difficult to summarize the situation better than Greszler does:

“The government and taxpayers never had a seat at the negotiating table of these unions and employers, and the government and taxpayers never made any compensation promises to these workers. Workers are not at fault for broken promises of future pension benefits. But since neither taxpayers nor the government made those promises, they should in no way be obligated to stand behind them.”

It is natural to assume that in most public policy disputes, business management and labor will be on opposite sides of the negotiating table. But when it comes to employer-provided pensions, it is more typically the case that if management and labor agree on something, the taxpayer should beware. This is because management, company owners and labor representatives benefit enormously if their workers can be provided extra compensation in the form of pension benefits, but the employer does not have to pay for them. This dynamic in turn creates a strong temptation to stick taxpayers with the bill for workplace pension benefits. Indeed, a foundational purpose of federal pension law is to guard against this outcome, and instead to ensure that sponsors fund the pension benefits they promise, and only promise pension benefits they can fund.

In the particular case of multiemployer pensions, a plan’s benefit structure is decided upon by a board of trustees consisting equally of representatives of management and labor. It is the board of trustees’ responsibility to ensure that a plan’s benefit promises do not exceed the funds available to pay for them. It is an irresponsible shedding of this basic obligation to then turn around and pass that bill to taxpayers.

Workers who were promised these pension benefits have every right to demand them. However, they are owed the benefits by the plan sponsors, not by the taxpayer. Lawmakers should not let employers and union representatives off the hook for their responsibilities to these workers by putting taxpayers on the hook instead.

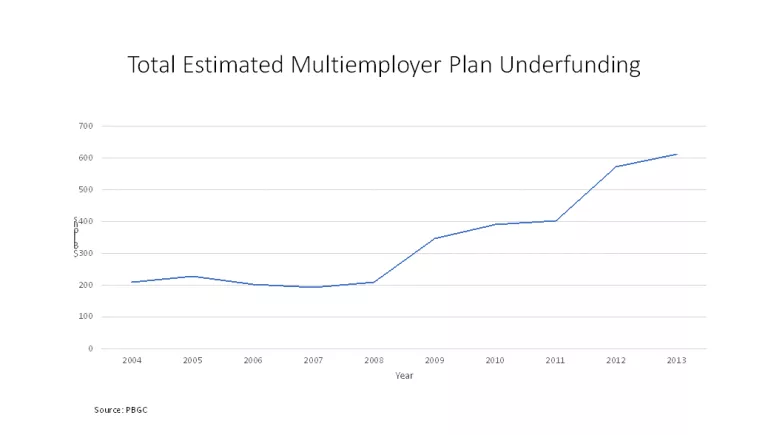

This issue is more than just a philosophical matter of corporate and union responsibility. The fiscal implications are vast and potentially very damaging. As soon as the door is opened to taxpayers paying for workplace pensions, that door cannot easily be closed until untold amounts are spent. Estimates made in 2013 put the size of multiemployer pension plan underfunding at over $600 billion, with the trend being such that the current amount is likely much higher.

In short, the legislation would require taxpayers to pick up the tab for multiemployer plan sponsors’ obligations well in excess of current pension insurance guarantees – a policy which, if extended throughout the multiemployer plan world, would ultimately cost taxpayers hundreds of billions of dollars. For context, consider that the federal government has still not developed a plan to finance its own retirement benefit obligations through Social Security, let alone to take on the additional burden of financing private workplace pensions.

Multiemployer plans are in this mess for a number of reasons, one of the key ones being that – like state and local pension plans but unlike single-employer plans – they have been permitted to assume away a good portion of their liabilities by choosing their own liability discount rates rather than using the ones economists would apply to estimate their actual value. Lowballing their actual liabilities permitted them to make inadequate funding contributions for several years, and sometimes to further increase unfunded benefits, thereby exacerbating current underfunding.

Although federal law permitted multiemployer plans to understate their liabilities for funding purposes, this does not excuse those plans that failed to fund their promised benefits. With the stock market currently at an all-time high, and the basic demographics of these plans well known for decades, responsible trusteeship would have involved taking the steps necessary to anticipate their plans’ funding needs.

The first order of business in any legislation affecting these plans should be fixing the liability discounting loophole in current multiemployer pension law. Not only plans asking for assistance, but all multiemployer pension plans, should discount their liabilities for funding purposes using the current high-quality corporate bond yield curve. In truth, even the single-employer pension discounting rules are currently too lax, with sponsors permitted to smooth away current market conditions by combining them with long-vanished ones. Any legislation to address multiemployer plans should include reforms requiring these plans to accurately measure their liabilities for future funding purposes.

Secondly, any assistance provided should not be financed by the US taxpayer. If such assistance is truly necessary to reduce the potential hit on the pension insurance system as its advocates claim, then it can and should be provided by the Pension Benefit Guaranty Corporation (PBGC), whose job it is to insure pension benefits. Lawmakers could expand PBGC’s authority to provide financial assistance to struggling multiemployer plans, while stipulating that PBGC must certify that any assistance package significantly improves the multiemployer insurance program’s net financial position. In effect, this would require that any financial assistance be coupled by concrete actions by recipient plans to reduce their underfunding.

It is especially important that lawmakers extinguish any signals to plan sponsors that taxpayers might swoop in to rescue them from their pension funding obligations. Such signals can only cause sponsors to delay much-needed corrections as they hope for a taxpayer bailout.

In sum, lawmakers should say no to any taxpayer-funded pension bailout, whether in this year’s omnibus legislation or any other context. Taxpayers should not be forced to pay for pension promises made by unions and corporations.