- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Understanding Social Security Benefit Adequacy: Why Benefit Growth Should Be Slowed

Many federal policy makers are aware that the Social Security program faces a substantial financing shortfall requiring correction. This would involve either increasing program taxes or slowing the growth of benefits – most likely both, given the size to which the shortfall has already grown in addition to the fact that neither party enjoys sufficient political power to impose its preferred solution on the other.

Many federal policy makers are aware that the Social Security program faces a substantial financing shortfall requiring correction. This would involve either increasing program taxes or slowing the growth of benefits – most likely both, given the size to which the shortfall has already grown in addition to the fact that neither party enjoys sufficient political power to impose its preferred solution on the other.

Social Security tax increases and benefit growth restraints are both politically unattractive; but at least one or the other is necessary to balance the program’s books if we intend to maintain Social Security as a self-financing program. Tax increases have obvious downsides that I have written about elsewhere and are not the subject of this article. The consequences of slowing benefit growth also concern many policy makers – specifically, whether Social Security can continue to offer adequate income protections if current benefit growth schedules are slowed.

As it turns out, however, it is not only possible to preserve Social Security benefit adequacy while slowing benefit growth, it is actually necessary if policy makers wish to avoid forcing participants into sub-optimal outcomes. This is good news, suggesting that Social Security cost restraints may embody a rare “win-win” policy opportunity. By slowing benefit growth, lawmakers can not only improve system finances, but the treatment of individual participants as well.

Background: Replacement Rates. To fully understand the issue of Social Security benefit adequacy, some familiarity is required with the “replacement rate” concept. Very loosely, a replacement rate is the ratio of one’s post-retirement to pre-retirement income. Financial planners often invoke the concept when advising individuals on how much to save for their retirement. A typical financial planner might suggest that retirement income needs to be at least 70–80% of pre-retirement income to maintain a consistent standard of living.

The current Social Security benefit formula is designed to hold replacement rates constant across time for certain similarly situated workers (as I will show, a very important specification) if benefits are claimed at the normal retirement age (NRA). To accomplish this, benefits are indexed under current law to grow with the national Average Wage Index (AWI) from one class of retirees to the next. Since wages tend to rise over time relative to price inflation (CPI), this formula produces benefits that grow faster than consumer prices. (This wage-indexing of the initial benefit formula should not be confused with the often-discussed issue of what version of CPI should be used to calculate annual Social Security COLAs).

Occasionally it is mistakenly said that Social Security benefits are scheduled to “decline” because under current law replacement rates at a fixed age, such as 65, will decrease. This is not actually a benefit decline but an artifact of the fact that under current law Social Security’s NRA will rise gradually to 67 by the early 2020s. Thus, individuals who retire at 65 thereafter will be subject to the reduction applied to early retirement benefits.

Calculating replacement rates at age 65 is clearly not the right way to measure benefit adequacy when the NRA is rising to 67. The scheduled NRA increase reflects a policy reality that as Americans live longer lives, the optimal age for entering retirement also rises; no sensible retirement planning strategy calibrates benefits at a forever-unchanging retirement age without taking into account how long individuals are expected to live. It also makes little analytical sense to assume the policy goal is to enable individuals to retire at age 65 with a full benefit, when lawmakers have deliberately chosen to raise the NRA to 67.

For these and other reasons, Social Security replacement rates – if invoked at all – are properly calculated at the NRA, when the individual is first eligible for full Social Security benefits. From this vantage point, there are a number of reasons why current-law Social Security benefit growth should be slowed, purely from a benefit equity perspective.

Reason #1: The current formula causes pre-retirement standards of living to decline relative to post-retirement living standards. The idea behind the current wage-indexing formula was to preserve benefit equity between generations; that is, to ensure that later cohorts received benefits that were as high a percentage of their pre-retirement earnings as previous generations did.

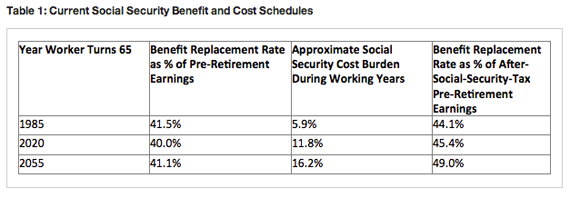

This, however, neglects the important factor that as the number of beneficiaries increases, the cost of maintaining wage-indexed benefits imposes larger tax burdens. The following table shows the rising cost burden successive generations must carry to fund the current benefit formula. The existing formula does not create income equity; instead it forces later generations to accept relatively lower pre-retirement living standards. It actually causes retirement benefits to grow faster than pre-retirement after-tax income. To correct this requires a reduction in the rate of benefit growth.

Reason #2: Social Security replacement rates are higher than commonly assumed and force many low-income workers into suboptimal income and consumption patterns. Most financial planners calculate retirement income replacement rates as a percentage of individual earnings prior to retirement. Social Security instead reports replacement rates as a percentage of an obscure and poorly-understood figure named the Average Indexed Monthly Earnings (AIME), which adjusts one’s prior earnings for intervening growth in the AWI. As a result, Social Security replacement rates are typically around 20 points higher than they are often misunderstood as being – indeed high enough to cause many low-wage workers to have less income while working than they expect after claiming Social Security benefits.

Andrew Biggs and Glenn Springstead found that when Social Security replacement rates were calculated as done in typical financial planning, and taking into account the sharing of taxes and benefits by married couples, individuals in the lowest income quintile expect Social Security benefits equal to 137 percent of their pre-retirement earnings (and 77 percent for the second-lowest quintile). This creates obvious disincentives for individuals either to extend their working careers or to engage in discretionary retirement saving. Perhaps most importantly, however, it means that the cost of supporting this level of Social Security benefits forces many low-income individuals to suffer lower living standards when working than they later experience as beneficiaries. Again, to correct this situation would require reductions in the growth of scheduled benefits.

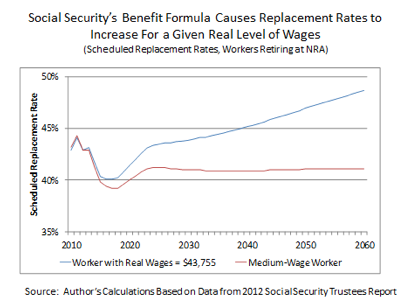

Reason #3: Real (inflation-adjusted) Social Security benefits are growing relative to real wages. It is sometimes inaccurately assumed that, because Social Security benefits are tied to wage growth, individuals with the same real wages must receive the same real benefits. This is not true. The current benefit formula causes Social Security replacement rates to rise over time relative to a given level of real wages. It is designed to pay the same replacement rates to so-called “similarly situated workers,” not to two workers with the same real wages born in different years. See the figure below.

The current Social Security benefit formula implicitly reflects a subjective value judgment that as society grows generally richer, the federal safety net should expand so that benefits for workers with a given real earnings level automatically become more generous. This is clearly not the only value judgment that could be made. One could alternatively argue that a given level of real wages should always return the same level of real benefits. One could just as reasonably argue that as society grows wealthier and more self-sufficient, individuals should receive relatively less in government benefits rather than more, relative to the real value of their Social Security contributions. Under either of these latter approaches, considerable reductions in Social Security benefit growth would be in order.

Policy Corrections: Whether the policy goal is to prevent pre-retirement living standards from declining relative to retirement benefits, to keep from forcing low-wage workers into sub-optimal lifetime income patterns, or to maintain a constant relationship between real wages and real benefits, Social Security benefit growth must be slowed substantially. Doing so would not only produce substantial systemic cost savings – e.g., maintaining constant replacement rates for a constant real wage would itself solve the majority of the financing shortfall – it would improve equity across generations.

Perhaps most importantly, a Social Security solution can honor the focus of left-of-center policy advocates on benefit adequacy, while also addressing the cost-containment concerns of right-of-center advocates. The first necessary step in such a discussion is to fully appreciate the limitations of certain common benefit adequacy measures as well as the adverse consequences that arise under current benefit formulas.

For more details, see my recent paper on this subject published with the Mercatus Center.