- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

Warning: Disability Insurance Is Hitting the Wall

For years Social Security’s trustees (of which I am one) have warned that lawmakers must act to address the troubled finances of the program’s disability insurance (DI) trust fund. Congress has nearly run out of time to do so. Legislation will be required during this Congress or, at the very latest, in a rush at the beginning of the next one, to prevent large sudden benefit cuts. The House of Representatives recently passed a procedural rule to prepare for the coming legislative debate. In this column I explain the issues in play.

For years Social Security’s trustees (of which I am one) have warned that lawmakers must act to address the troubled finances of the program’s disability insurance (DI) trust fund. Congress has nearly run out of time to do so. Legislation will be required during this Congress or, at the very latest, in a rush at the beginning of the next one, to prevent large sudden benefit cuts. The House of Representatives recently passed a procedural rule to prepare for the coming legislative debate. In this column I explain the issues in play.

The Problem

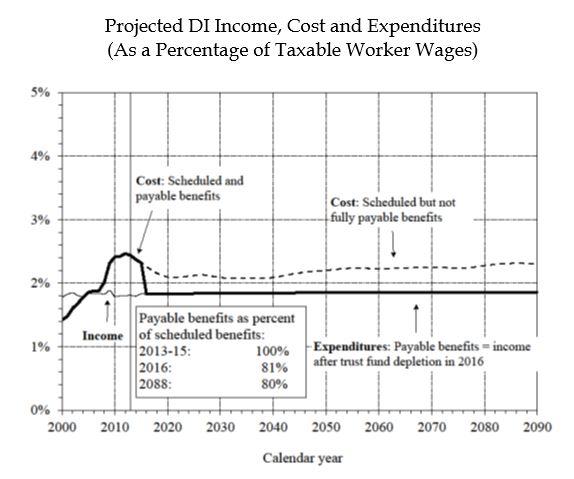

The problem in a nutshell is that Social Security’s disability trust fund is running out of money. The latest trustees’ report projects a reserve depletion date in late 2016. By law Social Security can only pay benefits if there is a positive balance in the appropriate trust fund (there are two: one for old-age and survivors’ benefits (OASI), the other for disability benefits). Absent such reserves, incoming taxes provide the only funds that can be spent. Under current projections, by late 2016 there will only be enough tax income to fund 81 percent of scheduled disability benefits. In other words, without legislation benefits will be cut 19 percent.

The Cause

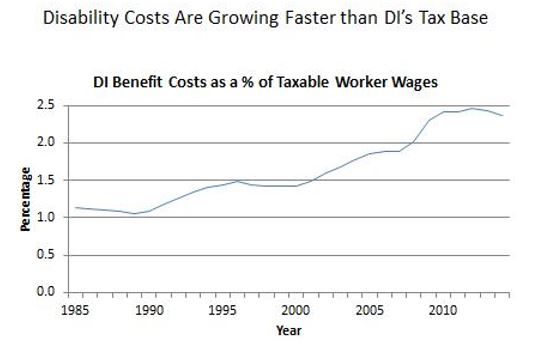

The cause of the problem is that DI costs have grown faster than the program’s revenue base. In 1990, the cost of paying DI benefits equaled 1.09 percent of taxable wages earned by workers. This year the relative cost is more than double that: 2.37 percent of the tax base.

The detailed reasons for the cost increase are beyond the scope of this column. (A good first source on these issues is the Social Security Chief Actuary.) The biggest reason is the growing number of beneficiaries, though real per capita benefits are also growing. Disabled population growth reflects several factors, including most notably the historically large baby boom generation moving through their ages of peak disability incidence (45-64). In addition, today more women have been employed long enough to be insured for disability benefits than was the case in earlier decades.

The growth in beneficiaries exceeds prior projections even after taking these factors into account. For example, the Chief Actuary reports that “the prevalence of disability among insured workers on an age-sex adjusted basis” rose by 42 percent from 1980 to 2010, even though there is no evidence suggesting that actual disability is much more common than it was thirty years ago. Instead the rise reflects causes ranging from a liberalization of eligibility criteria in 1984, to a surge in disability benefit applications when unemployment rose during the Great Recession.

Policy Ideals

Let us set aside political considerations from the outset and focus only on good policy. From a pure policy perspective the best solution is comprehensive reform shoring up Social Security financing on both sides (OASI and DI). Annual trustees’ reports have made clear that “lawmakers should address the financial challenges facing Social Security and Medicare as soon as possible” and that “earlier action will also help elected officials minimize adverse impacts on vulnerable populations.”

The worsening Social Security shortfall has already grown roughly twice as large as the one corrected with so much difficulty in 1983. Further delay in enacting comprehensive reforms would mean that still larger adjustments to taxes and benefits are required. Procrastinating for much longer worsens the risk that Social Security’s shortfall cannot be corrected at all, and that its historical financing structure will eventually have to be abandoned.

The integration of the disability and retirement components of Social Security also warrants a comprehensive response. The two sides use the same basic benefit formula to prevent discontinuities in benefit levels when the disabled reach retirement age. Criteria for benefit eligibility are integrated as well. A failure to address the two sides in tandem runs the risk of creating unintended inequities.

Reallocating Taxes Isn’t a Fix by Itself

Some have suggested that DI’s funding problem be addressed merely by giving DI some of the taxes now going to OASI (currently DI receives 1.8 points of the 12.4 percent payroll tax, OASI 10.6 points). As I have explained before, this suggests a misdiagnosis of the problem. The problem is not that DI commands too small a share of the tax relative to its obligations; to the contrary, OASI actually faces the larger actuarial imbalance. DI is hitting the wall first largely because the baby boomers hit their peak disability years before their retirement years; it is the first crisis triggered by the unsustainable financing arrangements threatening DI and OASI alike. Transferring funds from OASI to DI would weaken Social Security’s retirement component, which is in even worse long-term condition.

Lawmakers face a spectrum of choices. The most responsible and ambitious choice would be comprehensive reform shoring up Social Security as a whole. The most irresponsible (other than doing nothing at all) would be reallocating funds between DI and OASI for the purpose of delaying these necessary reforms, further increasing the risk of the shortfall growing too large to fix. The latter would be a national version of the tactics of avoidance that led to crises in many state pension plans.

Congress must determine the highest point on the responsibility scale at which it can produce legislation. Many outside experts are putting forth proposals to help lawmakers in this effort. The recently passed House rule allows for the full spectrum of responsible options, precluding only the worst outcome of making no net financing improvements whatsoever. Specifically, the rule requires that any tax reallocation occur in the context of broader reforms to improve Social Security finances, as recommended by the program’s six trustees in our annual message:

“Lawmakers may consider responding to the impending DI Trust Fund reserve depletion, as they did in 1994, solely by reallocating the payroll tax rate between OASI and DI. Such a response might serve to delay DI reforms and much needed financial corrections for OASDI as a whole. However, enactment of a more permanent solution could include a tax reallocation in the short run.”

The Historical Record

Some have suggested that a stand-alone payroll tax reallocation would be a routine action in keeping with historical precedent. This reflects substantial confusion about the historical record, which tells a wholly different story.

The last time Social Security taxes were reallocated was twenty years ago in 1994. The situation then (and surrounding other reallocations) was very different from today. DI costs had risen after the 1984 legislation liberalizing award determinations, rising further during a subsequent recession. Unlike the situation today, DI’s actuarial imbalance had then grown rapidly worse than OASI’s and much worse than prior projections.

In response to that looming insolvency threat, the program’s trustees recommended a number of actions, including a reallocation of taxes from OASI to DI. They were explicit that this proposed tax reallocation was to buy time (specifically, ten years) to enable comprehensive reforms.

In written testimony before Congress in 1993, the public trustees stated that while comprehensive reforms were the appropriate goal, there was yet “insufficient information to design specific proposals for the long term. . . the proposed reallocation for the short term will provide the time and opportunity to prepare and enact any needed changes in a careful and orderly manner.” The trustee present at the hearing, Stan Ross, cited a “prudent” goal “to meet short-term solvency so that both funds meet the 10-year test, and then to work on the long-term problems of both funds.”

In their 1994 message, the public trustees again voiced support for a temporary tax reallocation to avoid insolvency projected for 1995, but spent more of their message stressing that the purpose was to buy time for broader reforms:

“The 1994 Report continues to project that the DI fund will be exhausted in 1995. Therefore, we again strongly urge that action be taken as soon as possible to ensure the short-range financial solvency of the DI trust fund. We also strongly urge the prompt completion of the research efforts undertaken by the Administration at the Board's request. This research may assist the Congress as it considers the causes of the rapid growth in disability costs and addresses, as necessary, any substantive changes needed in the program. Disability Insurance under Social Security is nearly 40 years old. While some reforms have taken place over the years, the public is entitled to a thorough policy review of the program. The recent dramatic growth suggests the possibility of larger underlying issues related to the health and employment circumstances of workers and the need for responsive adjustments in the program.”

As recommended, lawmakers reallocated OASI/DI taxes in 1994. Rather than treat this as a resolution, the public trustees in their 1995 message made a further point of stressing that the tax reallocation was intended only to buy enough time for lawmakers to analyze, design and implement comprehensive reforms to control program cost growth:

“While the Congress acted this past year to restore its short-term financial balance, this necessary action should be viewed as only providing time and opportunity to design and implement substantive reforms that can lead to long-term financial stability. The research undertaken at the request of the Board of Trustees, and particularly of the Public Trustees, shows that there are serious design and administrative problems with the DI program. Changes in our society, the workforce and our economy suggest that adjustments in the program are needed to control long-range program costs. Also, incentives should be changed and the disability decision process improved in the interests of beneficiaries and taxpayers. We hope that this research will be completed promptly, fully presented to Congress and the public, and that the Congress will take action over the next few years to make this program financially stable over the long term.”

Despite these warnings, lawmakers have not yet implemented reforms as recommended by the trustees for several years. To reallocate taxes again in the absence of such reforms would be in direct conflict with the express purpose of the last reallocation. Clearly the last thing intended then was for lawmakers today to simply reallocate the taxes yet again, further postponing necessary reforms until both trust funds are on the precipice of insolvency.

Conclusion

The recently-enacted House rule conforms to the guidance repeatedly given by the program’s trustees on a bipartisan basis over several years. Those who suggest that DI’s impending reserve depletion warrants no action beyond taking revenues away from the Social Security retirement fund appear to be unfamiliar with the basis for the current allocation as enacted in 1994. Lawmakers should begin work now, with the assistance of responsible outside experts, on a bipartisan package of reforms to strengthen the disability program and Social Security as a whole.