- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

What the New York Times Isn't Telling You about Social Security

No politician on either side of the aisle reaps a political windfall from proposing to slow Social Security benefit growth. Responsible stewardship nevertheless requires that public pension plans such as Social Security only promise benefits that can be securely funded. Those who step forward with credible plans for correcting Social Security’s untenable cost growth trend are obeying the demands of responsibility, not ideology.

The New York Times recently published an editorial highlighting partisan differences over Social Security, advocating that current-law benefit growth be increased, and implicitly rejecting bipartisancalls to include some cost containment in legislated financing reforms. The Times, like everyone else, is within its rights to present its views on an important public policy concern. Adoption of its recommended position, however, would carry critical consequences of which the body politic should be aware. Among the pertinent considerations:

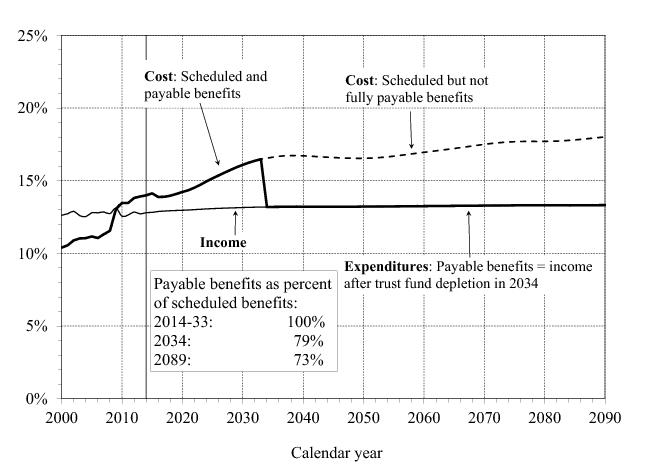

#1: Social Security costs are growing faster than the underlying economy or its tax base can sustain.Total Social Security costs never exceeded 12% of workers’ taxable wages before 2009. Since then costs have grown to roughly 14% and are currently projected to exceed 16.7% within twenty years (see Figure 1, reproduced from the Trustees’ report). In other words, one out of every six taxable dollars workers earn would be needed to finance this single federal program – and costs would continue to grow afterward. Raising benefits above current schedules would increase these costs still further.

Figure 1: Social Security Cost, Income and Expenditures as a Percentage of Taxable Worker Wages

#2: There is little evidence suggesting elected officials are willing to impose taxes at levels necessary to finance scheduled benefits, let alone higher ones. The immediate and permanent payroll tax increase necessary to finance scheduled (i.e., promised) benefits would be from today’s 12.4% rate to over 15%. If delayed until the program’s combined trust funds are nearing depletion, the required rate would be over 16%. Moreover, applying the payroll tax to additional wages as endorsed by the Times would not come close to meeting projected obligations (let alone a benefit expansion) even if SSA eliminated all benefit payments earned by the added contributions.

Despite annual trustees’ warnings and the growth of the funding shortfall beyond what has been successfully repaired in the past, lawmakers have declined to assess the taxes needed to finance scheduled benefits. To the contrary, lawmakers granted temporary relief even from the current 12.4% rate after the Great Recession. If lawmakers remain unwilling to align benefit schedules and incoming revenues, Social Security’s historical financing structure will no longer be viable.

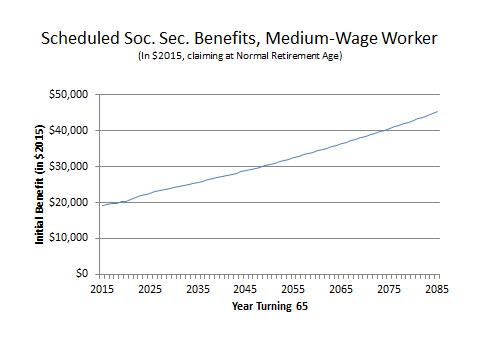

#3: Under current law the purchasing power of benefits increases automatically (see Figure 2).

Figure 2: Scheduled Social Security Benefits

Importantly, this rate of benefit growth is faster than the growth in workers’ after-Social-Security-tax pre-retirement earnings. In other words, Social Security is steadily lowering workers’ living standards relative to those they expect as beneficiaries, a trend that would be exacerbated by the tax increases required to finance accelerated benefit growth.

#4: Further increasing costs would worsen the treatment of younger generations who already stand to lose the most net income through the program. This is because Social Security is not a savings program but rather an income transfer program. Because the program does not add to total national savings available to finance retirement benefits, it is a zero-sum game at best; income transferred to one group produces losses for another. As it happens, the largest net income losses through the program under current law will be experienced by generations just now entering the workforce (they will lose over 4% of their career wages). If near-term retirees’ benefits are increased relative to their own contributions, many high-income people will benefit while the net income losses facing younger generations will worsen still further.

#5: Program costs have already risen to the point where many low-income people now receive lower incomes as workers than they do later as Social Security beneficiaries. CBO’s latest estimates show scheduled Social Security benefits replacing more than 100% of pre-retirement income for workers in the lowest income quintile. Given that many financial planners advise individuals to aim for a 70% replacement rate in retirement to maintain prior living standards, these trends raise fundamental concerns about program fairness and efficacy, in addition to warping work and savings incentives. Further benefit increases would exacerbate these problems.

#6: Further increasing benefit promises beyond available program resources would move Social Security closer to the troubled state of many state and local pension plans. Such plans got into severe trouble, threatening disruptions in workers’ retirement income, by promising benefits in excess of their ability to pay. Increasing promised benefits when Social Security already faces a substantial financing shortfall would repeat these mistakes on a national scale.

The Times editorial also contains some questionable analytical assertions. Among them:

#1: The Times asserts there is “no compelling evidence” warranting changes to the Consumer Price Index (CPI-W) used for calculating cost-of-living adjustments. Actually, economists across the political spectrum generally agree that CPI-W overstates price inflation and that a chained index would be more accurate.

#2: The Times states that raising Social Security’s eligibility age would “hit low-income workers the hardest. “ This is often assumed but studies have found it to be untrue. Determining a reasonable number of years over which benefits are paid is a critical factor in safeguarding retirement security; our national failure to adjust Social Security for longevity growth means that tax burdens must be higher and/or annual benefits lower than they otherwise would be, undercutting income security. Moreover, CBO, SSA’s Office of Retirement Policy and a recent National Academy of Sciences study all find that retirement age increases would not be regressive, contrary to the Times’s allegation.

#3: The Times cites widespread reliance on Social Security in support of its arguments for expanding the program. The logic is tenuous at best; expanding Social Security’s promises would simultaneously increase dependence on its benefits and reduce their reliability, while also further depressing other retirement saving.

#4: This last point is interpretative, but important: the Times miscasts the Social Security debate by depicting it primarily as a political divide. Far more salient than political or ideological divisions is a financing shortfall that must be resolved as a matter of arithmetic.

No politician on either side of the aisle reaps a political windfall from proposing to slow Social Security benefit growth. Responsible stewardship nevertheless requires that public pension plans such as Social Security only promise benefits that can be securely funded. Those who step forward with credible plans for correcting Social Security’s untenable cost growth trend are obeying the demands of responsibility, not ideology.