- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

What the Recent CBO Report Tells Us About Fiscal Stimulus and the Federal Budget

The findings of CBO’s gloomy long-term report come as no surprise. Over the most recent four years, the U.S. government has engaged in continued massive deficit spending on a scale not seen since World War II. CBO finds that the continuation of such policies in future years will lead to federal fiscal ruin and severe economic hardship.

This article was originally published in e21

The Congressional Budget Office (CBO) recently released two important reports on the federal budget. One analyzes the short term, the other the long term.

The first report explains what is projected to happen, both to the federal budget and to the larger economy, in the near term due to year-end expirations of various tax and spending policies.

The other report projects what will happen to the federal budget over the upcoming decades.

Both reports analyze two scenarios; first, if certain provisions of current law (raising taxes and cutting spending) are upheld, and second, if they are legislatively overridden.

The findings of CBO’s gloomy long-term report come as no surprise. Over the most recent four years, the U.S. government has engaged in continued massive deficit spending on a scale not seen since World War II. CBO finds that the continuation of such policies in future years will lead to federal fiscal ruin and severe economic hardship.

The short-term report is more nuanced. CBO finds that continued deficit-spending will increase economic growth in the near-term but weaken growth over the long term.

Here is CBO describing adverse near-term economic effects if various current tax and spending policies are allowed to expire as scheduled under current law:

Under those fiscal conditions, which will occur under current law, growth in real (inflation-adjusted) GDP in calendar year 2013 will be just 0.5 percent, CBO expects—with the economy projected to contract at an annual rate of 1.3 percent in the first half of the year and expand at an annual rate of 2.3 percent in the second half. Given the pattern of past recessions as identified by the National Bureau of Economic Research, such a contraction in output in the first half of 2013 would probably be judged to be a recession.

But CBO also finds that continuing current deficit-spending practices would lead to a weaker economy in the years ahead:

However, eliminating or reducing the fiscal restraint scheduled to occur next year without imposing comparable restraint in future years would reduce output and income in the longer run relative to what would occur if the scheduled fiscal restraint remained in place.

It’s important for policy makers to understand both of these effects. Continued deficit spending can prop up the economy in the near term but in the long run it both exacerbates federal fiscal problems and undercuts economic growth.

Thus, as we attempt to cushion ourselves against recession by running large federal deficits, we also weaken the economy our children will inherit. We also increase the probability that we’ll later face our current economic problems all over again, precipitating another future debate on whether we need still more stimulus spending. When that debate happens, federal finances will be even weaker than they are now. Continued deficit spending can thus lead to a vicious cycle in which there is an ever-increasing perceived need for short-term interventions, each of which worsens the long-term picture.

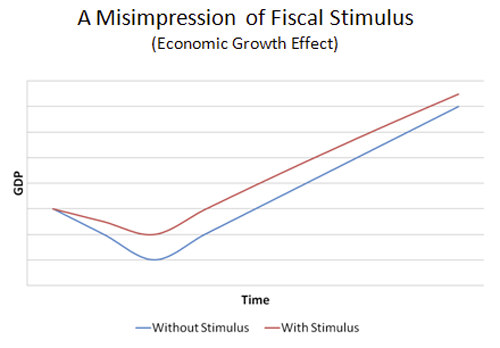

Most economists acknowledge these trade-offs. But sometimes the rhetoric employed to argue for more stimulus spending obscures them. Respected economist Larry Summers has said that one objective of fiscal stimulus is to enable the economy to achieve “escape velocity.” The phrase (to my ear) risks creating the misimpression that stimulus injections will actually help the economy to ultimately be stronger than it otherwise would have been. The picture below captures such a misimpression:

As depicted above, stimulus limits the pain of a near-term economic contraction. The picture also asserts that over the long run we’re better off having employed it, even though the later growth rate has been made a little bit slower (see how the slope of the red line is a bit less than that of the blue line). This image of stimulus is one of reducing near-term economic hardship and ultimately getting us back more quickly to where we want to be.

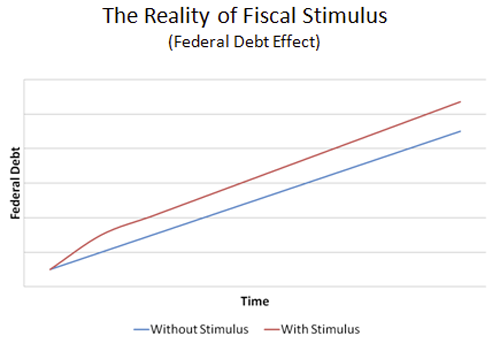

But that’s not what CBO and most other expert economists tell us happens with stimulus spending. They tell us instead that stimulus spending reduces long-term growth rates enough so that in the long run our economy is weaker than it would otherwise be. The real picture is thus more like this:

CBO, for example, finds that if current deficit-spending policies continue to be extended indefinitely, GDP will be more than 13% lower by 2037 than it otherwise would be.

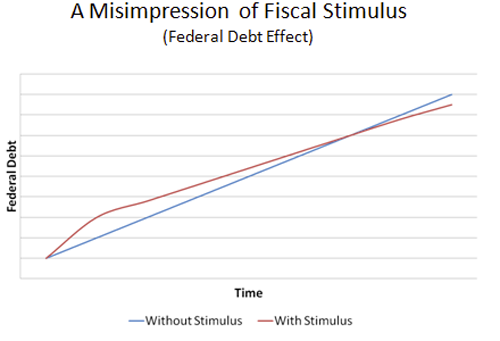

Similar misimpressions may exist with respect to the effect of fiscal stimulus on federal finances. Advocates of stimulus spending sometimes come close to arguing that it pays for itself – that ultimately federal finances will be better off due to it having been enacted. In the near term these advocates acknowledge that there will be a temporary increase in government debt, but assert that in the long run federal finances will be no worse, possibly even better, as the government reaps the benefits of having staved off a severe economic contraction. Again, see the picture below:

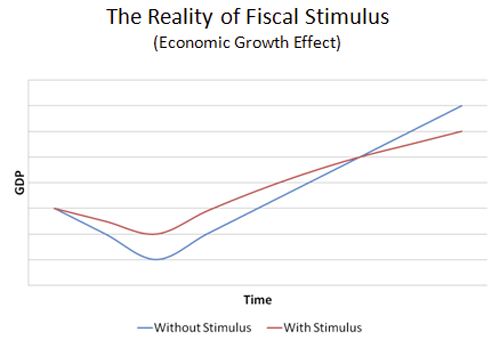

But once again this is not what CBO and other experts tell us that stimulus spending does (at least in the form that a real-world Congress enacts). They tell us that stimulus spending worsens federal finances both in the short-term and the long-term, as in the picture below. Given the weak condition of federal finances, this is a downside warranting our attention.

Deficit spending thus represents a policy decision to strengthen near-term economic performance at the expense of long-term performance, and at the expense of federal finances both in the near term and the long term.

This doesn’t mean that government should never engage in counter-cyclical deficit spending. We may make the value judgment that it is worth it to reduce future generations’ prosperity somewhat to mitigate economic hardship present today. But we need to recognize that this is what we are doing.

I have written before that having so many “temporary” tax and spending provisions in law is terrible budget practice, and that both parties would do well to eliminate the entire array and replace them with permanent policies. That said, I would caution fellow conservative advocates of tax rate permanency not to make this case primarily in terms of near-term economic effects. As the CBO report exemplifies, a short-term view of the economy will always appear to favor higher deficits and specifically more stimulus spending. If the economic debate focuses only on a near-term view, it will more often than not lead to policy choices that conservatives oppose.

I actually find little to disagree with in the following sentences from a recent Center on Budget and Policy Priorities publication on the “fiscal cliff.”

CBO's report is, in fact, about the trade-offs involved in adopting policies to avoid this worst-case short-term outcome, which policymakers almost surely will do — one way or another. The question is whether policymakers will respond to frightening rhetoric about the immediate economic impacts of a "fiscal cliff" by simply extending current policies and postponing the hard decisions needed to restore long-term fiscal stability. That would be a serious mistake and an unnecessary step.

I tend to disagree with the analysts at CBPP on the optimal contents of a long-term fiscal sustainability package (I would like to see current income tax rates made permanent for many taxpayers for whom they would likely not, and I would like to see tighter constraints on the growth of entitlement spending). I nevertheless agree with them that long-term fiscal policy should not be an accidental byproduct of lawmakers perpetually seeking to avoid adverse short-term effects.

If advocates on the left and the right can first agree that current budget policies are unsustainable, and that we desperately need to shift our focus away from short-term stimulus injections toward sensible, sustainable long-term policies, we will be much better off for it.