- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

- |

European Countries Can't Continue on Their Spendaholic Track

The European Union is the latest in a series of international bureaucracies to make the case that European countries should ease their stance on austerity. The underlying assumption behind this new policy position is that so far austerity has failed. If by that one means that the large tax increases implemented by European countries were counter-productive, then that is correct. But if it means that European countries have implemented savage spending cuts, then it is incorrect.

The European Union is the latest in a series of international bureaucracies to make the case that European countries should ease their stance on austerity. The underlying assumption behind this new policy position is that so far austerity has failed. If by that one means that the large tax increases implemented by European countries were counter-productive, then that is correct. But if it means that European countries have implemented savage spending cuts, then it is incorrect.

{kind=link}

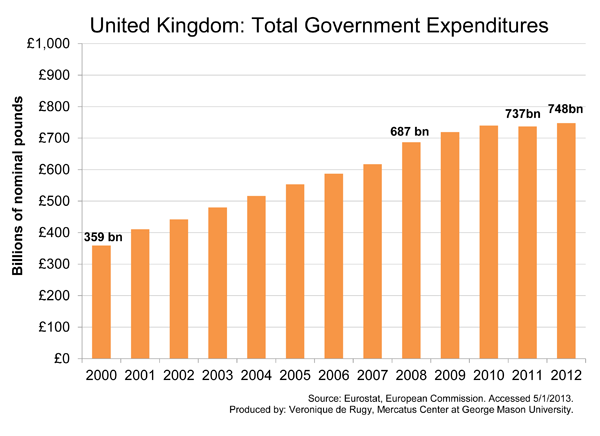

Unfortunately, the idea that austerity has failed in Europe is evidence of the lack of clarity that has obscured most of the debate so far. Let's be clear: European countries do not have the luxury of continuing on their current fiscal path. Who could argue, for instance, that it would have been better for Greece to continue on its spendaholic track? For many European countries, the lack of austerity means more deficit spending, which likely will trigger large increases in interest rates, debt restructuring (read defaults), capital levies and even more weakness in the banking sector.

The second problem with this simplistic view is that it fails to recognize that in the pursuit of austerity, the important question has less to do with the size of the austerity package than what type of austerity measures are implemented. Austerity can take different forms. It can be achieved by cutting spending or by raising taxes. Alternatively, austerity can be achieved by adopting a mix of spending cuts and tax increases.

The general consensus in the academic literature is that the composition of fiscal adjustment is a key factor in achieving successful and lasting reductions in debt-to-GDP ratio. The work of economists at Harvard University, the International Monetary Fund and the Organization for Economic Cooperation and Development, among others, has shown fiscal adjustment packages made mostly of spending cuts are more likely to lead to lasting debt reduction than those made of tax increases.

Most countries, it turns out, implemented spending cuts in name only and these cuts were often overwhelmed by much larger tax increases. While the finding that spending cuts are more effective at achieving debt reduction is not controversial, there is still significant debate about the short-term economic impact of fiscal adjustments. There are, however, some clear lessons:

1) Expansionary fiscal adjustments are possible.

2) While fiscal adjustment may not always trigger economic growth, spending-based adjustments are much less costly in terms of output than tax-based ones. In fact, when governments try to reduce the debtby raising taxes, it is likely to result in a deep and pronounced recession, making the fiscal adjustment counterproductive. Thus, we shouldn't be surprised by the impact that tax-revenue based austerity has had in Europe.

3) These expansionary fiscal adjustments are more likely to succeed when they are accompanied by growth-oriented policies such as labor and goods market liberalization. Monetary policy was also proven to facilitate the spending cuts. Countries such as Germany and Finland, and other more recent examples such as Estonia and Sweden, have managed both debt reduction and some level of growth.

Related Content

- | Government Spending Government Spending

- | Research Papers Research Papers

Austerity: The Relative Effects of Tax Increases versus Spending Cuts

- | Government Spending Government Spending

- | Research Papers Research Papers

In Search of Austerity: An Analysis of the British Situation

- | Government Spending Government Spending

- | Expert Commentary Expert Commentary

In Europe, Time for True Austerity