The Senate recently confirmed Howard Shelanski to head the Office of Information and Regulatory Affairs (OIRA). Shelanski is by all accounts a thoughtful scholar, and one of the first things he should try to solve is the long-standing transparency problem in federal regulation.

The Senate recently confirmed Howard Shelanski to head the Office of Information and Regulatory Affairs (OIRA). Shelanski is by all accounts a thoughtful scholar, and one of the first things he should try to solve is the long-standing transparency problem in federal regulation. Simply put, agencies often fail to explain how they use economic analysis — which is required by executive orders — to make decisions about major regulations that affect Americans’ health, wellbeing and pocketbooks.

Economists play a key role in advising policymakers. When the government implements a new program, economists project how the new spending will affect the federal deficit and economic growth. They may also forecast how a tax increase will affect federal revenues. While often imperfect, these projections play a critical role because they provide decision-makers with information about the likely effects of policies.

Without this information, policymaking would be a lot like throwing darts while blindfolded. Decision-makers would choose policies based on blind faith that a proposal would produce good results.

Unfortunately, when it comes to regulation, this analogy is not far from the truth. Since the early 1980s, presidents required federal regulatory agencies to conduct Regulatory Impact Analyses (RIAs) for major regulations. OIRA reviews each agency’s analyses to see if it has identified a widespread problem regulation might solve, considered a variety of alternative solutions and selected the most sensible approach. But agencies often fail to explain how the economic analysis informed their decisions.

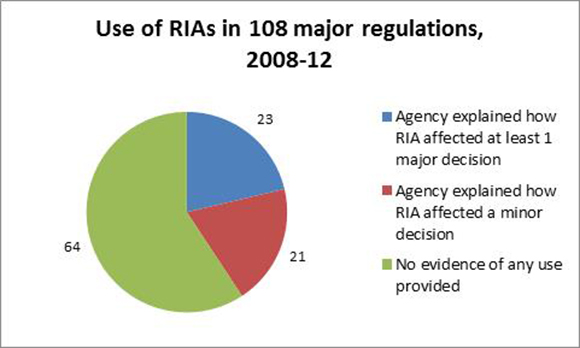

The data prove this. In 2008, the Mercatus Center’s Regulatory Report Card started to evaluate the quality of executive branch agencies’ RIAs for major regulations and the extent to which agencies explain how they used the analysis in their decisions.

One Report Card criterion asks whether the agency claimed or appeared to use any part of the analysis to guide decisions. As the chart below demonstrates, more than half of the major regulations — those with an estimated economic impact of at least $100 million — analyzed in the study were implemented without any evidence that agencies used RIAs.

Too often, economic analyses of regulations look like they were crafted to justify a premade decision, rather than serving as a way to carefully consider the effects of different alternatives. Numerous regulations evaluated in the Mercatus Report Card also lack information comparing the benefits and costs of multiple alternatives.

For example, in 2012 the Department of Health and Human Services proposed sweeping regulations to establish federal health insurance exchanges and regulate the types of plans insurers can offer. Neither regulation was accompanied by any analysis of the benefits or costs of alternatives, which suggests that the department never seriously considered alternatives to the regulations it wanted to propose.

Similarly, in 2008 the Bush administration proposed a regulation requiring federal contractors to use the electronic E-Verify system to verify employees’ identities. The accompanying analysis considered only one narrow alternative: requiring verification only for new employees instead of all employees. It estimated the costs but not the benefits of the alternative.

People might disagree about how much, and what type of, regulation is justifiable, but we should all be able to agree that government owes us a clear explanation of how it’s making decisions.

In theory, an OIRA administrator could help fix this problem by returning proposed regulations to agencies when they fail to clearly explain how they use economic analysis in their decisions. And surely the quality of analysis is better with OIRA reviewing regulations than without OIRA’s input. Yet sub-standard analysis persists, even with OIRA’s regulatory oversight in place for more than three decades.

To improve the quality and use of RIAs, the federal government could need a stronger enforcement mechanism. Legislation requiring economic analysis of proposed regulations, for example, could allow judges to invalidate regulations if the court finds that an agency failed to conduct a thorough economic analysis and an explanation of how that analysis affected decisions. The law need not require that quantified benefits of a regulation exceed its costs. It could merely be a procedural requirement that RIAs must meet minimum quality standards and the agency must explain how its decisions relate to the evidence.

Current regulatory institutions fail to hold agencies sufficiently accountable for explaining how their analysis informs decisions. Now that he is OIRA’s administrator, hopefully Shelanski will make this problem’s resolution a priority.