- | Regulation Regulation

- | Data Visualizations Data Visualizations

- |

Dodd-Frank and the Federal Reserve’s Regulations

The Dodd-Frank Wall Street Reform and Consumer Protection Act has been generally associated with an explosion in federal financial regulatory restrictions. RegData permits us to specifically examine which agencies produced regulatory restrictions associated with the law. Dodd-Frank was associated with a substantial increase in the Federal Reserve’s role as a regulator, as its number of regulations jumped 32 percent in the 4 years since the passage of the legislation.

The Dodd-Frank Wall Street Reform and Consumer Protection Act has been generally associated with an explosion in federal financial regulatory restrictions. RegData permits us to specifically examine which agencies produced regulatory restrictions associated with the law. Dodd-Frank was associated with a substantial increase in the Federal Reserve’s role as a regulator, as its number of regulations jumped 32 percent in the 4 years since the passage of the legislation.

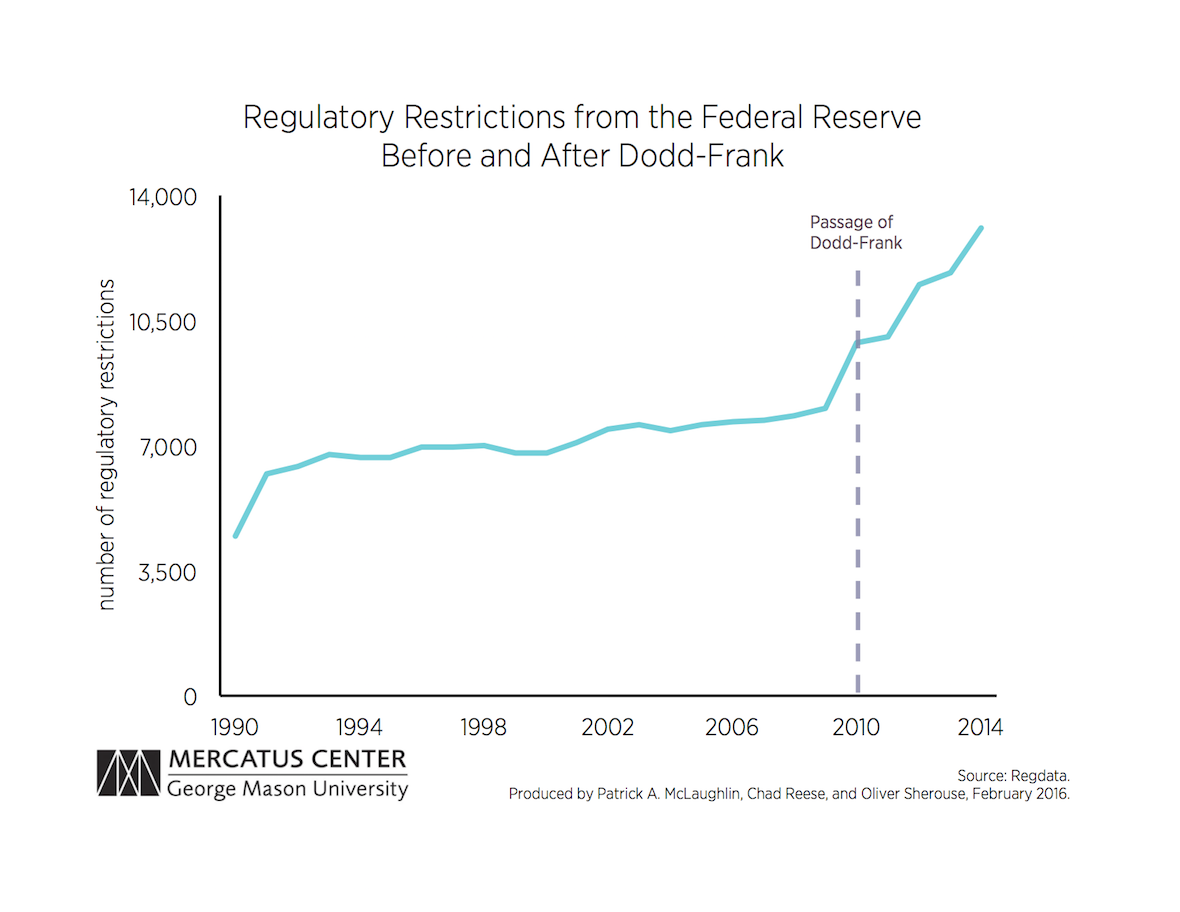

The chart below tracks total cumulative restrictions from the Federal Reserve from 1990 to 2014.

The dotted line in the chart marks the passage of Dodd-Frank in 2010. The accumulation of regulatory restrictions accelerated between 2009 and 2010, almost entirely from restrictions associated with the Credit Card Accountability Responsibility and Disclosure Act of 2009. There was, however, an even more noteworthy increase in total regulatory restrictions between 2010 and 2014, as the Federal Reserve added 3,186 new regulatory restrictions in response to Dodd-Frank. The Federal Reserve’s regulatory restrictions grew as much over the four years after Dodd-Frank was enacted as they did during the decade and a half prior to the law’s creation.

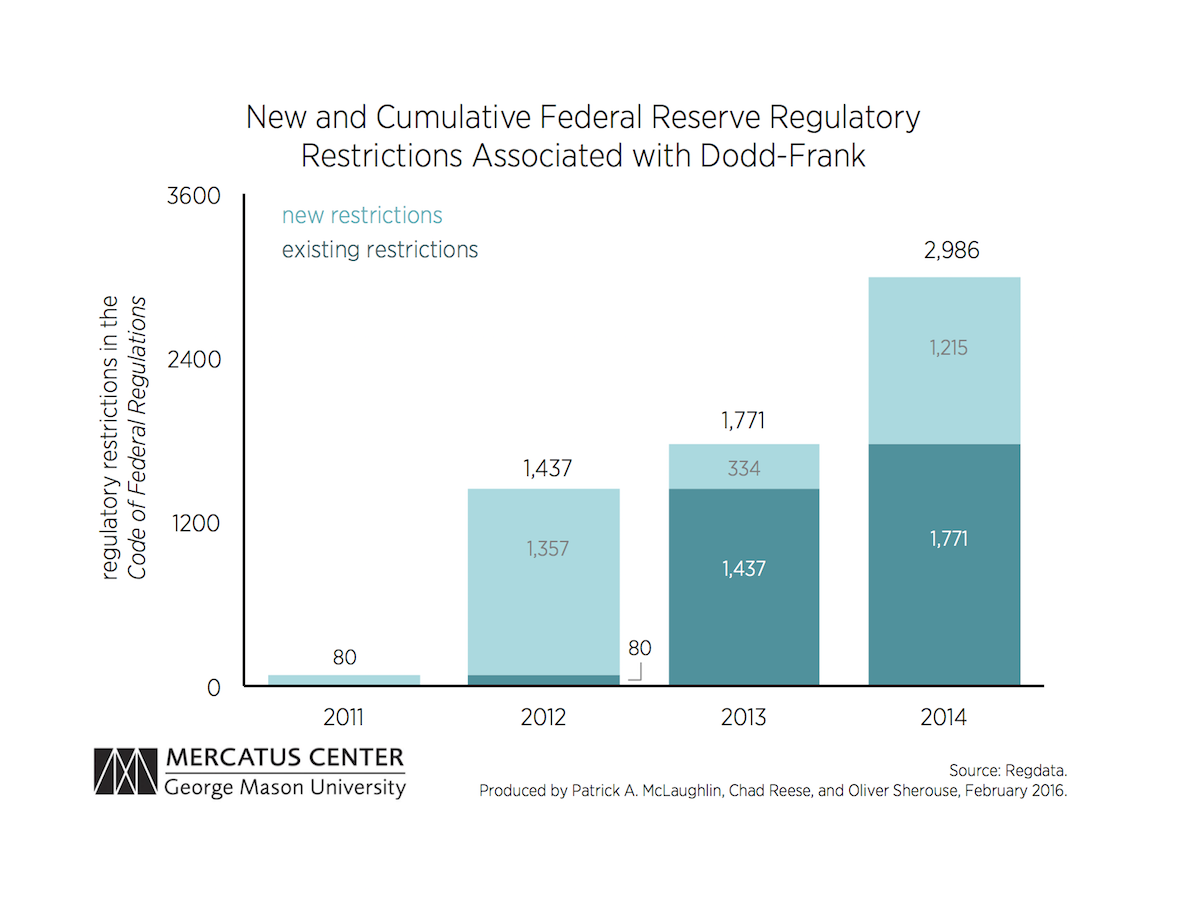

The chart below plots the annual growth of the Federal Reserve’s new and cumulative regulatory restrictions that are associated with Dodd-Frank.

The Federal Reserve’s increased pace of rulemaking since 2011 is striking. From 2013 to 2014 alone, regulatory restrictions imposed by the Federal Reserve associated with Dodd-Frank grew by nearly 70 percent. As our colleagues have noted in the past, Dodd-Frank substantially increased the Federal Reserve’s regulatory authority, a claim clearly supported by the data. This surge in regulatory activity at the Federal Reserve now means that nearly one-quarter of all regulatory restrictions imposed by the Federal Reserve are associated with Dodd-Frank. Importantly, of the 132 rulemaking requirements for all bank regulators (including the Federal Reserve), the law firm Davis Polk reports that only 83 were finalized as of September 30, 2015—meaning the total effect of Dodd-Frank on the Federal Reserve is not yet reflected in the data.

These charts understate the level of regulatory growth for financial firms and consumers, because they only reflect the growth in a single agency. They do not include, for instance, growing regulatory burdens for mortgages and other consumer debt products once regulated by the Federal Reserve, but now under the purview of the Consumer Financial Protection Bureau.

The expansion in the Federal Reserve’s regulatory role should raise concern about its rulemaking processes, including the use of regulatory analysis. While the Federal Reserve’s internal rulemaking policy calls for regulatory analysis to carefully consider, among other things, the “economic implications” of rules, it has not always adhered to that policy.

Moreover, the Federal Reserve enjoys a significant amount of independence as the arbiter of monetary policy. In view of the significant increase in regulatory activity post-Dodd-Frank, however, it is worth questioning whether the institutional protections from congressional oversight designed to keep monetary policy independent also prevent appropriate regulatory oversight of the Federal Reserve’s rulemaking activities.