- | Corporate Welfare Corporate Welfare

- | Data Visualizations Data Visualizations

- |

Ex-Im’s Working Capital Programs Benefit Big Businesses and Banks

Defenders of the US Export-Import Bank (Ex-Im Bank) cite its working capital programs as evidence that the agency plays a critical role in supporting small businesses. As one of four main components of Ex-Im’s export subsidies, the working capital programs represent a relatively small component of the agency’s overall portfolio. The agency as a whole mainly benefits large, politically connected firms, as I have previously demonstrated.

Defenders of the US Export-Import Bank (Ex-Im Bank) cite its working capital programs as evidence that the agency plays a critical role in supporting small businesses. As one of four main components of Ex-Im’s export subsidies, the working capital programs represent a relatively small component of the agency’s overall portfolio. The agency as a whole mainly benefits large, politically connected firms, as I have previously demonstrated.

Even though small businesses are the main beneficiaries of the Ex-Im Bank’s working capital programs, big businesses still remain big recipients indirectly and directly. The working capital program transfers the risk of lending from the lenders (often big banks or sometimes Boeing itself) to taxpayers.

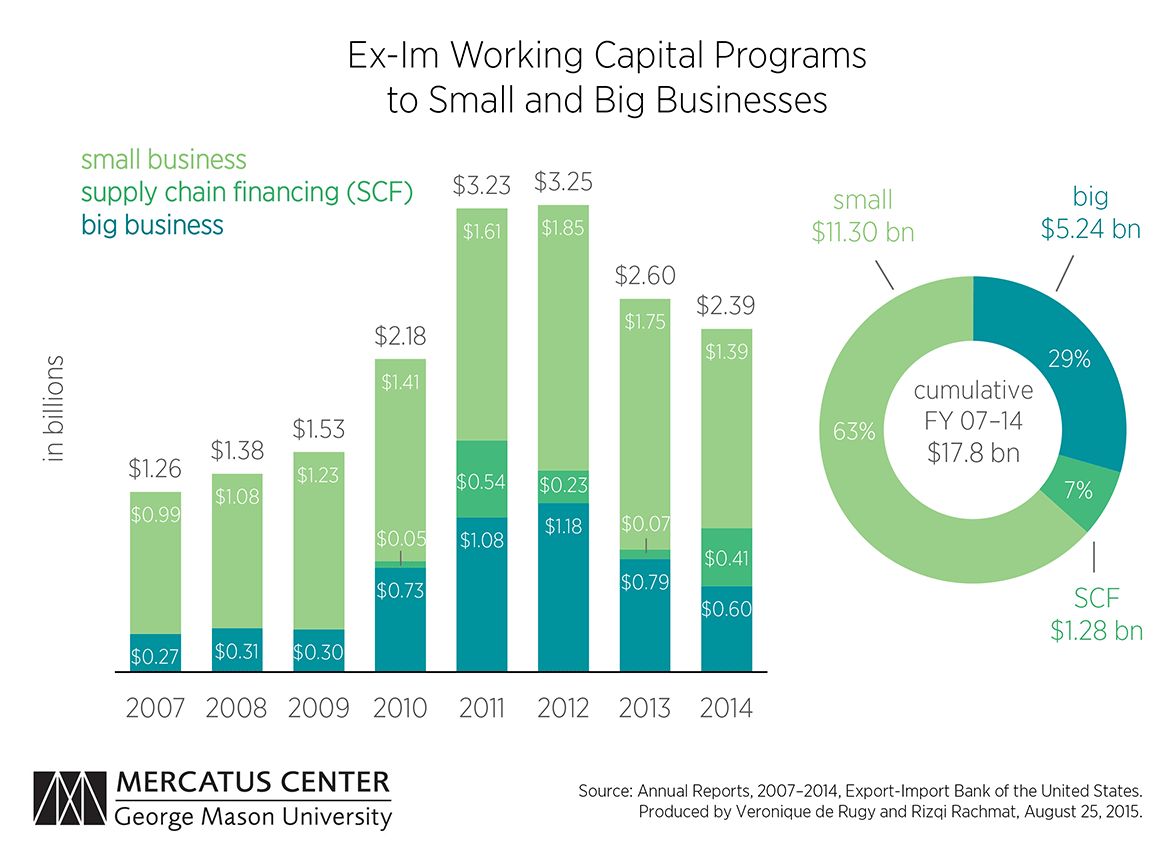

The first chart shows the annual authorized amount of working capital loans and guarantees for small business and big business. Also included are figures for the Supply Chain Finance Guarantee Program (SCF), which the Ex-Im Bank counts as benefitting small businesses even though the ultimate beneficiaries are large exporters such as Boeing and Caterpillar.

The bar chart shows breakdowns of the Ex-Im Bank’s annual working capital loans and guarantees from fiscal year (FY) 2007 to FY 2014. The amount authorized between FY 2007 and FY 2014 fluctuated from $1.26 billion in 2007 to $2.39 billion. The funding peaked in 2012 with $3.25 billion authorized that year. The data also show that every single year, large firms benefited from the working capital program directly, and they also benefited indirectly through the SCF program to the tune of $1.28 billion of working capital over the period.

The doughnut chart shows the proportion of total FY 2007 to FY 2014 working capital loans and guarantees. It shows that over the FY 2007 to FY 2014 period, 36 percent of the working capital programs benefitted large firms—29 percent directly and 7 percent through the SCF program.

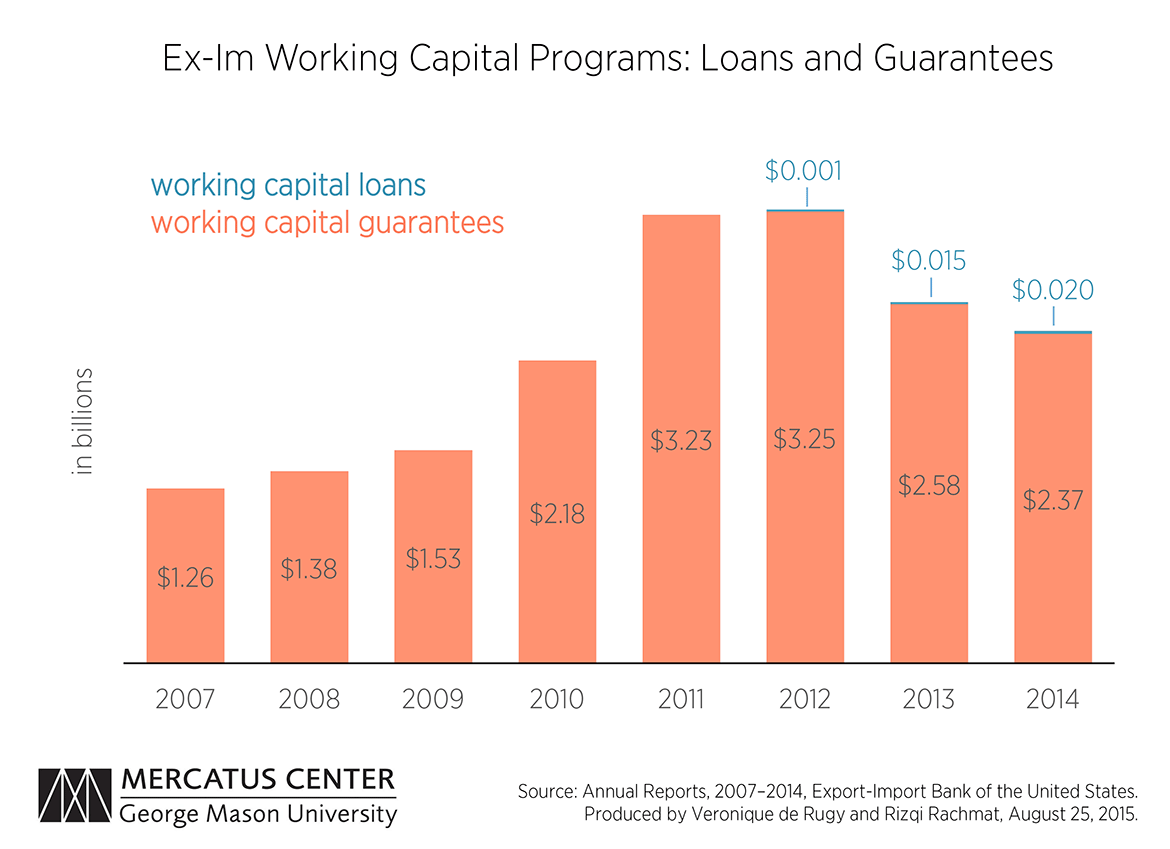

The second chart shows the annual total amount of working capital loans and working capital guarantees that the Ex-Im Bank authorized from FY 2007 to FY 2014.

The vast majority are guarantees in which the agency reimburses lenders up to 90 percent of the outstanding loan amount in the event of nonpayment. This shifts the risk from lenders—typically massive global financial institutions like PNC Bank, JPMorgan Chase, and Wells Fargo—to the taxpayers.

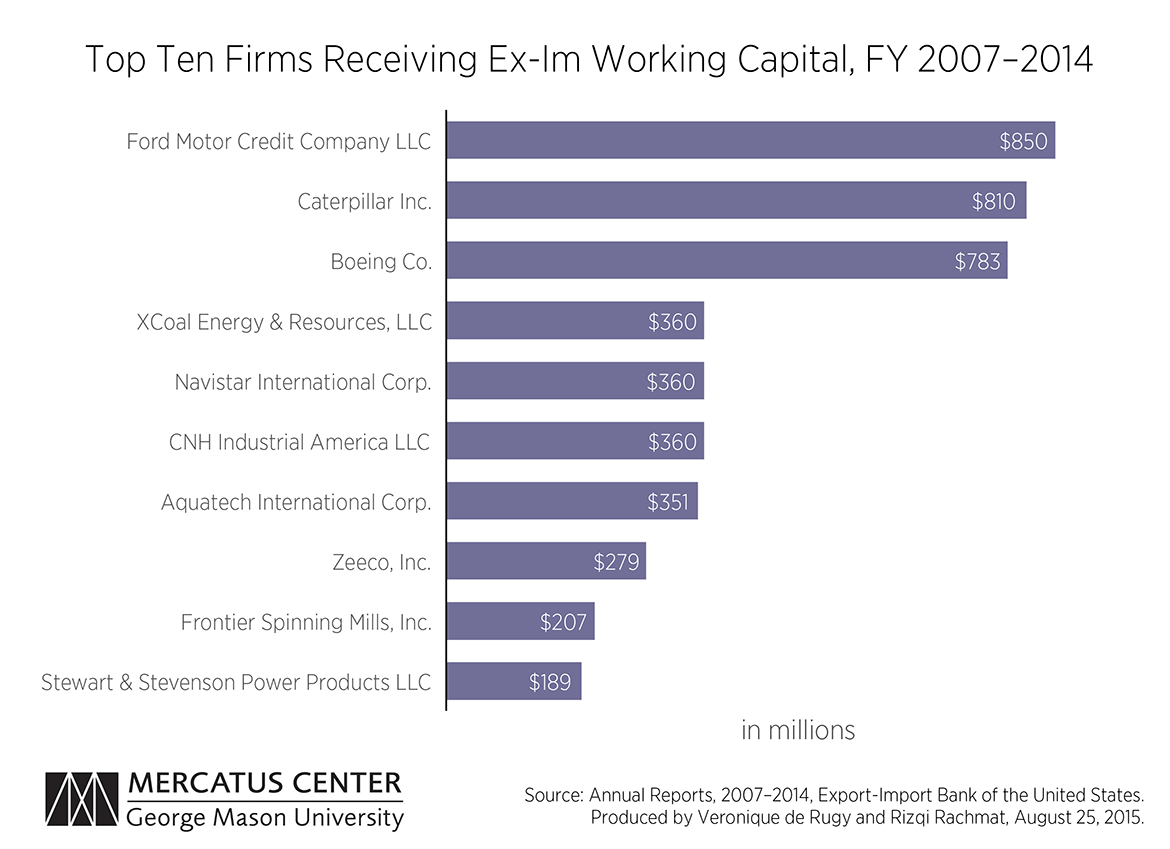

The third chart shows the top ten beneficiaries of the Ex-Im Bank’s working capital programs from FY 2007 to FY 2014.

The clear winners are large corporations like Ford, Caterpillar, and Boeing. The same names of large politically connected corporations that have shown up in our top ten Ex-Im beneficiaries of 2013 and 2007 appear in this context as well.

The good news is that this textbook example of cronyism is presently shuttered because Congress failed to reauthorize the Ex-Im Bank by July 1. The bad news is that the big corporate interests who have enjoyed its largesse over the years are committed to bringing the agency back to life. Despite the rhetoric of benefits to small businesses, policymakers would do well to remember the truth: the Ex-Im Bank’s benefits have flown primarily to large politically connected businesses.

{kind=link}