- | Monetary Policy Monetary Policy

- | Working Papers Working Papers

- |

The Iceland and Ireland Banking Crises: Lessons for the Future

The economic collapses of Iceland and Ireland after 2008 are the most severe in the developed world in recent history. This paper assesses five key differences in the causes of and responses to each country’s crisis.

Abstract

The economic collapses of Iceland and Ireland after 2008 are the most severe in the developed world in recent history. This paper assesses five key differences in the causes of and responses to each country’s crisis. On the causal side, we look at (1) the role that deposit insurance served in artificially increasing risk-adjusted returns and (2) the subsequent increase in loanable funds that bred large and unsustainable financial sectors. On the response side we look at (1) the speed, transparency, and effectiveness of the nationalization of each country’s financial sector; (2) the decision whether to bail out key financial institutions or to allow them to fail; and (3) the differences in exchange-rate structures that created different recovery paths. We conclude by drawing policy conclusions for countries with large, unstable banking sectors, notably the United States.

1. Introduction

In the fall of 2008, the Icelandic banking system collapsed, giving rise to a general economic recession and currency crisis. The size of the banking system and the severity of the events rendered both the Icelandic government and its central bank unable to save the insolvent financial system. The dire situation was mirrored 1,000 miles to the southeast, as Ireland entered into a similar banking crisis. Without a concerted effort to bail out its banking system, the Irish financial system would be brought to its knees like its Nordic neighbor’s. The sentiment of the time was captured in a common joke: “What’s the difference between Ireland and Iceland? One letter and six months.” If no bailout was forthcoming, the presumption was that the Irish tempest would turn into the Icelandic disaster. Bailouts did come in time to save the Irish banks, but not the leading banks of Iceland. Whether this saved Ireland from a worse fate is another question.

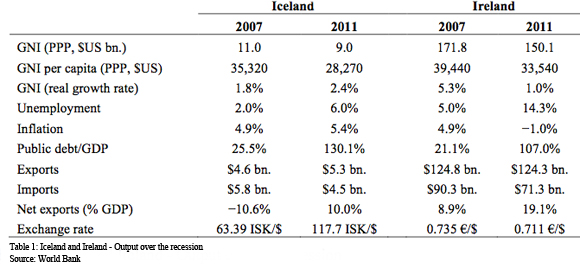

Consider the following statistics from 2007 at the peak of the boom to 2011:

Irish real output has stabilized faster, its exchange rate has remained stable, and its public debt level have been kept lower, although its unemployment rate remains high and the country has recently experienced deflation. Icelandic real GDP is rebounding after lagging for several years, and quickly turning into growth. Unemployment in Iceland remains low by European standards, and its trade balance has significantly improved as the country returns to being a net creditor.

In this paper we focus on five key differences in the causes of and responses to each country’s crisis. We conclude that each country did some things well and some things poorly over the past four years. In particular we contrast two key areas that bred financial instability leading up to the crisis: (1) the funding sources of each country—equity versus real estate loans—and the effects that the liquidity freeze of 2008 had on these funding sources, and (2) the insurance plans employed to safeguard depositors. We then turn our attention to three policy responses in the aftermath of 2008: (1) the speed, transparency, and completeness of the nationalization of some financial assets; (2) the decision whether to allow the banking sector to fail or to bail it out; and finally, (3) the differences in exchange rate structures—flexible in the case of Iceland versus fixed within the European Monetary Union for Ireland.

These five differences are crucial to understanding why some aspects of the crisis have gone right in each country, while other aspects have gone so wrong. Together they aid in providing a road map to follow as we trudge through the uncharted waters of the financial crisis. We conclude by pointing out some similarities to the American financial system, and their implications.

Related Content

- | Financial Markets Financial Markets

- | Journal Articles Journal Articles

Separating the Wheat from the Chaff: Icelandic and Irish Policy Responses to the Banking Crisis

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

European Austerity: Government Expenditures by Country

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations