- | Housing Housing

- | Data Visualizations Data Visualizations

- |

More Sales Tax Exemptions, Higher Sales Tax Rates

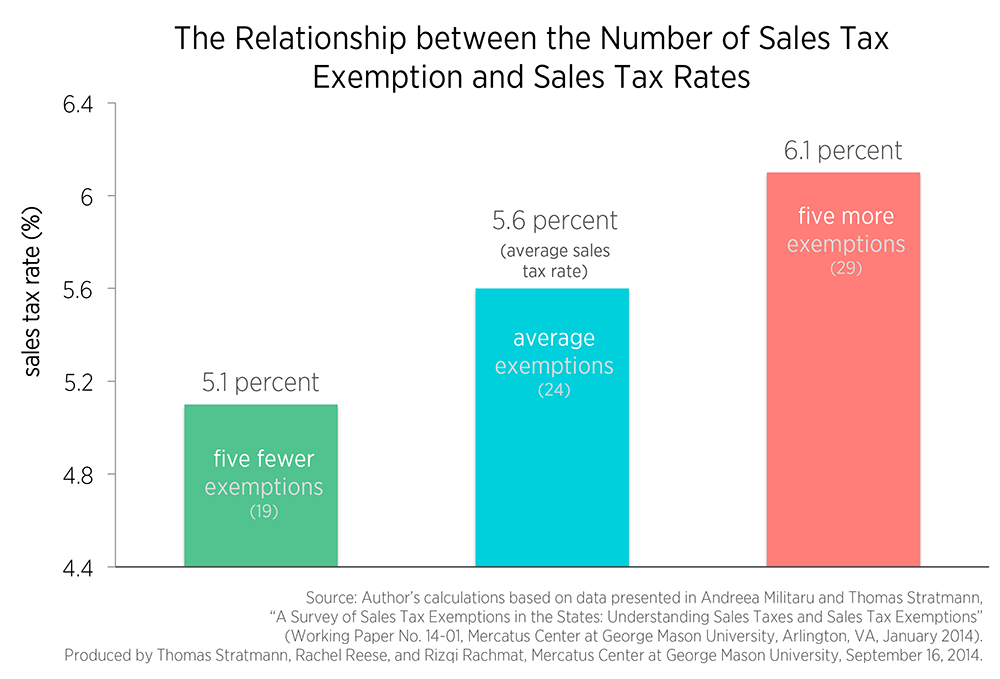

State and local governments often increase sales taxes to generate additional revenue; however, projections of added revenue tend to be over-optimistic, in part because sales tax exemptions tend to increase along with the tax rate. These charts illustrate the relationship between average sales taxes and exemptions among the states (five states without sales taxes were removed, as was Hawaii because of its complex tiered system).

State and local governments often increase sales taxes to generate additional revenue; however, projections of added revenue tend to be over-optimistic, in part because sales tax exemptions tend to increase along with the tax rate. These charts illustrate the relationship between average sales taxes and exemptions among the states (five states without sales taxes were removed, as was Hawaii because of its complex tiered system).

The average sales tax rate is 5.6 percent, ranging from 2.9 percent to 7.25 percent. The average number of exemptions is 24 and ranges from 19 to 31. The analysis suggests that the addition of five exemptions is correlated with an increase in the sales tax rate of at least 0.5 percent, and vice versa. This means that if a state has a current sales tax rate of 5.6 percent and adds another five exemptions, the state can be expected to increase the sales tax rate to 6.1 percent. Conversely, if a state increases the sales tax rate, more lobbying by special interests in that state will likely lead to five additional exemptions.

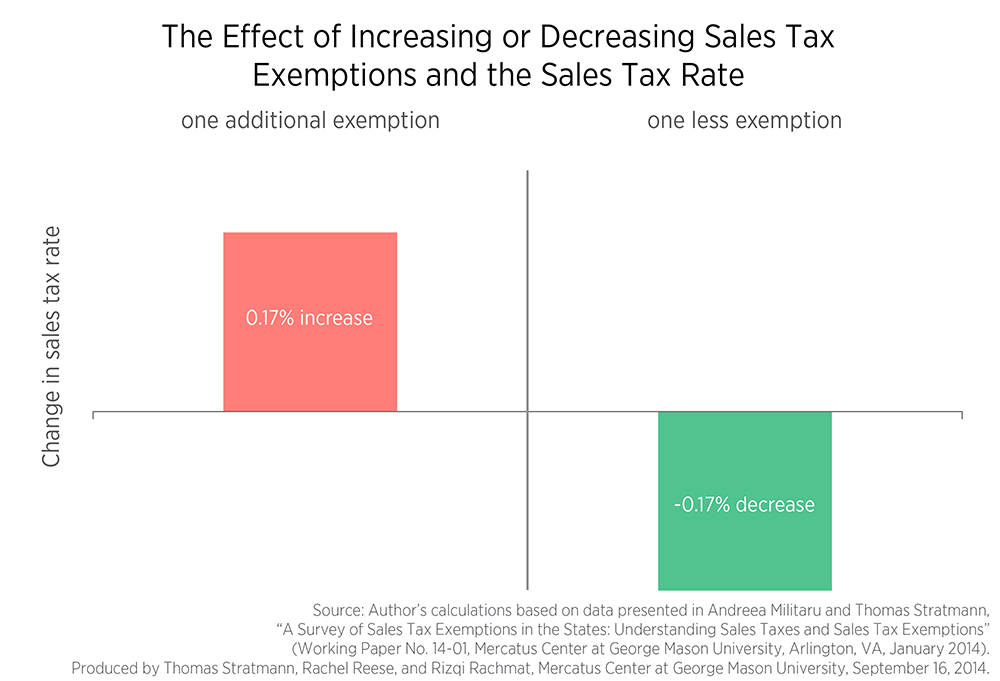

Similarly, the second chart demonstrates the effect on the sales tax rate of adding or eliminating just one exemption. The estimates indicate that a one-unit increase in the number of exemptions is associated with an increase in the sales tax rate between 0.10 and 0.25 percentage points—depending on whether a “broad” or “narrow” measure of exemptions is used.

Government agencies should consider this relationship between sales taxes and exemptions, and the unintended consequences that ensue, when making predictions. Changes in sales taxes can distort consumption of certain goods. Moreover, higher sales taxes tend to lead to increased lobbying activity, which creates additional distortionary effects on consumer choices and market transactions.