- | Housing Housing

- | State Testimonies State Testimonies

- |

Pension Reform In Pennsylvania

Testimony Before the Commonwealth of Pennsylvania House State Government Committee

In my testimony I would like to begin by discussing the reasons why Pennsylvania’s pension systems reached this point and the importance of accurate valuation in both determining a funding policy for the current DB plan and deciding how to structure a reliable retirement system for Pennsylvania’s public sector workers.

Chairman Metcalfe, Representative Josefs, and distinguished members of the General Assembly, thank you for inviting me to testify today on the subject of pension reform in the Commonwealth of Pennsylvania.

Public Sector Pension Policy in the Commonwealth of Pennsylvania

Pennsylvania’s two main pension systems, the State Employees’ Retirement System (SERS) and the Public School Employees Retirement System (PSERS) report a combined unfunded liability of $39.5 billion and funding ratios of 75 percent and 69 percent, respectively. However, on an economic basis, the shortfall in these plans increases to a total of $116 billion, leaving each system funded at 34 percent. In either case, Pennsylvania’s pension systems confront a very significant obligation to retirees. One question being considered today centers on the merits of closing down the defined benefit plan and shifting future hires to a defined contribution plan.

In my testimony I would like to begin by discussing the reasons why Pennsylvania’s pension systems reached this point and the importance of accurate valuation in both determining a funding policy for the current DB plan and deciding how to structure a reliable retirement system for Pennsylvania’s public sector workers.

This discussion of how to value a defined benefit plan is central to knowing how to choose the design of the pension plan, as the reason for the massive funding gap is driven by the underestimation of the true normal costs and contributions needed to fund SERS and PSERS. Thus the decision to shift workers to a DC plan entails also knowing the true costs of keeping the DB plans open.

The Importance of Economic or Market Valuation of Pension Plans

The crash in financial markets in 2008 is often cited as a leading cause for pension plan underfunding in the US. However, the steep decline in markets is not a cause of plan underfunding; it is instead a demonstration of a fundamental flaw in how public plans have been valued, funded, and exposed to large amounts of risk. The weakening of defined benefit plans is a direct result of a core assumption that is built into all public sector plans, that is, the discount rate chosen to value the pension obligation (or liability), and thus the amount needed to fund the liability (the Annual Required Contribution), in order to secure benefit payments to retirees.

The Importance of Selecting a Discount Rate

A public sector pension represents a promise on the part of the government to pay an employee a certain sum upon retirement, on a monthly basis, until their death based on the employee’s years of service, a measure of final salary, a benefit multiplier, and age. The payout is a guarantee. The pension as a government-backed plan is considered, “A debt of the Commonwealth, backed by the full faith and credit of the Commonwealth.” A public sector pension is a liability to the government, or, a stream of cash flows that the government as employer must pay to its employees, much like a bond. In choosing a discount rate (the interest rate) to convert the future value of that promise into a present value, what must be considered is the likelihood that the payment to the retiree will be made.

The pension is risk-free from the vantage point of the worker. It is a near-certainty that the government will not opt to default on this payment. Thus the correct discount rate to use is one that matches the risk and the timing of the pension cash flows. In this case it is the yield on 15-year Treasury bonds (15 years because this is the midpoint of that stream of cash flows). That rate is currently 2.5 percent. SERS assumes a discount rate of 8 percent and PSERS, a rate of 7.5 percent. The result is that the lower discount requires a higher contribution in the present to fund future benefits, presenting policymakers with a very intimidating budgetary reality.

It must be stressed that there is only one liability, not many possible liabilities based on many possible discount rates. Accounting assumptions that shift the timing of payment or seek to lower the size of the present value only serve to artificially suppress the underlying economic reality. In other words, the economics will catch up with the accounting eventually.

As M. Barton Waring notes (2012), “Best practices for estimating a discount rate, which are well established in all fields except actuarial pension finance treat the discount rate as identical to the opportunity cost of capital – that is the market cost of borrowing money or using capital on a basis that reflects all fully-diversified, market-related risks.”

Unfortunately, current guidance provided by Government Accounting Standards Board (GASB) 25 and Actuarial Standards of Practice (ASOP) 27 bases the selection of a discount rate on assumed asset returns. However, according to well-established principles of economics, the return on plan assets is absolutely irrelevant to the value of the liability. Assets and liabilities should be kept separate for the purpose of valuation.

This practice – valuing the pension liability based on assumed market returns – has led to a tragic outcome for defined benefit plans across the United States. It has resulted in sudden funding gaps emerging, and the inexorable pressure of immediate higher than anticipated contributions. There is a reason for this: using expected asset returns understates the value of the liability leading to an underestimation of contribution rates – a problem that is revealed when the assets fail to perform as well as expected.

The flawed discount rate assumption has had a negative effect on asset management, contribution policy, and defined benefit plan design in the public sector.

Effects On Asset Management

Several behaviors result from valuing liabilities based on expected asset returns. Each creates poor incentives for responsible fund management. Firstly, plan managers have a greater incentive to take on more investment risk in a gamble to achieve higher returns on plan assets. Public plan managers have embraced more risk over the course of the past 20 years. In 1990, 40 percent of public sector pension assets were held in equities. This rose to 70 percent in 2006. That is roughly 10 percent higher than the allocation of pension assets to equities in private pension systems. This behavior can be seen in the SERS investment portfolio which has put of 26 percent of its assets in alternatives.

This behavior – seeking out more risk in in asset portfolio – is an artifact of improper accounting, which implies it is possible to guarantee a certain, risk-free, benefit with volatile investments. However, exposure to volatility lessens the likelihood that there will be enough in the plan to pay benefits when they are due. The majority of a plan’s obligations are payable over the next 15 years. Even if plans accurately predict market returns over a long period, they must pay out benefits over the short term when average market returns are more uncertain. There is a significant probability that a “fully-funded” plan would be unable to make its obligations even if the plan accurately projects average market returns.

In sum, discounting pensions at the expected rate of return on investments implies the entire return is available to pay future benefits – and makes no allowances for losses. It implies that by taking on more investment risk, the plan’s funded status is improved.

This logic is seen in SERS Comprehensive Annual Financial Report (CAFR). The fund recorded an 11.9 percent gain in 2010, exceeding the plan’s anticipated 8 percent return. The CAFR posits that while the portfolio underperformed in the short-run with a 10-year return at 4.8 percent, longer run returns are more robust. The 20-, 25-, and 30- year returns are 9.1 percent, 9.3 percent and 10.1 percent respectively.

The expected value of a return is not necessarily the return that the state will realize. When a portfolio is invested in risky equities to pay a liability that is risk-free “a substantial danger exists that the portfolio will underperform the liability and leave it underfunded. This increases the possibility of default, or requires higher contributions. Equities have a higher rate of return than bonds because they have a higher risk, or probability of disappointment than risk-free assets.”

This can be stated as follows: “an investor does not ‘get’ the expected return, they get an uncertain and highly random draw from an increasingly wide distribution of possible returns.” In other words, two decades of good luck in the market can be followed by two decades of bad.

Funding Policy: Low, Deferred and Capped Contributions

The second problem presented by valuating plan liabilities based on expected assets returns is that it produces an Annual Required Contribution (ARC) that is too low, and insufficient to fully fund the benefit. That is, even when sponsors are contributing the full ARC, they are contributing too little. Since the liability is undervalued, so are the contributions needed to fund the benefit. In the case of Pennsylvania, Joshua Rauh and Robert Novy-Marx calculate that Pennsylvania’s current actuarially required contribution of $2.8 billion a year should be $10.5 billion and that this will required an increased contribution of 35.8 percent of payroll, or 15.2 percent of tax revenue.

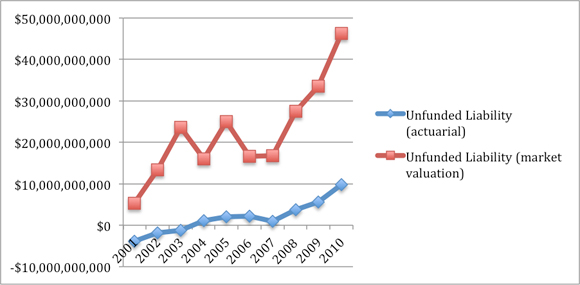

Figure 1 shows the difference between the unfunded liability on an actuarial versus a market basis. The mixing of plan assets and liabilities has produced another moral hazard problem in funding policy – it has given sponsors the illusory impression that plans are overfunded during boom years. Plan sponsors have set contribution policy according to market performance.

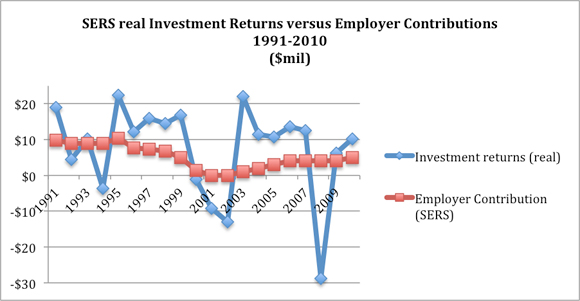

This is clearly seen in SERS. High investment returns in the 1990s triggered a downward trend in contributions. The contribution rate in 1980 and 1984 was 14 to 18 percent of payroll. Strong asset returns tracked with a marked decline in contributions. As a result of historically high market returns in the late 1990s Pennsylvania zeroed-out its annual contribution for two years (2000 and 2001). As SERS began to absorb the effects of the technology bubble bursting, plan contributions began to increase again, but only modestly.

A decision was made with Act 2010-120 to artificially cap contributions. The purpose was to lessen the immediate budgetary impact of rising pension costs and to push those costs into the future. But these costs have not been erased, only shifted forward.

For example, in the SERS system, actuaries estimate the ARC is 18.93 percent of payroll for 2010. Most of that, 14.85 percent, represents the amortization of the unfunded liability. The remaining 4.08 percent is the normal cost of the plan. However, as a result of Act 2010-120, that year’s contribution is artificially capped at 8 percent. The rate calculated for PSERS is 22.51 percent of payroll. Again, Act 2010-210 limits this contribution in FY 2012-2013 to 12.36 percent of payroll, which has the effect of deferring part of that year’s contribution to the future.

The effect of this policy is now being felt in the sudden expected spikes in annual contributions to both SERS and PSERS. And again, these growing contributions are still underestimating the amount needed. Figure 2 shows the inverted thinking that improper valuation gives rise to: funding policy and behavior that is influenced by market returns rather than by the guarantee offered by the government to pay out the liability.

What is the Cost of Moving to a Defined Contribution Plan?

In considering a shift to a DC plan, first policymakers must work with the right set of numbers. Otherwise they are comparing apples and oranges. To begin, actuaries should estimate the true cost of the DB plan based on the risk-free rate, and then determine the true normal costs to fund the plan. How do these costs compare to the cost of the DC plan? A 2002 study produced for the Commonwealth’s Public Employee Retirement Commission found that the annual cost of the DB plan averaged 14.9 percent, much lower than the estimated 20 percent of payroll that a DC plan might require. However this is a faulty comparison, as the normal cost of the DB plan is underestimated based on a high-risk discount rate. Again, by way of example, Pennsylvania’s actuaries estimate that SERS contribution rate for 2010 is 18.93 percent of payroll, and the PSERS plan is 22.51 percent of payroll. The state is choosing to pay only a portion of that. However, Novy-Marx and Rauh estimate using a risk-free rate, the true cost to fund the plan would require an increase of 35.8 percent of payroll.

The question under consideration today is what are the costs associated with shifting to a DC plan. I will mention a few principles to consider in evaluating the costs to Pennsylvania’s government and taxpayers.

- Switching to a DC plan does not save money in the short-run as both the DB plan and the DC plan must be funded.

- Switching to a DC plan shifts risk away from taxpayers and onto the workers who are participating in a DC plan. It also provides the worker with greater mobility as retirement savings are portable in a DC plan.

- The government must make its annual contribution to the DC plan thus mitigating the public choice problems and moral hazard problems present in the current DB plan.

- The annual contribution to the DC plan is not “more expensive” it is simply “more transparent” than the DB plan. This is only because currently DB plans are misvalued and the amount needed to fund the plans underestimated. Unless economic valuation of the DB plan is performed, which includes calculating the true normal costs and ARC, DB plans will artificially appear to be cheaper.

- Whether Pennsylvania chooses to stick with DB plans or shift to DC plans, the benefit for the DB plan must be funded. Underfunding presents a real risk to taxpayers and to beneficiaries. Policies that attempt to suppress contributions merely shift the bill forward and create greater funding problems for the future.

- DB plans can only function if the moral hazard problems presented by the current accounting and public choice problems are eliminated and this entails market valuation.

Thank you for the opportunity to testify on this important subject. I look forward to your questions.

Figure 1. SERS Actuarial Unfunded Liability vs. Market Unfunded Liability 2001-2010

Figure 2. SERS Real Investment Returns vs. Employer Contributions (1991-2010, $mil)