- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

Principles for Analyzing Distribution in Regulatory Impact Analysis

Federal regulatory agencies have been required to produce a regulatory impact analysis (RIA) for major regulations since the early 1980s. The analysis should include an estimate of the expected benefits and costs of the regulatory action (a benefit-cost analysis, or BCA) as well as a description of the parties who are likely to receive those benefits and incur those costs. The latter part of an RIA is known as a distributional analysis, and is not part of a classic BCA. Distributional analysis explores how wealth is redistributed as a result of policy decisions.

Federal regulatory agencies have been required to produce a regulatory impact analysis (RIA) for major regulations since the early 1980s. The analysis should include an estimate of the expected benefits and costs of the regulatory action (a benefit-cost analysis, or BCA) as well as a description of the parties who are likely to receive those benefits and incur those costs. The latter part of an RIA is known as a distributional analysis, and is not part of a classic BCA. Distributional analysis explores how wealth is redistributed as a result of policy decisions.

Nevertheless, a multitude of executive orders (EOs) and laws emphasize the importance of assessing distributional consequences of policies. For example, the current executive order governing the regulatory review process explicitly mentions “distributive impacts” and “equity” as issues analysts should consider. Other EOs prompt agencies to focus on environmental justice, children, and American Indian tribes, and laws are in place to protect small entities (including small businesses and governments). Employment gains and losses are also distributional consequences of policies, and the Office of Management and Budget (OMB), which sets guidelines for how agencies conduct economic analysis of regulations, further emphasizes distributional concerns.

With the exception of the legally required analysis for small entities (called regulatory flexibility analysis), agencies rarely conduct a general distributional analysis of the parties likely to receive benefits and bear costs. Because many regulations concentrate benefits for small groups while disbursing costs, distributional analysis can help to highlight inequities hidden in BCA. Those who incur the most net costs relative to their income are often those who are less well off, meaning that policies all too often have a regressive effect. Given the seemingly endless growth in regulations, it is time agencies focus more on the distributional repercussions of their rules.

Does Benefit-Cost Analysis Consider Equity?

BCA is a tool that analysts use to assess the efficiency of various policy alternatives. A policy maximizes efficiency if the benefits of the chosen policy exceed the costs by the largest amount among all possible policy options. Many economists believe efficiency and equity are distinct concepts that should be considered separately, but in fact equity is actually an inseparable component of BCA. Just as all citizens should receive equal treatment under the law, economists producing BCAs say that all citizens with standing in a BCA receive equal treatment in that analysis. BCA is based on a normative ethical judgment that says the value of one additional dollar of income is equal to all citizens, regardless of whose pocket that dollar goes into. In economics jargon, we say there is constant marginal utility of income across citizens. In this way, equity and BCA are inexorably intertwined.

Some analysts have sought to change the role of equity in BCA; analysts have, for example, assigned weights to different categories of people. These analysts say that if a regulation transfers money from wealthy people to less wealthy people, analysts should give each group a different weight so that even a pure transfer between two people can be seen as a benefit. Transfers of goods from one party to another are typically neutral in BCA because one person’s loss is another person’s gain, with no impact on the overall calculation of “net benefits” (i.e., benefits in excess of costs). Even some government agencies, such as HM Treasury in the United Kingdom, recommend using a weighting scale like this. One problem with weighting schemes is that identifying what the weights should be is an arbitrary decision that is hard to justify on ethical grounds because analysts must treat some citizens as deserving more weight than others.

A better approach is for analysts to present simple, straightforward information to decision makers, i.e., who gets what and who loses what, and to allow the decision makers to make the necessary political decisions about the appropriate course of action. The following principles can help analysts achieve this neutrality when analyzing distributional concerns in RIAs.

Principles for Analyzing Distribution in Regulatory Impact Analysis

First, distributional analysis should be part of an RIA but kept separate from a BCA. A BCA tells decision makers whether the benefits of a proposed policy exceed the costs, no matter how they are distributed. A distributional analysis illuminates who receives those benefits and costs (and transfers). Keeping these analyses distinct within the framework of an RIA will ensure that decision makers are aware of these different decision inputs.

Second, analysts should identify groups that are likely to be impacted by the regulation. Distributional analysis may not always be necessary; however, if any of the groups identified as groups of concern in executive orders or laws are impacted by a regulation, this might signal to analysts that further distributional analysis is necessary.

Third, analysts should determine the degree to which a regulation is likely to have regressive or progressive effects. There are several ways that regulations can be regressive. Some regulations impose costs in excess of benefits for the poor, while providing benefits in excess of costs to higher-income people (an example of this appears later in this report). Next, some regulations impose net costs on all groups, but the net costs to lower-income individuals represent a higher fraction of their incomes than the net costs to other groups. For this reason, calculating net effects of policies as a percentage of average subpopulation income is helpful.

There will also be cases where regulations create net benefits to low-income individuals, but the costs the poor pay represent a disproportionate share of their income relative to the costs other groups pay. While perhaps not technically regressive, this category may be undesirable because it redistributes wealth in such a way that lower-income people disproportionately bear the cost of regulation. Similarly, when the benefits of a policy represent a larger fraction of income for wealthy households relative to other groups, regulations are being designed in a manner that caters more to the preferences of the wealthy. This too may be undesirable in some cases. There may also be progressive regulations, which force the wealthy to bear a disproportionate share of the costs, while benefits accrue primarily to the poor.

Fourth, transfers should be included in a distributional analysis. While pure transfers do not affect overall benefits or costs, transfers may still have an important role to play as part of a distributional analysis, especially transfers going to groups that have been singled out for particular consideration.

Fifth, analysts should consider how the tolerance to bear regulatory costs varies across subpopulations. All groups, and especially the poor, have finite resources. If agencies presume a poor person can tolerate paying the same amount for a policy as a wealthy person, policies are likely to make the poor worse off. The level of cost tolerance can be estimated by examining how willingness to pay (WTP) for regulatory benefits changes across groups. For instance, the Environmental Protection Agency and Department of Transportation use estimates of WTP that vary by income for changes that occur across time. Applying this methodology to current citizens for the purposes of distributional analysis also makes sense. In many (but not all) cases, the poor are likely to have a lower tolerance for costs than the wealthy. This is because they are less willing and less able to pay for most benefits of regulation.

Some might be tempted to use population average estimates of WTP across groups in distributional analysis. This is reasonable in cases where a vulnerable population experiences benefits of a regulation, but does not bear any of the costs. Harvard law professor Cass Sunstein gives the example of a disabled worker who pays nothing to make a workplace accessible to the handicapped, but nonetheless enjoys benefits from this policy. If such a worker has a low WTP, based on a low ability to pay, using an average of the entire population’s WTP may make sense. Importantly, this is only true because the individual bears none of the cost. In cases where low-income individuals are forced to pay for regulatory benefits with their own resources, such as when a government mandate improves product quality (while also increasing the price of the product), it makes no sense to value policies higher than a person would voluntarily pay for them. Using population averages in this latter scenario will distort economic analysis, making it more likely that regulations will force people to pay more for policies than they value them to be worth.

In cases where WTP across subpopulations is unclear, say due to data limitations, population average WTP might be used, but a sensitivity analysis, used to describe uncertainties in analysis, should be conducted to determine the degree to which this assumption, when relaxed, changes outcomes across subpopulations.

An Example

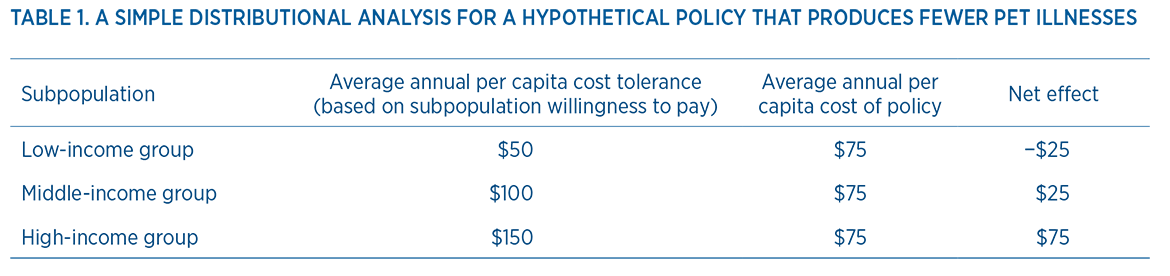

A simplified hypothetical example of a distributional analysis illuminates these principles further. Imagine that society comprises three types of people. One group consists of high-income people, one group is low-income people, and one group is in the middle. A policymaker is considering whether to implement a regulation intended to reduce contamination in pet food. Let’s say the policy produces a single outcome: fewer pet illnesses. Now, let’s assume people in the wealthy group are willing to pay on average $150 per year to ensure their “designer dogs” don’t suffer salmonella poisoning. The middle-income group will pay on average $100 to protect their golden retrievers, and people in the low-income group will pay up to $50 per year for their mixed-breed dogs. The costs of the policy may fall on pet food producers initially, but we will assume that in the long run all costs are passed from producers to consumers and spread evenly across the three groups.

As a first step, the analyst concludes that because some purchasers of pet food are low-income individuals, a distributional analysis is necessary. If these groups consist of identical numbers of individuals, the analyst determines that the total benefits of the proposed policy are likely to exceed the total costs. The analyst could simply multiply the averages for each subpopulation by the number of individuals in the group and take the sum of these values to obtain this information. In theory, the winners of this policy could compensate the losers and everyone would still be better off than they were before the policy was put in place. This type of compensation rarely, if ever, occurs. In American society with millions of individuals and businesses, transaction costs are likely to make it too difficult to identify and redistribute between the winners and losers of policies, particularly given the current number of regulations passed each year.

As described above, a well-done distributional analysis will identify the subpopulations a policy affects and present information about their various measures of WTP for regulatory benefits. This allows analysts to determine a unique cost tolerance for each group. Notice that we do not assume that the average per capita cost tolerance across the entire population (in this case, $100) applies to low-income individuals. A poor person generally has a lower willingness and ability to bear costs than a wealthy person. In this example, the low-income group is only willing to pay up to $50 on average for the policy. This is the level at which the members of this group value the policy according to their own preferences and situations, not according to the analyst’s preferences. The typical person in this group is made worse off in our example because he or she might take the $75 spent complying with the regulation and put it toward other more highly valued uses, such as a home security system, healthier food, day care for his or her children, or whatever else he or she cares about. It is not the analysts’ job to question why people might prefer paying for some items (e.g., a home security system) and not others (e.g., complying with a regulation). Each individual in society must make these decisions for themselves and analysts simply report this behavior.

This example is meant to be a simplified version of a distributional analysis. It is not a BCA, which looks at cumulative effects on society and would therefore rely on population average values. As mentioned above, population averages might be used in distributional analysis in instances where a subpopulation bears no cost and has a limited ability to pay for the policy. BCA also ignores transfers, which aren’t included in table 1 but generally should be considered. A more detailed distributional analysis should also convert net effects of the policy into percentages based on the average annual income of each subpopulation. This allows for more meaningful comparison across groups. Employment effects might also be considered. For example, this policy might increase employment for monitors while simultaneously reducing employment for other types of pet food workers.

The Role of Decision Makers

RIAs are conducted to inform decisions made by those who are elected or appointed to make decisions. The final decision will involve considering many different factors, including economic efficiency, legal constraints, public opinion, politics, and the distribution of wealth and income.

Decision makers might want to adhere to a decision rule that says analysts should evaluate benefits and costs to those below a particular threshold (e.g., the poverty line) distinctly from the benefits and costs to society more generally. Such a rule might state that only those policies that make both groups better off may be adopted. A similar rule might stop regulations from being adopted that exacerbate income or wealth inequality. These judgments should be made by decision makers who are accountable to the public and to elected representatives of the people, not by analysts. In order to avoid appearing politicized or biased, analysts must provide descriptive information and refrain from incorporating opinions about fair distribution of wealth into their analysis. Those decisions belong entirely to parties more accountable to the public.

Conclusion

Recent research suggests agencies rarely conduct general distributional analysis, and when they do, it is often incomplete. Agencies fail to conduct proper analyses despite executive orders and laws that repeatedly draw attention to the importance of the distributional effects of regulations. When preparing RIAs, agency analysts should keep distributional issues separate from issues of economic efficiency, so as not to confuse decision makers about these different decision inputs. Furthermore, analysts should not forget that equity is already a foundational principle of BCA. It is their job to present information about distributional effects of policies, while leaving value judgments about what is a fair distribution of wealth to others who are more accountable to the American people.

Related Content

- | Regulation Regulation

- | Federal Testimonies Federal Testimonies

OIRA Alone Could Not Achieve President Carter's Goals

- | Regulation Regulation

- | Working Papers Working Papers

Reforming Regulatory Analysis, Review, and Oversight: A Guide for the Perplexed

- | Regulation Regulation

- | Working Papers Working Papers

Assessing the Quality of Regulatory Analysis

- | Regulation Regulation

- | Research Papers Research Papers

21st Century Regulation: Discovering Better Solutions to Enduring Problems