- | Academic & Student Programs Academic & Student Programs

- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

The Tax Exclusion for Retirement and Pension Plans

The US federal tax code contains a number of provisions designed to encourage individuals to save for retirement. These provisions allow individuals to avoid or defer taxes if they choose to set aside a portion of their income for future consumption. When all of these provisions are combined, they are the second largest “tax expenditure” category as defined by the Joint Committee on Taxation. The exclusion of retirement savings from taxation causes some economic distortions, which we will discuss in this paper. However, unlike some other tax expenditures, there is a strong economic rationale for not taxing savings. Higher rates of investment lead to higher rates of economic growth, and it may be sound policy for the tax code to encourage this behavior, even after considering the economic costs. Excluding retirement income from taxation may also make the tax system more efficient, even though most other tax expenditures reduce efficiency.

The US federal tax code contains a number of provisions designed to encourage individuals to save for retirement. These provisions allow individuals to avoid or defer taxes if they choose to set aside a portion of their income for future consumption. When all of these provisions are combined, they are the second largest “tax expenditure” category as defined by the Joint Committee on Taxation. The exclusion of retirement savings from taxation causes some economic distortions, which we will discuss in this paper. However, unlike some other tax expenditures, there is a strong economic rationale for not taxing savings. Higher rates of investment lead to higher rates of economic growth, and it may be sound policy for the tax code to encourage this behavior, even after considering the economic costs. Excluding retirement income from taxation may also make the tax system more efficient, even though most other tax expenditures reduce efficiency.

When an employer chooses to compensate employees with contributions to a retirement or pension plan, rather than with wages, that compensation is not taxed in the current year. Instead, the income will be taxed in the future when employees choose to withdraw it, presumably when they are in a lower tax bracket. Similarly, investment income in tax-protected plans, such as dividends and capital gains, is not taxed until it is withdrawn.

Traditional employer-sponsored, defined-benefit pensions were the first major plans of this type to be excluded from taxable income, but over the years many other similar kinds of retirement savings have also achieved tax exclusion. Important additions were Keogh plans for the self-employed, contributions to Individual Retirement Arrangements or Accounts (IRAs) beyond employer-sponsored plans, and defined-contribution plans set up by the employer, such as 401(k)s. While these programs have important technical differences, the basic economic function is the same: contributions are made with pre-tax income and grow tax free, and the tax is paid in the future when withdrawals are made. The more recent Roth IRA operates differently from the rest, as it is funded with post-tax dollars and only the gains are tax free, but the intended economic effect of encouraging retirement savings is the same.

These exemptions result in a loss of revenue for the federal government. The Joint Committee on Taxation estimates that in FY 2013, about $117.2 billion in income tax revenue was not collected from the “net exclusion of pension contributions and earnings,” and the Congressional Budget Office has a slightly higher estimate of $137 billion once the forgone payroll tax revenue is included.1 While much of that tax revenue is simply deferred, rather than avoided, the lost payroll tax revenue (i.e., Social Security and Medicare taxes) which employers would have paid on wages is completely forgone. These estimates place the exclusion of retirement savings as the second largest tax expenditure, behind only the tax exclusion of employer-provided health insurance.2

Do Tax Incentive Increase Savings?

A primary question on the tax exclusion of retirement savings is whether they encourage individuals to save more than they otherwise would. The primary economic benefits associated with this tax exclusion can only be achieved if savings increase on net. The macroeconomic benefit of an increase in net savings is greater long-run economic growth from more capital accumulation. The potential benefit to individuals is the long-run increase in savings if, for behavioral reasons, they will save too little from their own perspective.3 While the same result might be achieved by mandating more saving for retirement, perhaps by increasing Social Security taxation and benefits, the tax exemption may be a more attractive policy because it does not involve direct taking and giving but merely encourages citizens to provide for their future retirement.

For there to be an increase in net saving, savers actually have to decrease their current consumption and standard of living in lieu of future consumption and standard of living. Because of this condition, the incentives provided by the tax deferral may not encourage genuine savings. Instead, it may merely encourage deposits and contributions into the account in ways that don’t require reducing one’s present standard of living. Some individuals probably would have saved for retirement even without the tax incentive; thus, looking at the aggregate amount deposited in these accounts is misleading. As a result, we need to investigate how much savings increased as a specific result of the tax benefit. The Journal of Economic Perspectives devoted a symposium to this question with contributions from the leading scholars in this debate. While the empirical evidence is mixed, there does seem to be strong evidence that there is some net increase in savings from tax incentives, even if the magnitude is debated.

Other Tax Exclusion Concerns

While it is important to know whether a tax exclusion has a positive effect on savings, that alone is not enough to justify a tax policy. The costs of the economic distortions introduced by the policy must also be considered. One cost may be that individuals put their savings in forms that are different from what they would choose independent of these incentives. Individuals with savings in the form of 401(k) accounts have much less freedom to choose their investments than those with savings in traditional brokerage accounts, and those with traditional defined benefit pensions have essentially no choice in how their assets are invested. This could lead to serious principle-agent problems between employers and employees, with employers or their chosen brokerages not making the best investment decisions from the perspective of the employees.

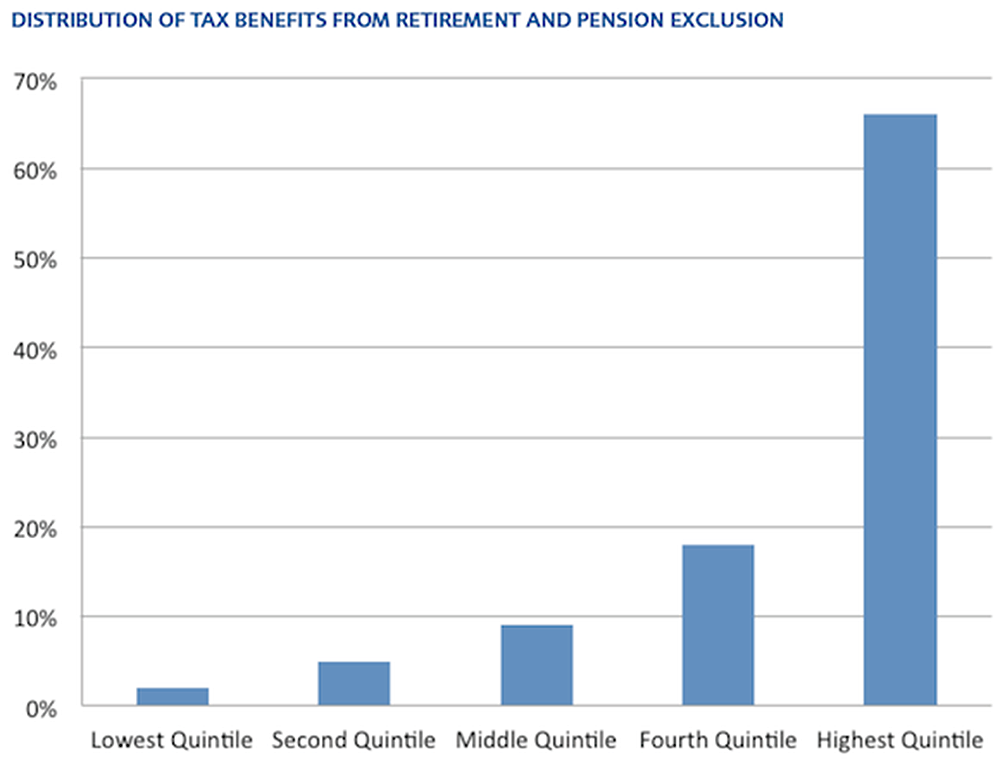

Another concern is that most of the benefits of the tax treatment of retirement savings accrue to those with the highest incomes. Toder, Harris, and Lim of the Tax Policy Center estimate that about 80 percent of the benefits for tax incentives for retirement savings go to the top income quintile.5 Those in the top income quintile almost always benefit the most from tax expenditures, largely due to the fact that they pay the most taxes; however, the 80 percent benefit for this category of tax expenditures is higher than other major categories, such as the mortgage interest deduction (about 68 percent goes to the top quintile) and healthcare-related tax expenditures (about 42 percent goes to the top quintile).

Can a Loophole Make the Tax System More Efficient?

While tax expenditures or “loopholes” are generally regarded as making the tax system less efficient overall, the exemption for retirement savings may be an exception. In fact, this exemption may make the tax system more efficient both by making the current system function more like a consumption tax and by partially correcting the double taxation of capital within the current tax code.

Since individuals can choose when they wish to realize the tax by delaying consumption, this may very well be a desirable feature of tax incentives for retirement savings. A tax on consumption is generally more economically efficient than one on income since it does not discourage production.6 The Congressional Budget Office even admits that it may not make sense to count this category as a tax expenditure: “because a consumption tax would exclude all savings and investment income from taxation, the exclusion of net pension contributions and earnings would be considered part of the normal tax system and not a tax expenditure.” 7

However, this desirable feature is only obtained by adding yet another layer of complexity to the income tax. If a consumption tax is what is desired, then proponents should make their goal changing the income tax into a consumption tax rather than creating unnecessary complexity within the system that we have. Nevertheless, we may consider this layer of additional complexity a second-best solution in a world where most federal revenue is still derived from taxes on income.

A second efficiency benefit of this tax exemption is that it serves as a partial correction for the current double taxation of capital income in the United States. With the highest corporate tax rate in the developed world, the United States must be particularly attentive to the impact of its tax system’s effect on capital formation.9 Currently, capital income is taxed when corporations earn income, and the same income is taxed again when it is paid to individuals in the form of dividends or capital gains. The exclusion of taxes on retirement income, specifically dividends and capital gains, means that the double taxation is eliminated for some capital income. In the absence of a corporate income tax, this tax exemption may make less economic sense, but given current corporate taxes in the United States, it has a sound economic logic.

Conclusion

In the end, the federal tax code allows for a deferral of income tax on contributions to a retirement or pension plan, which provides an incentive for people to save for their retirement. People choose to save more because they probably will be in a lower-income tax bracket during their retirement and also because they will be able to accrue the benefits of invested funds that would have otherwise been taxed away. Despite the complexity that this deduction adds to the tax code and some economic costs, this deferral brings the income-tax function closer to a more economically efficient consumption tax. It also mitigates the problem of the double taxation of capital for the tax-deferred contributions.

To speak with a scholar or learn more on this topic, visit our contact page.