- | Corporate Welfare Corporate Welfare

- | Policy Briefs Policy Briefs

- |

Land Assembly without Eminent Domain: Laboratory Experiments of Two Tax Mechanisms

Our laboratory experiments o er compelling evidence that eminent domain is not necessary to facilitate land assembly.

Introduction

Eminent domain, the power granted to governments to take property for public use, is increasingly viewed by many policymakers and policy analysts as a necessary evil to assemble multiple properties for development. For example, suppose a real estate developer wants to build a hotel on 20 contiguous parcels of land. The developer needs all 20 properties to build the hotel, but when she submits bids to the 20 property owners, 19 accept her offer and 1 does not. The owner refusing to sell grew up in his current home and claims that he intends to live out his life there.

Economists refer to this predicament as the “holdout problem,” and the developer has several options to address it. She could offer the owner who did not accept her offer more money, but he may still refuse to sell because of the sentimental value of the property. Another option is to look for another location for the development, but the developer may see the current location as the best spot. This leaves her with a third option: approach the city council and ask them to invoke eminent domain on her behalf, forcing the holdout to sell his property and vacate the premises.

The city council faces a dilemma. Market economies require secure property rights, but in some cases one person’s property rights may deny the community economic benefits, such as jobs, beautification, and greater tax revenue. Should the city council refuse these benefits so the owner can stay in his childhood home? The owner may be feigning his sentimental attachment to claim a bigger share of the surplus from the development. Should the council evict him and hope the developer fulfills her promises? After all, the developer may be overstating the economic benefits of the development in a bid to get the city council on her side. This has happened on multiple occasions and resulted in litigation, such as in the cases of Kelo v. New London and Poletown v. Detroit.

Alternatives to Eminent Domain

Economists have proposed a number of alternatives to eminent domain. Two such proposals involve changing tax policy. We refer to them as revealed assessment and declared assessment.

Revealed assessment. Under revealed assessment, a developer makes offers to property owners and reports these offers to the government. If the owner refuses the offer, then he has revealed that the property is worth more to him than the amount that was offered. Consequently, the taxable value of his property is reassessed to equal the highest refused offer. Thus, strategic holdout results in a financial penalty. Theoretical work by Thomas Miceli, Kathleen Segurson, and C. F. Sirmans shows that this tax mechanism may lead to efficient land assembly. That is, the developer will succeed in assembling the properties only if she values the assembly more than the owners do. This result holds provided that the value of the development—divided by the number of properties—exceeds the highest value that any owner places on his property.

Declared assessment. Under declared assessment, every property owner declares a price for his property to the government. The government uses a tax formula to assess a property tax based on the declaration. If the government entity—or another designated entity—offers to buy the property at the declared price, the owner is required to sell. Florence Plassmann and Nicholas Tideman have shown that if the tax formula is constructed so that the marginal property tax rate is always equal to the likelihood that a developer will wish to purchase the land, then it is in the owner’s financial interest to truthfully declare his value to the government. This result holds provided that the likelihood that a developer will wish to purchase one property is not affected by the declared prices of adjacent properties. Otherwise the owners would be able to lower their tax burdens if they were to collude and declare prices that overstate their valuations.

Design of the Experiments

We used laboratory experiments with human subjects as a policy test bed for the proposed tax mechanisms. This setup allowed us to observe different tax policies under identical conditions and measure their performance. Our experiments were organized into negotiations. In each negotiation one buyer tried to purchase properties from four sellers. The participants earned cash payments based on the outcome of the negotiation. We gave each seller a value for his property, known only to himself. If the seller sold his property during the negotiation, he earned an amount equal to the price the buyer paid him. If the seller did not sell, we paid him an amount equal to his value. The value of every seller’s property was drawn at random between $100,000 and $150,000. When paying the sellers after the experiment, we gave them $1 in US currency for every $15,500 they had earned in the experiment.

We gave the buyer a value—known only to herself—for the combination of the four properties. If the buyer purchased all four properties she earned the value minus the prices she had paid. If the buyer failed to buy one or more of the properties, then she did not earn her value. The buyer’s value was drawn at random between $300,000 and $1,250,000. We paid the buyer $1 US for every $60,000 she had earned in the experiment.

We conducted the negotiations in three tax policy treatments. The control treatment—or “baseline”—mimicked current tax law. The sellers started the negotiation owing $10,000 in tax on their properties. If they sold their property, then no tax was owed; if they did not sell, then the $10,000 was deducted from their payment after the experiment. The buyer had five rounds to negotiate with the sellers. In each round, she sent offers to the sellers, which they could accept or reject. We made delay costly to the buyer by imposing a 5 percent penalty on her post-experiment earnings for every round in which at least one seller refused to sell. The buyer was free to abandon negotiations in any negotiating round.

In addition to the baseline, we conducted two experimental treatments: “revealed” and “declared.” The revealed treatment was identical to the baseline except for one change: if a seller rejected all of the buyer’s offers, then we used the highest of those offers to reassess his property tax, charging him 10 percent of the highest offer rather than $10,000 as in the baseline. The highest offer was typically more than $100,000, so this reassessment was costly to sellers who kept their properties. In the declared treatment, there was no negotiation between buyer and sellers. The sellers simply declared a price for their properties and we used a tax formula to assess a tax for each seller. If the sum of the declared prices was less than or equal to the buyer’s value, then she purchased all four properties, otherwise she did not.

Results of the Experiments

Both of the experimental tax policies were very successful in facilitating land assembly. Buyers in the baseline were successful in assembling all four properties only 50 percent of the time. In the revealed treatment, the buyers succeeded in 79 percent of their negotiations. This higher assembly rate was driven by a reduction in the amount of money sellers held out for in the revealed treatment. In the baseline, the average holdout was for $54,000 more than the value, while in the revealed treatment it was for $26,000. Thus, it was easier to get sellers to agree to a price in the revealed treatment.

In the declared treatment, buyers were even more successful, assembling the properties in 83 percent of the negotiations. Sellers in this treatment did hold out by declaring prices higher than their values. However, the amounts for which they held out—typically $42,000—were usually not enough to exceed the buyer’s value. Also, buyers in the baseline often became discouraged after repeated rejections from one or more sellers and ended negotiations early. This never happened in the declared treatment, which contained only one round of negotiation for each buyer.

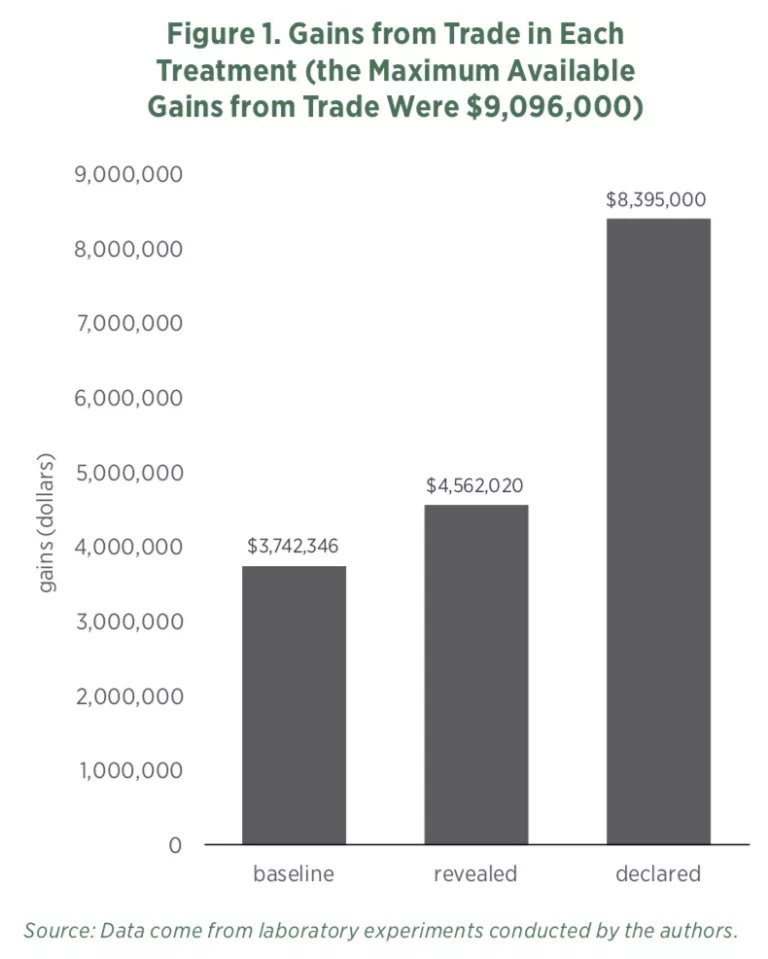

We also measured the gains from trade between the buyer and seller. In each treatment, a total of about $9.1 million in experimental currency could have been earned.

In contrast, participants captured almost all of the gains from trade in the declared treatment. They earned a total of $8.4 million, or 92 percent of what was available. This superior performance is a result of two factors: First, the only negotiations that failed in the declared treatment were those with small gains from trade available. Second, delay was impossible in the declared treatment, so successful negotiations never lost value as in the baseline and revealed treatments.

Conclusion

Our laboratory experiments offer compelling evidence that eminent domain is not necessary to facilitate land assembly. At least two tax policies could drastically increase the success rate of assembly relative to the status quo. One of these policies—declared assessment—could also eliminate delay and increase gains from trade by a substantial margin.

Some landowners may be uncomfortable with revealed assessment or declared assessment because those methods could empower private parties to increase a seller’s tax assessment or force a sale of the seller’s property. However, both policies could be tweaked so that they vary in who is certified to make an offer that triggers reassessment or executes a sale at the declared price. In the strictest case, the government would be the only certified body and these tax policies would simply be a substitute for eminent domain. In a less strict scenario, one or more private developers could be certified to invoke the tax policy (perhaps only in a limited number of cases). In the most liberal scenario—which is unlikely to be adopted—any individual or organization could make an offer that affects the owner’s property tax liability or forces him to sell.

In any event, our experiments can be considered proof of concept of alternatives to eminent domain that are more respectful of private property rights. Other researchers may propose still other alternatives that are more effective or politically popular or easier to implement than the ones presented here. We welcome such proposals. In our view, the hunt is on for new solutions to the holdout problem, and it should continue until eminent domain is a thing of the past.