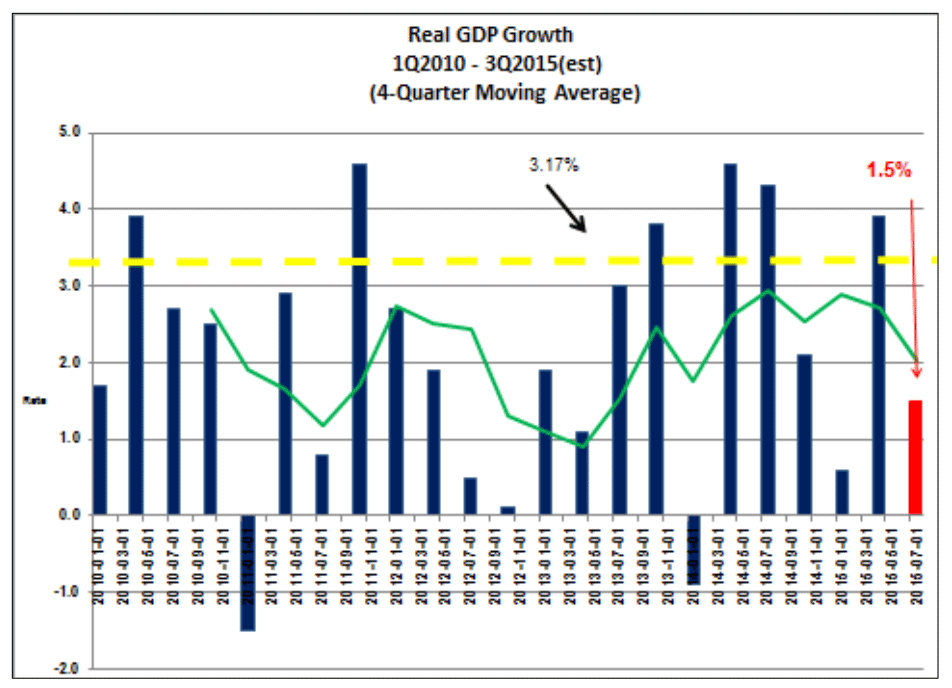

Fed uncertainty, the levitated dollar, China’s continuing weak economy, Europe’s mixed bag, and US political crazy season combine to yield a slow but somehow sound winter economy. Let’s take it from the top. The most recent third quarter 2015 GDP growth estimate arrived to the tune of 1.5 percent.

The Winter Economy

Fed uncertainty, the levitated dollar, China’s continuing weak economy, Europe’s mixed bag, and US political crazy season combine to yield a slow but somehow sound winter economy. Let’s take it from the top. The most recent third quarter 2015 GDP growth estimate arrived to the tune of 1.5 percent. When considered in terms of a four-quarter moving average, the more inclusive trend yields a rather cool 2.0 percent, well below the yellow dashed line in the accompanying chart that reminds us of the gap between current performance and the longer-run average.

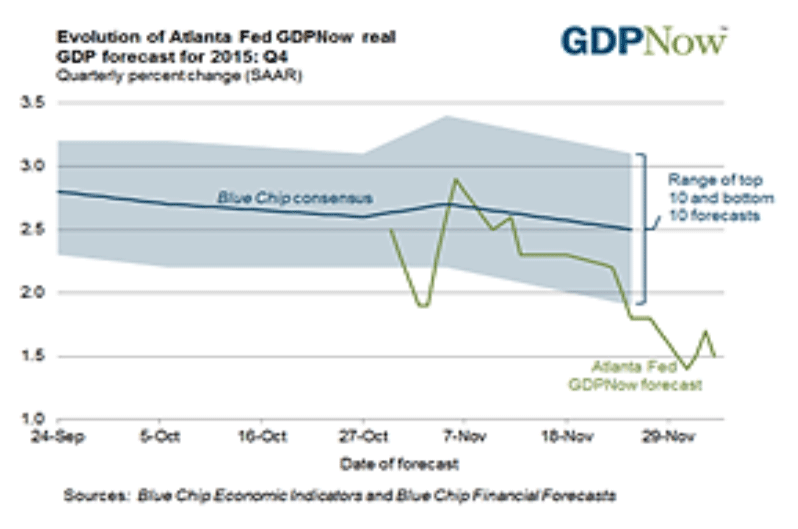

What about the prospects for closing the GDP gap in the months ahead? Don’t bet on it. According to most soothsayers and forecasters, the chances are slim to none. The Atlanta Fed’s GDPNow analysts’ December indicator showed GDP growth falling to 1.5 percent, which, as indicated in the accompanying chart, is well below the Blue Chip consensus. Construction, while recovering, is still weak, as is investment in new plants and equipment. Dramatically lower energy prices are stimulating some sectors but newly imposed energy regulations are weakening others. The economy is operating like a strange washing machine that is taking in fresh water while also caught in a spin cycle.

Growth Components

The effects of this are seen when we examine recent components of GDP growth. As indicated here, consumption—consumer spending—is the big driver. Growing expenditures on services, with healthcare being a major item, account for the strongest part of this. Net trade, driven down by the strong dollar and weaker trading partner growth, is either adding little to the mix or subtracting from it. As indicated in the chart, the advance estimate for the third quarter of 2015 shows inventory reductions as a large negative component of GDP growth. We have no way of knowing if decision makers overreacted to the economy when managing their supply chains or whether sudden increases in consumer spending caught them off guard. But based on recent retail sales data and weaker consumer balance sheets, those inventory cuts may be well-justified.