- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

Comment on Proposed Rulemaking for Regulatory Capital Rules

The Supplementary Leverage Ratio Means Supplementary Complexity

I appreciate the opportunity to comment on the notice of proposed rulemaking for “Regulatory Capital Rules: Regulatory Capital, Enhanced Supplementary Leverage Ratio Standards for U.S. Global Systemically Important Bank Holding Companies and Certain of Their Subsidiary Insured Depository Institutions; Total Loss-Absorbing Capacity Requirements for U.S. Global Systemically Important Bank Holding Companies.” I am an economist at the Mercatus Center, a university-based research center at George Mason University. My comments do not reflect the views of any affected party but do reflect my general concerns about the effectiveness of regulation and the associated burden and unintended consequences of regulation.

I will briefly summarize the points I will make that concern some of the questions posed in the notice of proposed rulemaking and then provide more detail supporting my responses.

- Question 1 concerns whether the enhanced supplementary leverage ratio proposal balances stability against growth. While higher capital for banks does help foster stability, the complexity of the proposal and existing guidelines make capital adequacy standards more costly for firms adhering to those standards. Larger firms may be able to manage the costs better than smaller firms would, but customers ultimately bear at least some of the added costs. A simple, higher leverage ratio is less costly to implement and fosters stability.

- Question 5 concerns the benefits and drawbacks of excluding central bank reserves from the denominator of the supplementary leverage ratio. The short answer to this question is that doing so turns the leverage ratio into a risk-based capital ratio, albeit a very simple one. Risk-based capital standards can create unintended consequences that undermine the effectiveness of higher capital requirements.

- Question 8 asks about any concerns arising from adopting the proposed modification and whether alternatives might be considered instead. I discuss some simpler alternatives.

- Question 9 concerns whether a dynamic risk-based capital surcharge should be implemented. Such proposals may not add much value but do add complexity.

Concerning Question 1: The Simple Leverage Ratio Works

In a keynote speech on March 28, 2018, former Federal Deposit Insurance Corporation (FDIC) Vice Chairman Thomas Hoenig asked, “Why shouldn’t a capital ratio of 10 percent equity to total assets be the minimum standard for every bank wishing to operate in the United States?” One-size-fits-all regulations in general may not be justified, but capital concerns solvency rather than size, so the suggestion has merit. The 10 percent minimum may even be too low, as James Barth and I found in a recent working paper: under relatively conservative assumptions, the benefits of increasing the leverage ratio to 15 percent tend to outweigh the costs. Our baseline results suggested that 19 percent might be optimal, or the level at which the marginal benefits would equal the marginal costs.

Concerning Question 5: Complexity Does Not Mean Efficacy

Page 17,319 of the Federal Register notice of proposed rulemaking cites a Federal Reserve Bank of New York study in footnote 12 as a justification for having both the leverage ratio and the risk-based capital requirements. Yet numerous academic studies have found that risk-based capital requirements have a weaker empirical relationship with stock returns and measures of bank risk than simpler, non-risk-based measures of capital. Other studies have observed that risk-based capital requirements create regulatory arbitrage opportunities, even leading up to the last crisis.

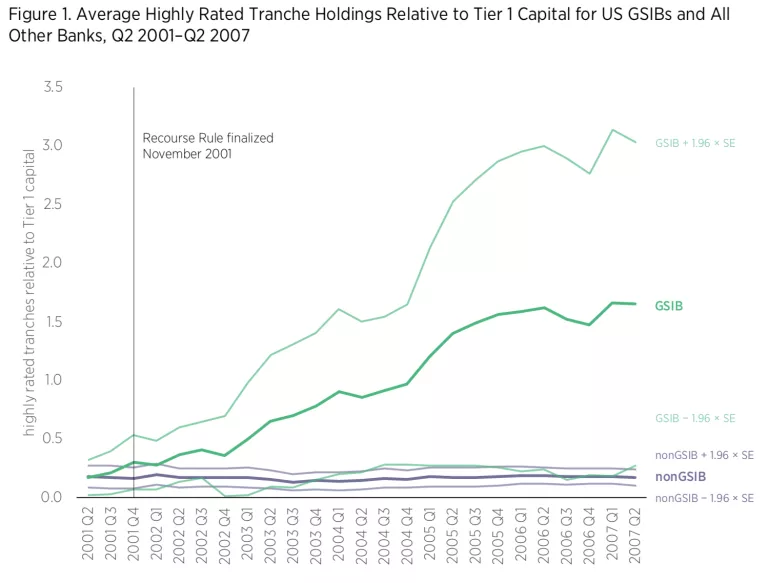

One example in the lead-up to the last crisis is the changes to risk-based capital requirements following the Recourse Rule, finalized on November 29, 2001, by the Federal Reserve System (FRS), Federal Deposit Insurance Corporation (FDIC), and Office of the Comptroller of the Currency (OCC). A key aspect of the rule was that it lowered the risk weights for bank holdings of highly rated, private-label asset-backed and mortgage-backed security tranches and collateralized debt obligation tranches. For tranches with AAA or AA ratings, risk weights were lowered from at least 0.5 to 0.2, which meant that capital requirements for these assets fell from at least 4 percent to 1.6 percent, while for A-rated tranches the risk weights were set at 0.5, which meant that the capital requirement equaled 4 percent.

Figure 1 shows the average holdings of highly rated, private-label securitization tranches relative to Tier 1 capital for US global systemically important banks (GSIBs) listed in the FDIC’s Global Capital Index that were bank holding companies (BHCs) in the period from Q1 2001 to Q2 2007—and also Wachovia—as well as the 95 percent confidence interval. While not shown, BHCs with greater holdings of the highly rated tranches also experienced increases in insolvency risk. Figure 1 also depicts the quarterly average holdings for all other BHCs with at least $1 billion in total assets, as well as the 95 percent confidence interval. The figure shows that on average, the largest BHCs that securitized assets held the most highly rated securitization tranches, measured here relative to Tier 1 capital; and highly rated tranche holdings rose after the Recourse Rule was finalized and until mid-2007.

Note: To estimate these holdings for all reporting bank holding company corporations with total assets (bhck2170) greater than $1 billion, Erel et al. suggest adding held-to-maturity securities in the 20-percent and 50-percent risk buckets (bhc21754 and bhc51754), available-for-sale securities in the 20-percent and 50-percent risk buckets (bhc21773 and bhc51773), and all other mortgage backed securities in trading accounts (bhck3536). From this total, they subtract the amortized cost of held-to-maturity US government agency and corporation obligations issued by US government–sponsored agencies (bhck1294); amortized cost of available-for-sale US government agency and corporation obligations issued by US government–sponsored agencies (bhck1297); amortized cost of held-to-maturity mortgage pass-through securities issued by Fannie Mae and Freddie Mac (bhck1703); amortized cost of available-for-sale mortgage pass-through securities issued by Fannie Mae and Freddie Mac (bhck1706); amortized cost of held-to-maturity mortgage-backed securities issued or guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae (bhck1714); amortized cost of available-for-sale mortgage-backed securities issued or guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae (bhck1716); amortized cost of other held-to-maturity mortgage-backed securities collateralized by mortgage-backed securities issued or guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae (bhck1718); amortized cost of other available-for-sale mortgage-backed securities collateralized by mortgage-backed securities issued or guaranteed by Fannie Mae, Freddie Mac, or Ginnie Mae (bhck1731); amortized cost of held-to-maturity securities issued by states and political subdivisions in the United States (bhck8496); and amortized cost of available-for-sale securities issued by states and political subdivisions in the United States (bhck8498). These estimated holdings are then divided by Tier 1 capital (bhck8274).

Source: Chicago Fed Call Report Y-9C forms, available from The Wharton School, University of Pennsylvania, “Wharton Research Data Services,” accessed August 18, 2015, https://wrds-web.wharton.upenn.edu/wrds/.

A general implication of the graph is that in spite of the often-repeated claim that the leverage ratio contributes to bank risk-taking, the same might be said about risk weights, especially since BHCs with greater holdings of the highly rated tranches also experienced increases in insolvency risk.

Recent studies have found that while banks satisfied regulatory capital requirements, which rely on book values, market valuations of capital plunged well below book values during the crisis. As banks are able to use the more complex risk-based capital requirements to lower the required regulatory capital, the efficacy of these standards becomes suspect and complexity grows.

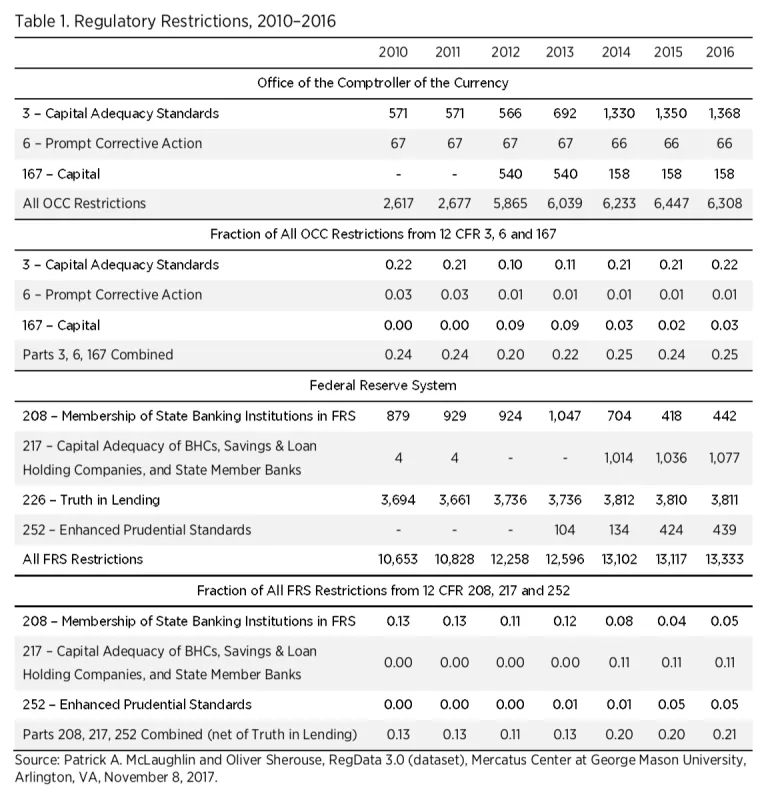

Table 1 reports data available from the QuantGov open-source platform to quantify the growing complexity of regulations associated with this particular proposed rule and other closely related parts, based on counts of regulatory restrictions that appear in the US Code of Federal Regulations (CFR). In the QuantGov platform, regulatory restrictions are instances of the terms shall, must, may not, required, and prohibited, which signify legal constraints or obligations. For the OCC, parts 3 and 167 of the CFR already make up nearly 25 percent of regulatory restrictions. For the FRS, the largest fraction of its regulatory restrictions are associated with “Truth in Lending,” so after netting out those restrictions, parts 208, 217, and 252, which concern this notice of proposed rulemaking, make up about 20 percent of all regulatory restrictions.

Overall, the results show that the complexity (defined in terms of regulatory restrictions) has been growing since 2010. Some of that rise may come from Dodd-Frank, but some of it comes from the rulemaking associated with establishing capital adequacy standards consistent with Basel Committee on Banking Supervision guidelines. The Economic Growth, Regulatory Relief, and Consumer Protection Act (Pub. L. No. 115-174, 132 Stat. 1296 (2018)) does have provisions that will address this for smaller banking organizations. Still, the complexity does not serve consumers well, as it tends to raise the cost of compliance for the regulated entities, which makes financial services more costly, less accessible to consumers, or both. In the face of this growing problem, the question is whether viable alternatives exist.

Concerning Question 8: Alternatives

If size-based capital adequacy standards are to remain in place, then the Federal Reserve Bank of Minneapolis’s “plan to end too big to fail” offers a simpler option. In particular, steps 1 and 2 of the plan concern financial institutions with at least $250 billion in total assets. For those deemed not systemically important, step 1 calls for them to meet a 23.5 percent equity-to-risk-weighted-assets ratio and a simpler 15 percent equity-to-total-assets leverage ratio. For those deemed systemically important, step 2 of the plan calls for financial institutions with at least $250 billion to have their equity-to-risk-weighted-asset ratios increased further from 23.5 percent (which translates to a 15 percent leverage ratio) to 38 percent (which translates to a 23.75 percent leverage ratio). The combination of risk-based capital and the supplementary leverage ratio does not signal capital adequacy the way the market would. In the end, investors will look at equity values.

I have discussed another option in a recent public interest comment that calls for using a ratio of some measure of the market value of equity relative to short-term liabilities rather than assets. That could also address the challenge of marking assets to market, which arises because many bank assets trade infrequently. Tracking the face value of short-term liabilities could simplify the process too.

The idea draws from the US model for calculating required reserves for banks. To satisfy reserve requirements, banks in the United States currently measure reserves relative to the average amount of net transaction accounts. To accomplish that, reserve managers determine required reserves during the reserve computation period, and then must ensure that required reserves are met during the reserve maintenance period.

Currently, reserve managers calculate the daily average during the previous 14 days of net transaction accounts during the reserve computation period, which begins on Thursdays and ends two Wednesdays later. Net transaction accounts equal total transaction accounts, which include those for which account holders can make withdrawals (e.g., demand deposits and negotiable orders of withdrawal), minus demand balances due from other banks and items in process of collection. Once determined, reserves must cover the target during the reserve maintenance period, which begins 17 days after the reserve computation period ends.

A capital adequacy standard might be developed in line with this reserves management model. Here, bank treasury staff could be made to ensure that the market value of the bank’s equity (market price of shares times the total number of shares of common stock outstanding) equals a fixed fraction of current short-term liabilities during some short-term period, such as one quarter.

As an example, if a bank has a median value of $100 billion in various forms of short-term debt during a particular period, and if the capital requirement is 15 percent, then staff must ensure that the average or median market value of the bank’s shares during that period equals $15 billion. The use of the median could be robust to large fluctuations in stock prices, while the use of market prices would foster market discipline.

Concerning Question 9: Dynamic Capital Requirements Add to Complexity, But Probably Not Efficacy

While some studies have tried to establish the merits of dynamic capital requirements, here I would like to point to the study by Juliane Begenau and Timothy Landvoigt. They show that a simple leverage ratio of 15 percent is optimal, that such a leverage ratio does not increase risk-taking by banks, and that a counter-cyclical measure has little merit.

Conclusion

Overall, the general direction of regulatory capital requirements, including the proposal here, works against the competitiveness and effectiveness of the banking system without contributing to stability. Simpler, higher capital requirements foster stability.

rule and agency details

Agency: US Department of the Treasury, Office of the Comptroller of the Currency

Proposed: April 19, 2018

Extended: May 25, 2018

Comment Period Closes: June 19, 2018

Submitted: June 19, 2018

Docket ID: OCC-2018-0002

RIN: 1557-AE35

Agency: Federal Reserve System

Proposed: April 19, 2018

Extended: May 25, 2018

Comment Period Closes: June 19, 2018

Submitted: June 19, 2018

Docket No. R-1604

RIN: 7100-AF03