- | Financial Markets Financial Markets

- | Data Visualizations Data Visualizations

- |

The Decline of US Small Banks (2000–2013)

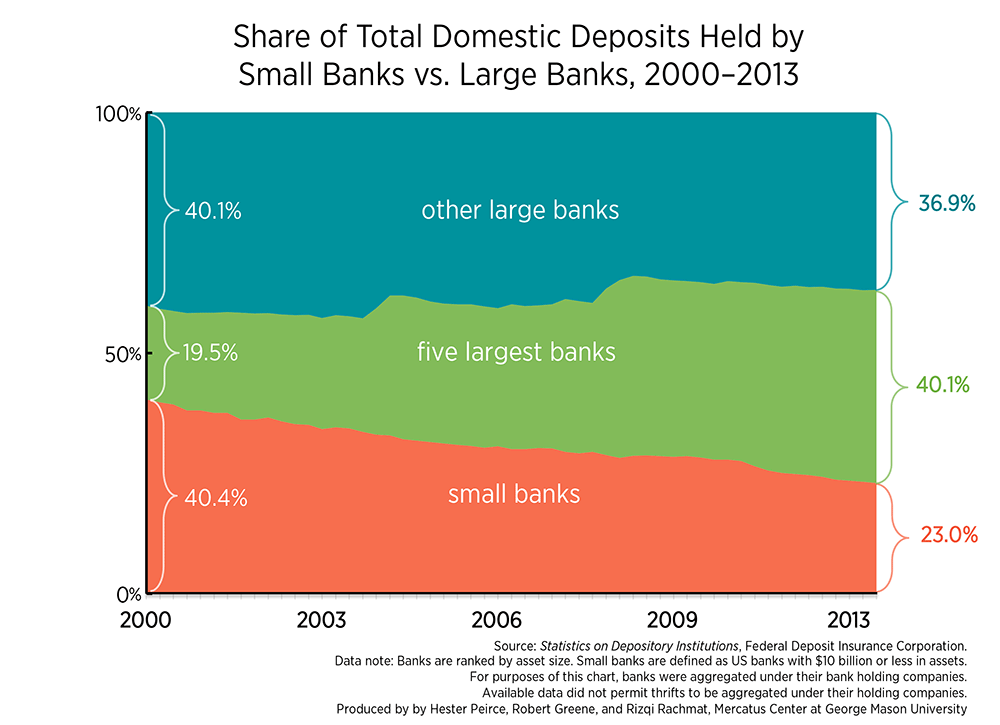

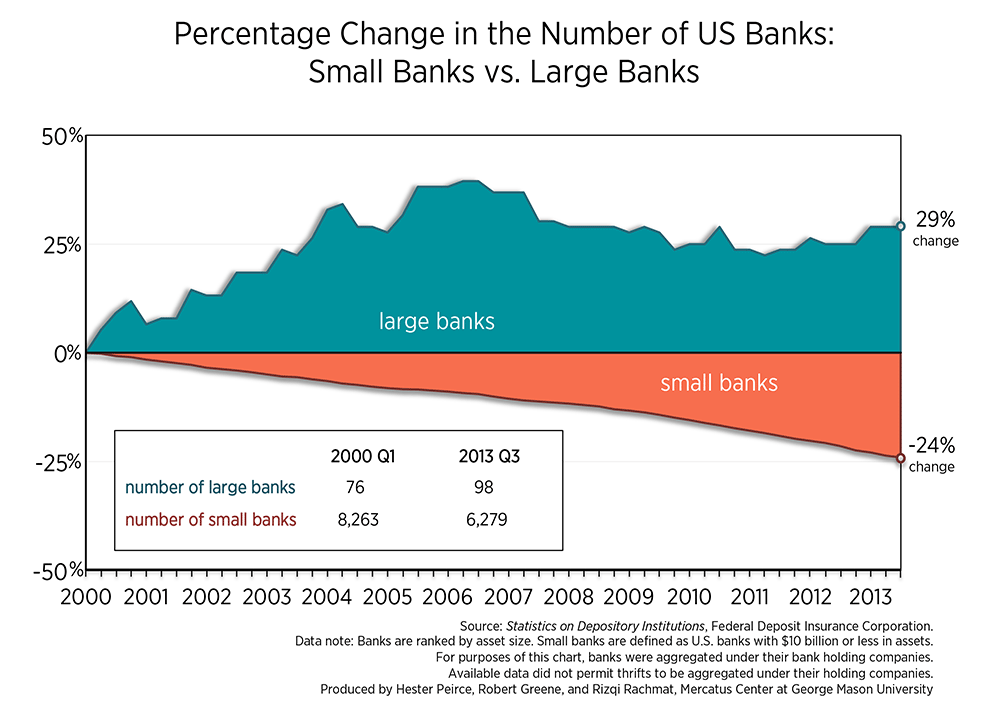

The charts below show that both the number of US small banks (which we define as banks with $10 billion or less in assets) and their share of US banking assets and domestic deposits declined substantially between 2000 and 2008. Simultaneously, the five largest US banks’ share of US banking assets and domestic deposits increased markedly.

The charts below show that both the number of US small banks (which we define as banks with $10 billion or less in assets) and their share of US banking assets and domestic deposits declined substantially between 2000 and 2008. Simultaneously, the five largest US banks’ share of US banking assets and domestic deposits increased markedly. Since the financial crisis, US banking assets and deposits have continued to consolidate in a handful of large banks. As the charts show, the five largest banks by assets now hold 44.0 percent of US banking assets and 40.1 percent of domestic deposits—up from 23.5 percent and 19.5 percent, respectively, in early 2000. Correspondingly, small banks’ share of domestic deposits has fallen from 40.4 percent to 23.0 percent since early 2000, and their share of US banking assets has declined from 35.8 to 19.5 percent.

Small banks play a critical role in the US banking system and are particularly important in rural and small metropolitan areas. As an AEI report details, small banks play a particularly important role in providing certain products, such as small-business loans, mortgages, and farm loans. They typically fund themselves with customer deposits. Small banks’ community focus enables them to develop and maintain relationships with customers. Through these interactions, they obtain information about borrowers that larger banks generally do not have. As a result, small banks are able to make loans to borrowers who might not qualify under larger institutions’ standardized lending criteria.

There are many factors at work contributing to the huge decline in small banks’ market share. Some of the decline is organic, in that market forces encourage combinations of small banks as a way of spreading operational costs over a larger customer base. The FDIC finds that an average of 182 mergers and 107 consolidations occurred per year from 2001 to 2011. The FDIC also shows that some small banks simply outgrew their small bank status.

Another factor, the financial crisis, is less benign. One study finds that more than five percent of small banks failed in the wake of the crisis.

Bank concentration itself is not bad. But increasing regulatory burdens force consolidation in the US banking industry for the wrong reasons. Regulatory compliance can be a particular challenge for small banks with limited compliance expertise. Regulatory expenses absorb a larger percentage of small banks’ budgets than of their larger counterparts’ budgets. Although correlation is not evidence of causation, as financial regulation has increased since 2000, so has banking concentration. The Dodd-Frank Act, passed in 2010, imposes a new set of regulations that are disproportionately burdensome to small banks. Moreover, by designating the largest financial institutions as “systemically important,” Dodd-Frank creates a market expectation that designated firms are too big to fail and generates funding and other competitive advantages for the largest US banks.

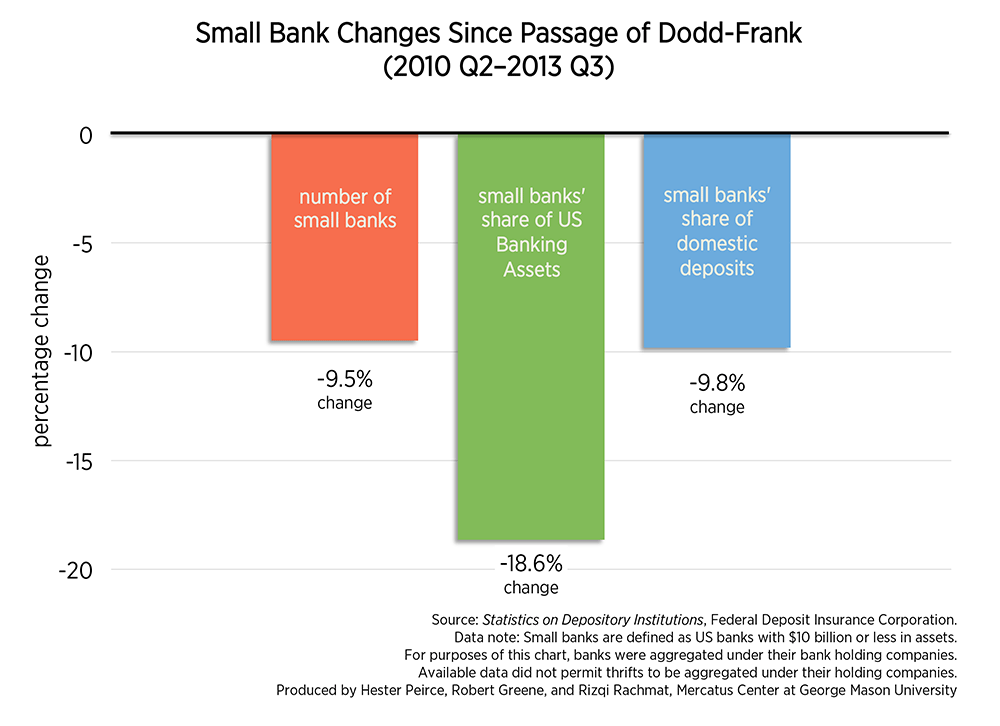

Since the second quarter of 2010—immediately before the July passage of Dodd-Frank—to the third quarter of 2013, the United States lost 650, or 9.5 percent, of its small banks. Small banks’ share of US banking assets and domestic deposits has decreased 18.6 percent and 9.8 percent, respectively, and the five largest US banks appear to have absorbed much of this market share. Mounting regulatory costs threaten to accelerate the shift towards big banks and away from small banks that have long been important members of the financial industry and the local communities they serve.