- | Financial Markets Financial Markets

- | Policy Briefs Policy Briefs

- |

Large Bank Holding Company Capital Ratios before and after Basel III

After the 2007–2009 financial crisis, the Basel Committee on Banking Supervision (BCBS) at the Bank of International Settlements unveiled Basel III to address perceived shortcomings in the original Basel I capital adequacy standard guidelines. The new guidelines added more measures to establish minimum capital adequacy in a way that made existing bank capital guidelines more complex while increasing the minimum required amount of funding from capital. The US implementation of the Basel III guidelines applies to most bank holding companies (BHCs) and bank subsidiaries, with even higher standards applying to the largest holding companies. In this policy brief, I show that the number of capital ratios for US BHCs has proliferated, but the fundamental measure of the ratio of Tier 1 to risk-weighted assets on average changed little after the US implementation of the Basel III capital final rulemaking. This circumstance suggests that not much has changed aside from the added complexity.

How Basel III Changed Bank Capital Requirements

In the aftermath of the financial crisis, the BCBS unveiled the so-called Basel III capital guidelines in December 2010 and then a revised version in June 2011. US regulators subsequently implemented a variant of those guidelines after issuing three notices of proposed rulemaking in June 2012, and after the notice and comment period, they issued a final rulemaking in July 2013. The most complex versions of those standards focus on so-called advanced approaches BHCs, which tend to have at least $250 billion in total assets or considerable foreign exposures or have elected to be classified that way. The list includes Bank of America, Bank of New York Mellon, Citigroup, Goldman Sachs, JPMorgan Chase, Morgan Stanley, Northern Trust, State Street, U.S. Bancorp, and Wells Fargo.

The capital adequacy standards under the original US Basel I rulemaking were complex. For instance, banks had to adjust the measure of assets in the denominator of the capital ratios by weighting assets according to officially determined values intended to reflect the underlying risks. Under Basel I, Basel II, and Basel III, assets deemed riskier are assigned higher risk weights, which would tend to increase the asset measure and lower the capital ratio, while assets deemed safer have lower or even no risk weights, which would tend to decrease the asset measure and increase the capital ratio. For example, under the simpler standardized approach that most BHCs tend to use, US Treasuries and balances held at regional Federal Reserve banks, or reserves, have no risk weights, agency mortgage-backed securities might be assigned 20 percent risk weights, mortgages are assigned 50 percent risk weights, and loans might be assigned 100 percent risk weights. That approach implies that if a bank has $100 million allocated to each category, total assets equal $500 million, but risk-weighted assets calculated under the standardized approach equal only $170 million. Advanced approaches BHCs have to apply complex formulae to measure risk-weighted assets.

The accounting measures of regulatory capital used in the numerators of the minimum regulatory capital ratios are also complex. The primary sources of capital under the original US Basel I rulemaking included Tier 1 capital, comprising common equity capital, noncumulative perpetual preferred stock, and minority interests in equity capital accounts of consolidated subsidiaries. Banks also had to subtract goodwill, other intangible and deferred tax assets disallowed, and other amounts determined by the federal supervisor. Tier 2 capital included cumulative perpetual preferred stock, intermediate-term preferred stock, convertible and subordinated debt and allowances for credit losses (for example, loan and lease losses), and pretax net unrealized holding gains on available-for-sale equity securities that have determinable fair values.

US Basel III defines Tier 1 capital as the sum of common stock and retained earnings, accumulated other comprehensive income for non-opt-out and advanced approaches BHCs, deductions and adjustments, qualifying Common Equity Tier 1 (CET1) minority interest minus the sum of goodwill, other intangibles, and deferred tax assets. US Basel III defines Tier 2 capital as allowances for loan and lease losses to a limited extent, qualifying preferred stock, subordinated debt, and minority interests. Although US Basel III maintains the ratio of minimum total capital to risk-weighted assets (total capital ratio) at 8 percent, the rulemaking adds much more complexity for regulatory compliance by changing or adding new minimum risk-based capital ratios, including

- increasing the ratio of Tier 1 capital to risk-weighted assets (Tier 1 capital ratio) from 4.0 percent to 6.0 percent;

- introducing a new ratio of CET1 capital to risk-weighted assets (CET1 capital ratio) equal to 4.5 percent;

- introducing a new capital conservation buffer that adds 2.5 percent to the CET1, Tier 1, and total capital ratios, with the aim of limiting distributions to investors or bonuses to executives if the buffer falls below 2.5 percent; and

- introducing a new global systemically important bank (GSIB) surcharge that adds between 1.0 and 4.5 percent to the capital conservation buffer and, in turn, the CET1, Tier 1, and Total capital ratios, which applies to advanced approaches BHCs rather than GSIBs with at least $50 billion in total assets, as originally planned.

US Basel III also introduced a countercyclical capital buffer that would add between 0 and 2.5 percent additional capital for advanced approaches BHCs, depending on whether officials deem credit growth excessive. However, to date, regulators have yet to implement the measure.

Table 1 summarizes how the minimum risk-based capital requirements changed between Basel I and Basel III. The upper panel of rows show the change in the individual ratios, whereas the lower panel of rows show the change in the combined minimum ratios. Although Basel III pushed to make equity a greater component of Tier 1 capital through the introduction of the CET1 ratio, the Tier 1 capital ratio still receives the most attention in policy and research debates, because it comprises the bulk of the total capital ratio. Table 1 shows that by the end of the transition period, the minimum Tier 1 capital ratio equaled between 9.5 and 13 percent, when including the buffers for advanced approaches BHCs, and after subtracting the GSIB surcharge the minimum Tier 1 capital ratio equaled 8.5 percent for smaller BHCs.

Table 1. Changes in US Basel Minimum Risk-Based Capital Requirements

Ratio | Basel I | Basel II | Basel II.5 | Basel III | |||||||

1991–1992 | 1993–2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | |

Individual Ratios | |||||||||||

Minimum CET1 ratio |

|

|

|

| 3.500 | 4.000 | 4.500 | 4.500 | 4.500 | 4.500 | 4.500 |

Minimum Tier 1 ratio | 3.625 | 4.000 | 4.000 | 4.000 | 4.500 | 5.500 | 6.000 | 6.000 | 6.000 | 6.000 | 6.000 |

Minimum total ratio | 7.250 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 |

Capital conservation buffer |

|

|

|

|

|

|

| 0.625 | 1.250 | 1.875 | 2.500 |

GSIB surcharge (range) |

|

|

|

|

|

|

| 0.250–1.125 | 0.500–2.250 | 0.750–3.375 | 1.000–4.500 |

Total Ratios | |||||||||||

Minimum CET1 ratio + capital conservation buffer + GSIB surcharge (range) |

|

|

|

| 3.500 | 4.000 | 4.500 | 5.375–6.250 | 6.250–8.000 | 7.125–9.750 | 8.000–11.500 |

Minimum Tier 1 ratio + capital conservation buffer + GSIB surcharge (range) | 3.625 | 4.000 | 4.000 | 4.000 | 4.500 | 5.500 | 6.000 | 6.875–7.750 | 7.750–9.500 | 8.625–11.250 | 9.500–13.000 |

Minimum total ratio + capital conservation buffer + GSIB surcharge (range) | 7.250 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.000 | 8.875–9.750 | 9.750–11.500 | 10.625–13.250 | 11.500–15.000 |

Note: Table adapted from table 2 in Stephen Matteo Miller and Blake Hoarty, “On Regulation and Excess Reserves: The Case of Basel III” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, July 2020).

Table 1 summarizes only changes to risk-based capital ratios. Although Basel III guidelines included a non-risk-based leverage ratio for the first time, US regulators have always used a variant of a simpler non-risk-weighted capital ratio, known as the leverage ratio. The leverage ratio includes Tier 1 capital in the numerator and total assets, rather than risk-weighted assets, in the denominator. The US Basel III rulemaking introduced the following changes:

- Replacement of the old ratio of Tier 1 capital to asset leverage with a new ratio of Tier 1 capital to on-balance-sheet exposures of at least 4 percent—the leverage ratio—for all BHCs.

- Introduction of a new additional ratio of Tier 1 capital to total leverage exposure of at least 3 percent of total on- and off-balance-sheet exposures—the supplementary leverage ratio (SLR)—for advanced approaches BHCs

- Introduction of a new enhanced supplementary leverage ratio (eSLR) that adds a buffer of 2 percent to the 3 percent SLR (for a total of 5 percent) for BHCs with at least $700 billion in total assets or $10 trillion in assets under custody, with the aim of limiting distributions to investors or bonuses to executives if the buffer falls below 2 percent

Given the additional capital requirements and increased regulatory minima, one might expect to see an increase in the overall Tier 1 capital ratio. However, I will show that little has changed.

Tier 1 Capital Ratios before and after Basel III

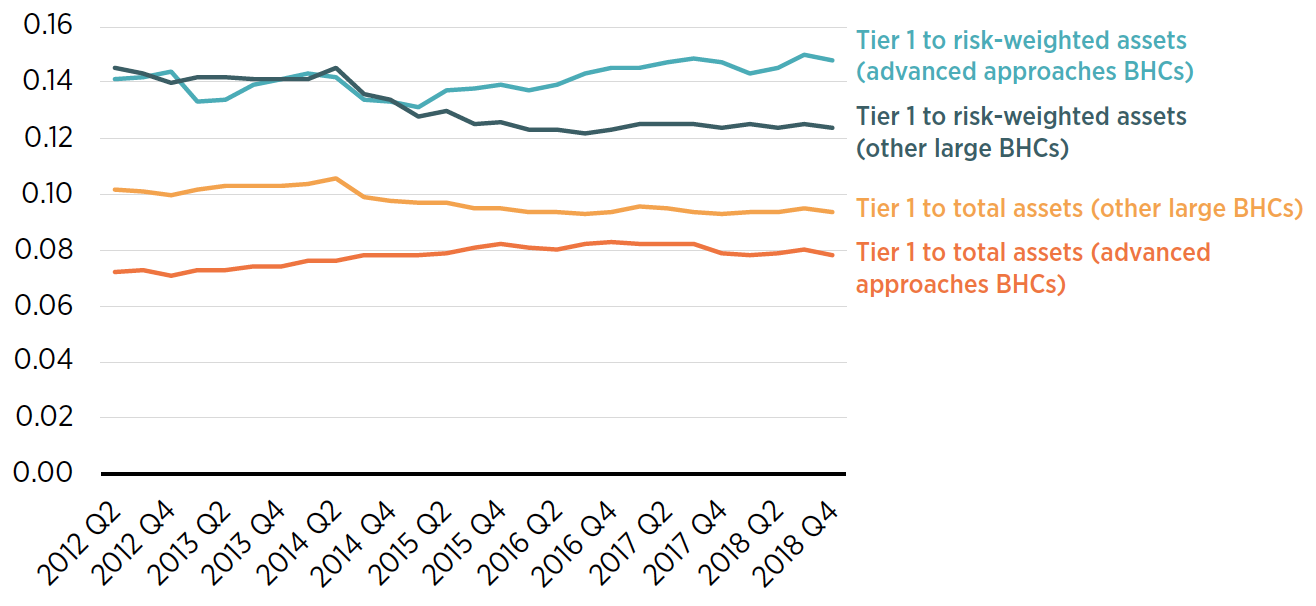

Figure 1 depicts the average Tier 1 capital ratio, and the leverage ratio of Tier 1 capital to total (on-balance sheet) assets, for advanced approaches BHCs and for non-advanced approaches BHCs that had at least $10 billion in total assets. The figure shows that before the implementation of the US Basel III final rulemaking, the average Tier 1 capital ratio for advanced approaches and non-advanced approaches BHCs was similar. However, with the implementation of US Basel III, on average, non-advanced approaches BHCs had slightly lower Tier 1 regulatory capital ratios, whether measured relative to risk-weighted assets or total assets. For advanced approaches BHCs, the ratio of Tier 1 capital to total assets increased after the implementation of Basel III, while the ratio of Tier 1 capital to risk-weighted assets exhibits little difference from that observed before the implementation of Basel III.

Figure 1. Average Risk-Based Capital Ratios and Leverage Ratios for Advanced Approaches and Non-Advanced Approaches BHCs with at Least $10 Billion in Total Assets, Q2 2012–Q4 2018

Note: To measure the ratio of Tier 1 to risk-weighted assets before Q1 2015, divide “Tier 1 capital,” bhck8274, by “Risk-weighted assets,” bhcka223. For non-advanced approaches BHCs, starting in Q1 2015, divide “Tier 1 capital,” bhca8274, by “Risk-weighted assets,” bhcaa223. For advanced approaches BHCs, starting in Q1 2014, divide “Tier 1 capital,” bhca8274, by “Risk-weighted assets,” bhcaa223. Then, starting in Q3 2014, divide “Tier 1 capital,” bhca8274, by “Risk-weighted assets,” bhcwa223. Divide “Tier 1 capital,” bhca8274, by “Risk-weighted assets,” bhcwa223, for Wells Fargo starting in Q2 2015 and for Bank of America starting in Q4 2015.

Source: The data for all reporting BHCs with greater than $10 billion are recorded in the Chicago Fed Call Report Y-9C forms, available from “Wharton Research Data Services,” Wharton School, University of Pennsylvania, accessed April 21, 2020, https://wrds-web.wharton.upenn.edu/wrds/.

In spite of much praise for the US Basel III framework, lobbyists often complain about the onerous nature of bank capital but focus on capital ratios being too high. Yet, the Tier 1 leverage ratio shows that capital ratios have changed little in the years since the crisis. This lack of change matters because a number of studies have found that the optimal leverage ratio could be as high as 15 percent or more, well above the average values depicted in figure 1.

Conclusion

The results here show that capital regulation for large BHCs has become increasingly complex since the implementation of Basel III. At the same time, in spite of efforts to have BHCs operate with more capital, the results for the largest BHCs do not differ much from what one observed before the implementation of Basel III.