- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

Proposed Leverage Buffer and Credit Risk Transfer Rules Contradict the FHFA's Goals

Enterprise Regulatory Capital Framework Rule-Prescribed Leverage Buffer Amount and Credit Risk Transfer

Agency: Federal Housing Finance Agency

Comment Period Opens: September 27, 2021

Comment Period Closes: November 26, 2021

Comment Submitted: November 23, 2021

Document No. 2021-20297

RIN: 2590-AB17

We appreciate the opportunity to submit a comment to the Federal Housing Finance Agency (FHFA) in response to its 2021 proposed changes to its rules defining the capital adequacy of Fannie Mae and Freddie Mac (hereafter referred to as the Enterprises). The Mercatus Center at George Mason University is dedicated to advancing knowledge about the effects of regulation on society. With that in mind, this comment does not represent the views of any particular affected party or special interest group. It is designed to help the FHFA as it considers the consequences of its proposed rule. Specifically, the comment seeks to help the FHFA ensure that the enterprises, should they be reconstituted as private firms rather than government agencies, are adequately capitalized, are financially stable, and will not again require a public bailout. By achieving these goals, the Enterprises can serve the public interest in promoting access to affordable housing across the United States.

Our comment points out an apparent contradiction between the FHFA’s stated goals and the proposed rule changes. We begin with a response to question 8, regarding efforts to ease the Enterprises’ capital requirements intended to enhance the marketability of credit risk transfer (CRT) instruments, placing more credit risk with the private sector. After raising some concerns with the proposed approach, we then respond to question 4, regarding the leverage ratio and the proposed changes to make it a nonbinding backstop for the risk-weighted capital standards. Lastly, we attach to this comment Thomas Hoenig’s August 2020 response to the FHFA’s earlier proposal advocating a higher leverage ratio requirement to strengthen the Enterprises’ financial position and protect the public from having to bear undue risk should the Enterprises again encounter adverse economic conditions.

Addressing Question 8: On the Efforts to Ease the Enterprises’ Capital Requirements

The proposed rule asks in question 8 whether the amendments to the CRT securitization framework provide the Enterprises with sufficient incentives to engage in more CRTs without compromising safety and soundness. The FHFA views the transfer of risk, particularly credit risk, to a broad set of investors as an important tool to reduce taxpayer exposure to the risks posed by the Enterprises and to mitigate systemic risk caused by the size and monoline nature of the Enterprises’ businesses.

The proposed rule would reduce capital requirements for the specific purpose of incenting the Enterprises to engage in a greater use of CRTs. Currently FHFA rules specifically acknowledge that CRT tranches, even senior tranches, are not risk free and require the Enterprises to maintain regulatory capital to absorb losses on retained CRT exposures. The FHFA currently requires a 10 percent floor to retained CRT exposure. It also requires an overall effectiveness adjustment that reduces the risk-weighted assets of transferred CRT tranches by 10 percent, thereby reducing the capital relief afforded by CRTs. This adjustment accounts for the fact that a CRT does not provide the same loss-absorbing capacity as equity financing.

The easing of the capital standards will encourage the Enterprises to engage in more CRT transactions, but doing so presents a risk tradeoff. Allowing the Enterprises to increase leverage will encourage them to expand their use of CRTs to reduce the on-balance-sheet credit risk. However, as noted earlier, the increased leverage will increase the Enterprises’ insolvency risk. The current proposal provides little empirical analysis to confirm that there would be a net reduction in risk to the Enterprises. In addition, the FHFA’s proposal to reduce the 10 percent floor for retained CRT exposure to 5 percent and to eliminate the overall effectiveness adjustment further weakens the financial resilience of the Enterprises. The combined effects of the actions could, on balance, increase the Enterprises’ risk profile, reduce the Enterprises’ overall financial soundness, and potentially expose taxpayers to losses.

Addressing Question 4: On the Inconsistency between Concerns and Proposed Changes

On page 53,231 of the published notice of proposed rulemaking, the paragraph says

"FHFA is concerned that certain aspects of the ERCF might create disincentives in the Enterprises’ CRT programs that may result in taxpayers bearing excessive undue risk for as long as the Enterprises are in conservatorships and excessive risk to the housing finance market both during and after conservatorships. This concern is heightened by the fact that the Enterprises presently are severely undercapitalized and lack the resources on their own to safely absorb the credit risk associated with their normal operations."

In contrast to this observation, however, the proposed rule changes would make the leverage ratio a nonbinding constraint on judging the adequacy of capital resources and allowing Freddie Mac to reduce capital by $35 billion and Fannie Mae by $39 billion, for a combined total of $74 billion. Such a reduction in capital works against improving the Enterprises’ capital.

The FHFA argues that maintaining higher capital will cause the Enterprises to take on more risk relative to the risk-weighted capital standards, undermining safety and soundness. The FHFA also argues that lessening the capital requirements will incent the Enterprises to expand their use of CRTs and thereby transfer credit risk to the private sector and protect taxpayers from having to absorb this risk.

To understand the inconsistency between the FHFA’s stated goals and the likely outcomes of the proposal, we point out that, in principle, for firms not in conservatorship, default risk comes primarily from two sources: asset risk and leverage. In addition, although requiring less capital may incent the Enterprises to make greater use of CRTs and reduce taxpayer direct exposure to losses, this does not ensure that the Enterprises are less likely to pose risks to taxpayers while in conservatorship because their risk profile increases with greater leverage. Depending on the relative tradeoff between more leverage and less direct credit risk, we provide estimates that indicate what taxpayers might be on the hook for if the Enterprises were not in conservatorship.

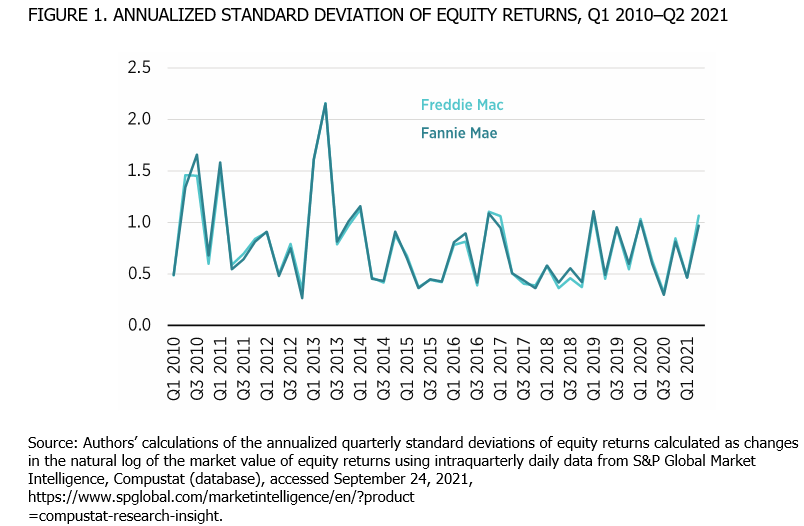

As evidence of the potential taxpayer exposure, consider first that shares of the Enterprises currently trade at about one dollar per share. Using daily data on the market value of equity (price multiplied by the number of shares outstanding) from January 1, 2010, through June 30, 2021, for the Enterprises, figure 1 depicts the annualized quarterly standard deviation of equity returns.

The estimated volatility has ranged from about 30 percent to more than 200 percent since 2010; before the 2007–2009 crisis, stock return volatility for the Enterprises typically equaled about 30 percent and only once exceeded 50 percent, in Q1 2000. Overall, the Enterprises exhibit considerable equity return volatility. We discuss next how inverting that measure of equity return volatility for each firm offers a simple measure of distance to default, a measure of how far each firm is from defaulting.

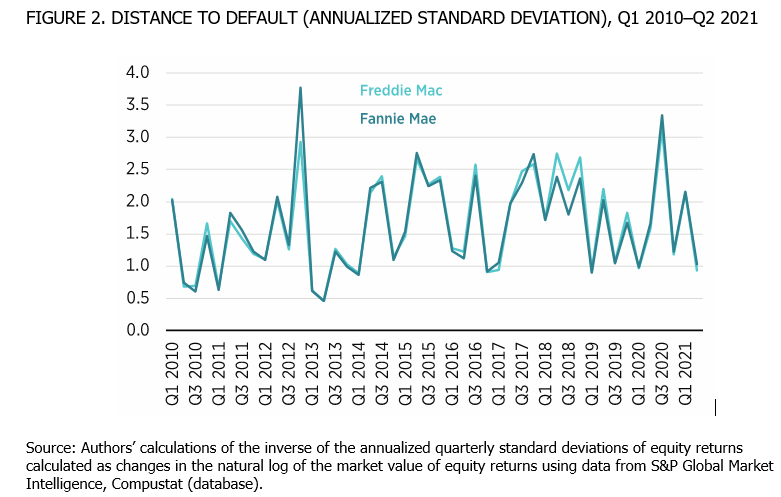

The inverse of the annualized standard deviation of equity returns for the Enterprises, depicted in figure 2, indicates that the market would have concerns about insolvency if the Enterprises were not in conservatorship. Before the 2007–2009 crisis, the average value exceeded 3.0 for each firm, but since 2010 that average has fallen to about 1.6. In Q2 2021, the measure equaled about 1.0, indicating that the market views the Enterprises as still reflecting distress. If the FHFA has concerns about that, then that would be a reason not to lower capital requirements but instead to make plans for the Enterprises to raise equity capital.

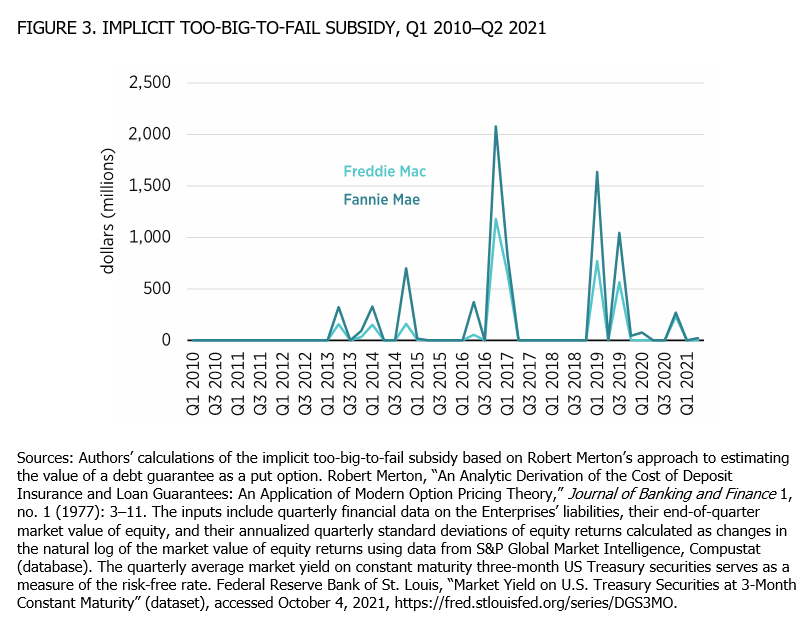

Not only do market values suggest that investors would have concerns about insolvency risk for these firms, but these concerns imply that taxpayers could be on the hook for losses based on the estimated implicit “too big to fail” subsidies. Figure 3 shows that since 2013, the implicit too-big-to-fail subsidies have occasionally reappeared, reaching a peak of about $3.00 billion combined for the two firms ($1.18 billion for Freddie Mac and $2.08 billion for Fannie Mae). By comparison, our approach suggests that the peak value of the too-big-to-fail subsidy equaled $274 billion combined in Q3 2008 ($113 billion for Freddie and $161 billion for Fannie).

Lastly, we highlight that we do not think it makes sense to refer to capital adequacy standards that apply to the largest advanced approaches banks, including Bank of America, BNY Mellon, Citigroup, Goldman Sachs, J.P. Morgan, Morgan Stanley, Northern Trust, US Bancorp, State Street, and Wells Fargo, which are subject to the supplementary leverage ratio and the enhanced supplementary leverage ratio. In figure 4, we depict the market leverage ratio, which is defined as the ratio of the market value of equity to the estimated market value of assets for the Enterprises. By comparison, we also depict the average market leverage ratio for the advanced approaches bank holding companies. Whereas the market leverage ratio for advanced approaches banks exceeds the minimum standards, for the Enterprises it lies close to zero.

Summary

The FHFA’s proposal is intended to move risk from the Enterprises to the private sector and, thus, provide each of the Enterprises with more flexibility in its operations. Although the objective is laudable, our analysis suggests that the outcome, given the fact that the Enterprises remain in conservatorship, could result in even more taxpayer losses rather than fewer. Whether the goal is to end conservatorship by having the Enterprises substantially increase capital or to once again become federal agencies, we recommend that the FHFA consider other options that allow risk to be transferred into the private sector without potentially putting taxpayers on the hook for losses occurring within the Enterprises.

Attachment

Thomas M. Hoenig, “Comment on FHFA Proposed Capital Framework” (Public Interest Comment, Mercatus Center at George Mason University, Arlington, VA, August 26, 2020).

COMMENT ON FHFA PROPOSED CAPITAL FRAMEWORK

Enterprise Regulatory Capital Framework

Agency: Federal Housing Finance Agency; Office of Federal Housing Enterprise Oversight

Comment Period Opens: June 30, 2020

Comment Period Closes: August 31, 2020

Comment Submitted: August 26, 2020

Docket No. 2020-11279

RIN: 2590-AA95

I appreciate the opportunity to submit a comment to the Federal Housing Finance Agency (FHFA) in response to its proposed rulemaking addressing the capital adequacy of Fannie Mae and Freddie Mac (hereafter referred to as the enterprises).1 The Mercatus Center at George Mason University is dedicated to advancing knowledge about the effects of regulation on society. With that in mind, this comment does not represent the views of any particular affected party or special interest group. It is designed to help FHFA as it considers how to best implement its proposed rule. Specifically, the comment seeks to help FHFA assure that the enterprises, as private firms, are adequately capitalized, financially stable, and will not again require public bailout. By achieving these goals, it is expected that the enterprises will best serve the public interest in promoting access to affordable housing across the United States.

This comment addresses several aspects FHFA’s re-proposed capital rule for the enterprises, including the following:

- Support for proposed changes affecting the weighting schemes used in its risk-weighted models

- Support for proposed changes affecting mark-to-market countercyclical adjustments, credit risk transfers, and prescribed capital conservation buffer amounts

- A recommendation to use a single definition of capital for public disclosure purposes

- A recommendation to use Tier I capital rather than adjusted total capital when defining both the risk-weighted and leverage ratios and standards (because adjusted total capital, used when computing the risk-weighted ratio, overstates the enterprises’ loss-absorbing capacity)

- A recommendation that the minimum leverage ratio be set higher than 4 percent of adjusted total assets

- A recommendation that the risk-weighted and leverage ratios be interchanged as primary and backstop measures when judging the enterprises’ capital adequacy

DEFINITIONS OF CAPITAL

The proposed rulemaking incorporates five different definitions of the enterprises’ capital, each relying on different measurements. Two are statutory definitions and three are supplemental definitions. All the definitions use measurements of equity: four use measurements of preferred stock; one uses measurements of excess credit reserves and subordinated debt; and another uses a measurement of a portion of other comprehensive income. Also, four of the definitions account for regulatorily-required deductions and adjustments for certain deferred tax assets, goodwill, and other intangible assets that have little loss-absorbing capacity when enterprises are under financial stress. Ultimately, FHFA relies on two of the five definitions to establish the enterprises’ minimum capital requirements. Adjusted total capital is used to set the risk-weighted capital requirement, and Tier I capital is used in setting the leverage ratio requirement. Adjusted total capital includes subordinated debt and a portion of credit reserves, while Tier I capital does not.

Having multiple definitions of capital serves to confuse the public as much as it serves to inform it, and it impedes transparency. FHFA should select a single capital definition for calculating both the risk-weighted and leverage ratios. Doing so would more clearly and consistently inform investors and the public regarding the enterprises’ financial strength and ability to absorb unexpected losses.

Supplemental Tier I capital serves this purpose best. It is defined as common equity, noncumulative preferred stock, and a portion of other accumulated comprehensive income (AOCI). Also, unlike adjusted total capital, supplemental Tier I capital excludes subordinated debt, which has no loss absorbing capacity and for which interest payments—unlike dividends—cannot be suspended without risking default. Tier I capital, therefore, should be the common numerator for both the riskweighted and leverage ratios, reported appropriately as Tier I risk-weighted capital and Tier I leverage.

RISK-WEIGHTED CAPITAL RATIO

The risk-weighted capital ratio is composed of a base ratio, defined as adjusted total capital to riskweighted assets, plus a prescribed capital conservation buffer amount (PCCBA). FHFA relies principally on a model-based approach for estimating risk-weighted assets, and it proposes adjusting certain of the model’s weighting schemes to better align risk with assets and capital with risk assets. These adjustments are improvements to the process of assigning risk weights among assets and should be incorporated in the revised rule.

Additional changes and additions, discussed below, would affect the mark-to-market loan-tovalue (MTMLTV) adjustment, the countercyclical adjustment factor, and the treatment of credit risk transfers (CRT). Lastly, the proposed rulemaking would add several enhancements to the PCCBA.

MARK-TO-MARKET COUNTERCYCLICAL ADJUSTMENTS

The proposed rulemaking introduces useful countercyclical adjustments of single-family MTMLTV amounts when measuring risk-weighted assets, which should be adopted. Asset values and capital requirements are modified depending on the movement of current house prices relative to their long-run trend. These adjustments serve to moderate the effects of sharp changes in house prices on the enterprises’ capital requirements, and their potential procyclical effects on the housing market are a reason the proposed rulemaking should be adopted.

ADJUSTMENT TO CREDIT RISK TRANSFERS

Changes affecting the enterprises’ use of CRTs are intended to better account for the limitations in transferring balance sheet risks to a third party. While CRTs transfer credit or other risks to a counterparty, some level of risks remains related to timing, quality of the security, and the ability of the counterparty to pay as promised. The proposed rulemaking, therefore, correctly acknowledges that CRTs do not provide the same loss-absorbing capacity as equity capital and appropriately require enterprises to retain some amount of capital to allow for this risk.

PRESCRIBED CAPITAL CONSERVATION BUFFER AMOUNT

The PCCBA is composed of a countercyclical buffer, a stress buffer, and a stability buffer. It is measured as a percentage of adjusted total assets rather than of risk assets. This feature, as the proposed rulemaking notes, serves to promote greater stability through the economic cycle. The countercyclical component would be implemented at the discretion of FHFA, depending on macroeconomic conditions. It is similar to the one defined for the banking industry, and FHFA will coordinate its application with bank supervisors. The stress component of the buffer is 0.75 percent of adjusted total assets and provides the enterprises an additional margin of capital to absorb unexpected loss from significant but temporary adverse events. FHFA correctly recognizes that the 0.75 percent stress buffer component should be periodically reviewed and adjusted as needed.

The stability component of the buffer adjusts capital levels to recognize the potential systemic disruption that a failure of the enterprises would have on the housing market. Importantly, it is rule based and dependent on the enterprises’ relative concentration of industry loans. The inclusion of the stability buffer reflects lessons learned from past crises. The housing market and the enterprises’ dominant role in funding this market have a profound effect on the economy, which should be accounted for in setting capital standards. The proposed rulemaking also asks for suggestions on possible alternative measures to define this buffer; however, estimates of the enterprises’ systemic effect are subject to any number of influences and to significant error, and no other method would necessarily be superior.

While providing a significant additional margin of capital, the PCCBA also provides the enterprises’ useful flexibility in maintaining capital over the economic cycle. As long as capital remains greater than total minimum requirements, no restrictions on operations would likely be imposed. Should the ratio decline to less than the minimum required level but within the buffer, enterprises would have the opportunity to rebuild capital with limited operational restrictions, including only gradual reductions in capital distributions. Thus, FHFA’s use of the PCCBA serves to mitigate potential procyclical effects that strict capital minimums would otherwise have on the enterprises’ operations and on the broader housing market.

Overall, if FHFA chooses to implement a risk-weighted capital program for enterprises, these modifications represent improvements to the proposed rulemaking and should be included in the final rule. However, as proposed, the risk-weighted capital standard generally overstates the percentage of loss-absorbing capital relative to risk assets. To address this weakness, Tier I capital, rather than adjusted total capital, should be used to define the risk-weighted capital ratio.

RISK-WEIGHTED CAPITAL RATIO OVERSTATES CAPITAL STRENGTH

Using the enterprises’ financial reports from September 2019, FHFA provides an example of the minimum amount of capital required under the proposed risk-weighted capital rule. The estimate, $234 billion in adjusted total capital (Tier I capital, subordinated debt, and a portion of credit reserves) plus a PCCBA, divided by $1,686 billion of risk-weighted assets, is 13.9 percent. However, to the extent that this equation includes debt, the risk-weighted capital ratio may overstate enterprises’ capacity to absorb unexpected loss. In this example, by excluding any debt or excess credit loss reserves as capital, the ratio’s numerator would decline to a Tier I amount of $200 billion dollars, or 11.9 percent of risk-weighted assets, reflecting the $34 billion reduction. As noted earlier, Tier I capital, which excludes subordinated debt and credit reserves, more accurately represents the percentage of loss-absorbing capital relative to risk assets. Therefore, to enhance the transparency and clarity of the risk-weighted capital ratio, it should be redefined and recalibrated using Tier I capital only.

Finally, the proposed rulemaking would impose a floor on the adjusted risk weights for singlefamily mortgages of 15 percent. Such a floor acknowledges the difficulty of relying on models to fully identify relative risks within the different asset classes or to provide a fully dependable estimate of risk-weighted assets. It also recognizes the incentives to arbitrage based on the enterprises’ balance sheet to maximize leverage. If the risk-weighted capital minimums were the best means to judge the enterprises’ risk and capital requirement, this floor would be unnecessary.

LEVERAGE CAPITAL RATIO

The leverage ratio is proposed as a capital backstop for enterprises, below which capital could not decline, regardless of the minimum estimated using the risk-weighted ratio. It is defined as Tier I capital divided by adjusted total assets. Tier I capital is composed principally of equity capital and is the best measure of the enterprises’ loss-absorbing capacity. Adjusted total assets is defined as total assets under generally accepted accounting principles, adjusted for certain off-balance-sheet risk items such as loan commitments and derivatives. FHFA proposes a minimum leverage ratio of 4 percent, which, as discussed later, is insufficient to assure greater stability and should be increased to at least 5 percent.

The leverage capital ratio does not assign relative risk weights to assets and does not attempt to anticipate the source or the predictability of loss, whether from credit exposures, market spreads, or operations. Also, the leverage ratio, by excluding debt, informs investors and the public of approximately how much loss the enterprises can absorb relative to total assets before insolvency occurs. This is a clearer and more reliable indicator of an institution’s financial resiliency.

The proposed rulemaking sets 4 percent as the minimum required leverage ratio, composed of a 2.5 percent base and a 1.5 percent capital buffer. Using September 2019 financial data, FHFA estimates that the 4 percent required Tier I capital would be $243 billion (4 percent of $6,076 billion in adjusted total assets).

Based on past events, FHFA’s proposed 4 percent Tier 1 leverage ratio most likely leaves enterprises vulnerable to unexpected adverse shocks. In setting the minimum ratio at 4 percent, FHFA notes that this percentage is comparable to the one selected for the banking industry. While this acknowledgement is correct, it raises the question of whether 4 percent is adequate to preclude the enterprises’ having to be placed into conservatorship should they encounter a significant crisis in the future. FHFA notes, for example, that the enterprises’ peak losses during the Great Recession (adjusted for comparability) were approximately 3 percent of total adjusted assets. Thus, should the enterprises’ Tier I capital decline to 1 percent, it is likely that they would once again require government assistance.

Some commentators may question whether setting the minimum leverage ratio at 4 percent would provide sufficient returns to attract private investment. This should be carefully evaluated, but it is doubtful that it would inhibit investor interest. For example, based on 2019 financial reports, if enterprises were required to maintain a higher 5 percent leverage ratio while earning a 1 percent return on assets (similar to the return earned in the banking industry), returns on equity would be roughly 20 percent, which is competitive with other industries’ returns. Thus, the tradeoff between more capital and greater returns should not necessarily inhibit investor interest.

RISK-WEIGHTED RATIO OR THE LEVERAGE RATIO

Using the example presented in FHFA’s proposed rulemaking, calculating both the risk-weighted and leverage ratios using Tier I capital in the numerator makes for a more direct comparison of how much loss-absorbing capital is required under each measure. As noted earlier, based on FHFA’s example, the minimum risk weight capital requirement under the proposed rulemaking would be $234 billion (adjusted total capital to risk weighted assets plus the PCCBA). However, adjusted total capital can include approximately $34 billion of debt and credit reserves, which means as little as $200 billion would be Tier I equity. Under the leverage ratio, which allows only Tier I equity in the calculation, even the 4 percent Tier I capital to adjusted total assets is a significantly higher amount of $243 billion.

For greater clarity and transparency, therefore, FHFA should use only Tier I capital in the numerator for both the risk-weighted capital and leverage ratios. In addition, if the leverage ratio is to be the backstop capital measure, the minimum levels should be recalibrated to increase the riskweighted minimum ratio, decrease the leverage ratio, or both. Once in place, these ratios would be far more effective in capturing and comparing relative shifts in the enterprises’ risk assets, changes in leverage, and overall risk levels.

Finally, given the comparative results discussed earlier and given that the risk-weighted capital standard has shown mixed results in the past, FHFA should designate the leverage ratio as the primary measure for setting the enterprises’ minimum capital requirements. The housing market is dynamic and highly volatile, while the risk-weighted measure, even with the proposed changes, is static, since regulators are slow to change risk weights as markets change. It is also highly complex and open to manipulation. The leverage ratio is simpler and clearer in its information, since it identifies the enterprises’ total loss-absorbing capacity relative to total assets, regardless of source.

An objection to using the leverage ratio is that it fails to distinguish degrees of risks among assets, and if it were the primary standard, it would give managers an incentive to take on riskier assets for a given level of capital as a means to increase investor returns. Assuming the minimum leverage ratio is set appropriately, this outcome is unlikely. However, an antidote to this concern is to incorporate risk analysis into the stress test as the backstop to the leverage ratio. Different assumptions can be made to analyze and judge the effects of potential changes in risks among assets. FHFA staff, trained in the highly technical and complex details of a risk analysis, could best measure and provide a check in the event that management increases the enterprises’ portfolio risks over time.

CONCLUSION

FHFA’s proposed rulemaking improves the usefulness of the risk-weighted capital analysis introduced in an earlier proposal to establish minimum capital requirements for the enterprises. Nevertheless, it requires that FHFA assume that its models can anticipate and accurately measure shifting risks within a highly dynamic market, which too easily misleads the public regarding the enterprises’ financial resiliency. This public interest comment, while recognizing improvements to the proposal, offers several recommendations to strengthen it further for judging the enterprises’ capital and financial strength. I appreciate the opportunity to offer these recommendations and would be pleased to provide FHFA follow-up comments should they be helpful.