- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

ACA Indexing Provisions: A Reality Check

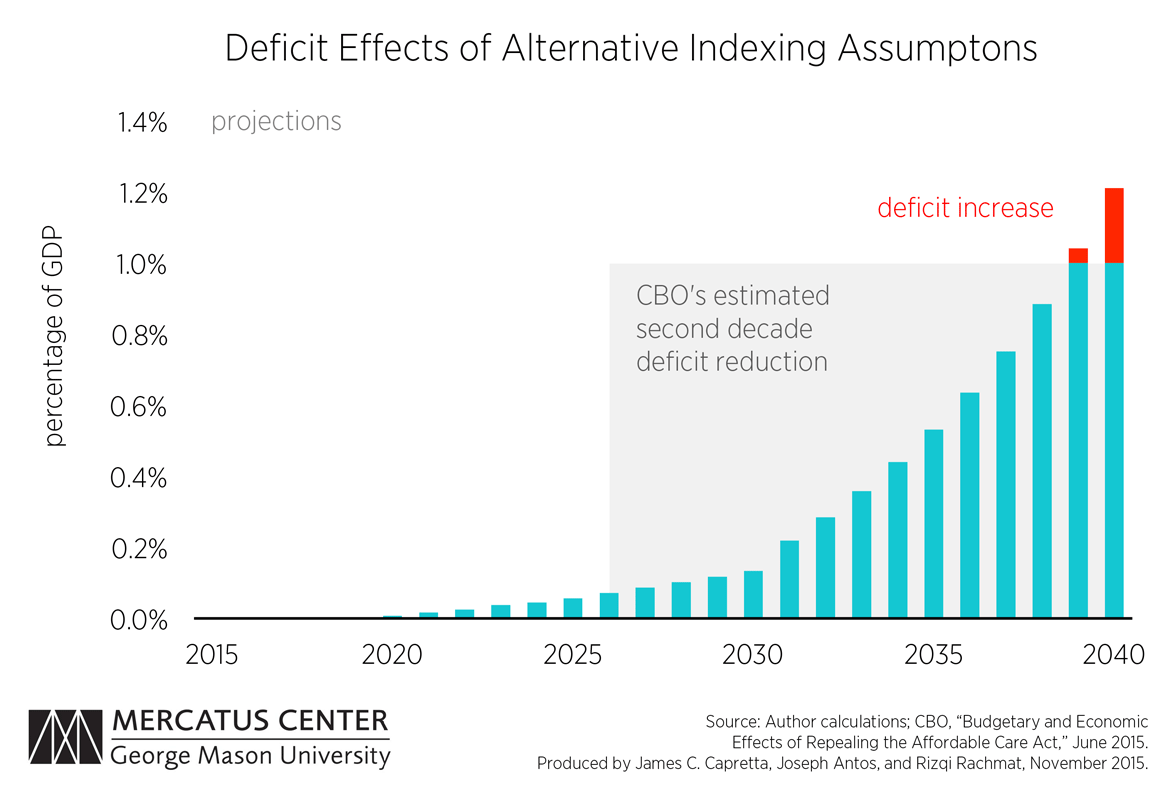

The ACA contains indexing provisions that are set to automatically reduce federal payments for health services or increase tax revenues every year into the future. CBO estimates show that the ACA will reduce future deficits by about 1.0 percent of GDP in the decade beyond the current 10-year budget window (roughly 2026–2035). This projection assumes uninterrupted implementation of the ACA’s aggressive indexing adjustments, but historical precedent tells us that these indexing measures will not be implemented as stated. The first chart below estimates, based on reasonable adjustments to the implementation of the indexing provisions, the presumed second decade deficit reduction of 1.0 percent of GDP will be eliminated and the ACA will start to increase the federal deficit.

The Affordable Care Act (ACA) passed Congress largely because it promised to offer health insurance to millions of Americans while simultaneously lowering projected annual federal budget deficits. The Congressional Budget Office’s (CBO) conclusion that the ACA would reduce the deficit is widely cited, but poorly understood. In a new study, we demonstrate that this promise of deficit reduction is fragile, and modest changes in implementation would wipe out presumed future deficit reduction.

The ACA contains indexing provisions that are set to automatically reduce federal payments for health services or increase tax revenues every year into the future. CBO estimates show that the ACA will reduce future deficits by about 1.0 percent of GDP in the decade beyond the current 10-year budget window (roughly 2026–2035). This projection assumes uninterrupted implementation of the ACA’s aggressive indexing adjustments, but historical precedent tells us that these indexing measures will not be implemented as stated.

The first chart below estimates, based on reasonable adjustments to the implementation of the indexing provisions, the presumed second decade deficit reduction of 1.0 percent of GDP will be eliminated and the ACA will start to increase the federal deficit.

One of the indexing provisions, intended to increase revenues, are taxes designed to look as if they will be paid only by those with a “high income.” These high-income taxes are the Medicare Hospital Insurance (HI) tax add-on of 0.9 percent of earnings (bringing the tax from 1.45 percent to 2.35 percent), and a new 3.8 percent tax on net investment income. Each of these taxes applies to earnings over $200,000 for individual taxpayers and $250,000 for married couples.

The income thresholds stated are not indexed to inflation or wage growth. The result of not indexing the $200,000 and $250,000 thresholds is that over time more individuals and households will begin to fall into this high-income bracket.

The second chart shows authors’ estimates that by 2033, 20 percent of households will pay the high-income taxes, and 40 percent of households will pay the taxes in 2045. If the thresholds are left as they are, these taxes will begin to hit the middle class and will no longer be taxes only on those with a high income.

If, however, these two taxes were indexed to either inflation or wage growth in order to remain high-income taxes, the revenue generated from them would drop drastically and would be insufficient to reduce the deficit as projected by the CBO. It is reasonable to assume that future action will be taken to index these taxes to either inflation or wage growth, because this tax strategy has been tried before.

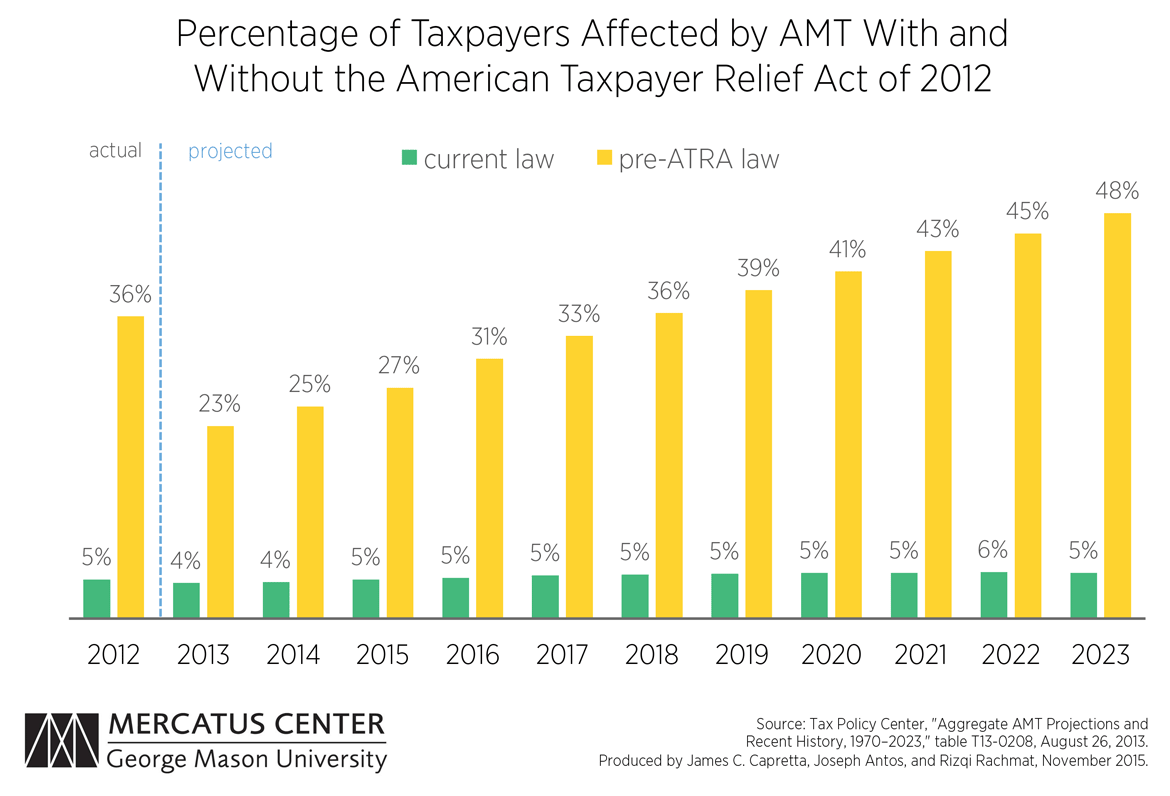

Learning from the Alternative Minimum Tax

In 1969 the “Alternative Minimum Tax” (AMT) was enacted to ensure that wealthy taxpayers paid a minimal amount of tax and could not overuse deductions and loopholes. The AMT was not indexed to inflation, so the number of AMT taxpayers continued to grow over time. As the tax began to hit the middle class it became less popular and Congress was called to act.

Congress acted with the Economic Growth Tax Relief Reconciliation Act, the Job Growth Tax Relief Reconciliation Act, and the American Taxpayers Relief Act (ATRA) to reduce the percentage of taxpayers affected by the AMT. ATRA permanently indexed the AMT parameters to inflation, thereby lowering the percentage of taxpayers paying the AMT–this is shown below in the third chart. Without congressional action, it is estimated that by 2023 close to 50 percent of taxpayers would have been paying a tax meant for high-income individuals.

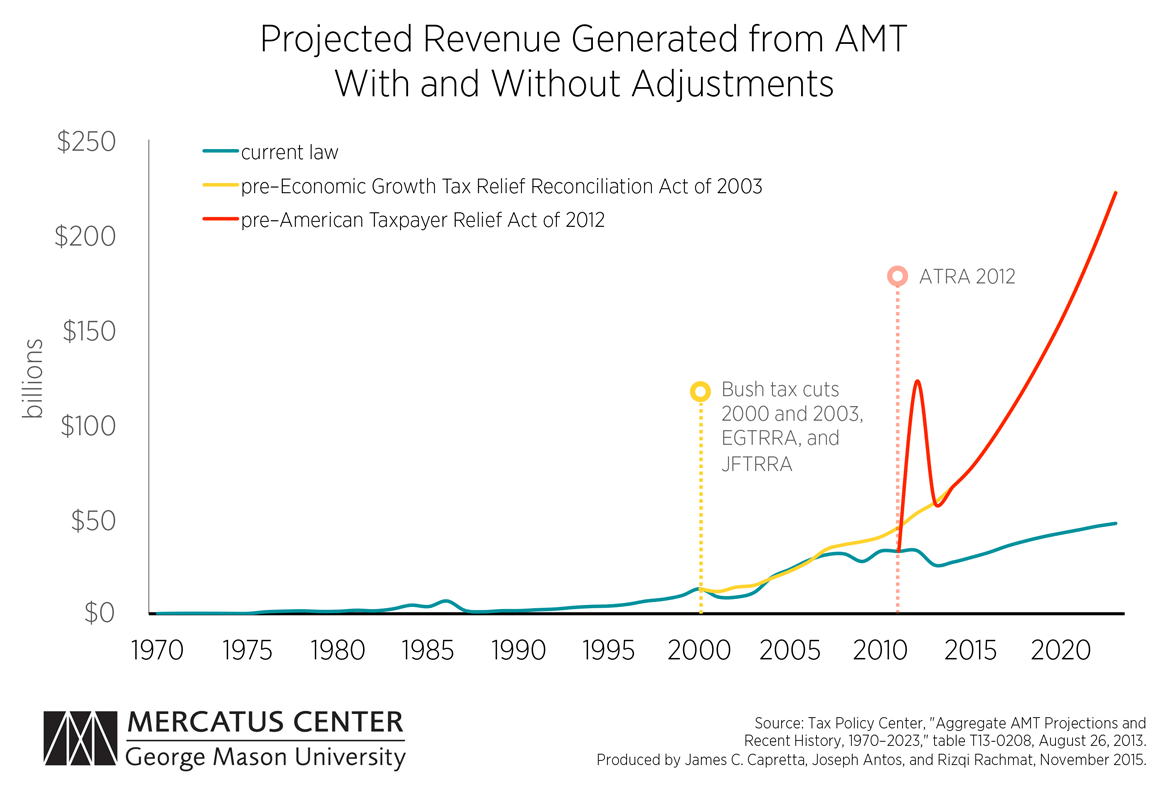

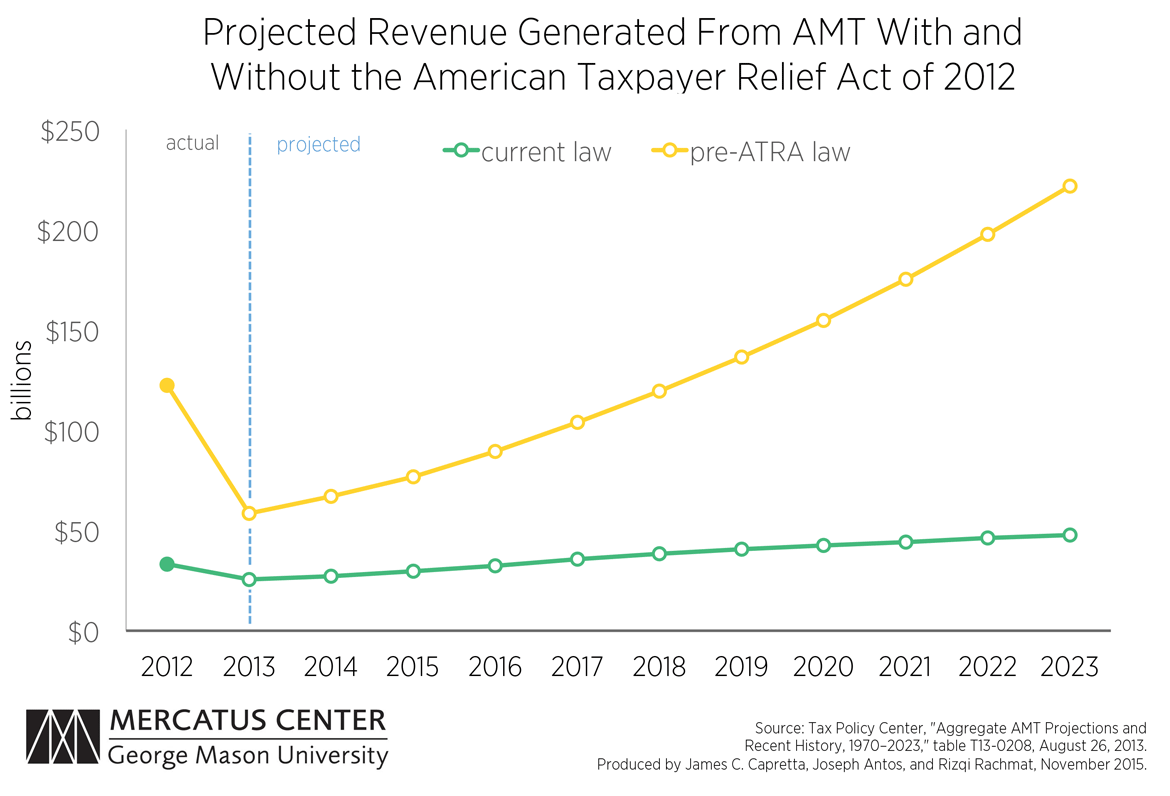

The fourth and fifth charts demonstrate how the smaller AMT tax base (created through various legislative action) impacted revenue generation. It is clear that the amount of revenue generated from the AMT decreased dramatically from where it is projected to have been if it had not been modified by Congress.

The ACA’s taxes on high-income households are likely to follow historic precedent and eventually be indexed for inflation, producing significantly less revenue than projected. With less revenue generated, the ACA is unlikely to meet projected reductions in the federal deficit.

The high-income taxes are just one of four key indexing provisions in the ACA, and each one will encounter serious flaws as it is implemented. Pressure will inevitably build to modify the implementation of these provisions, and even small modifications can quickly turn the ACA into a drain on the federal budget.

Related Content

- | Healthcare Healthcare

- | Policy Briefs Policy Briefs

What’s Holding Back the Supply of Innovative, Consumer-Friendly Medical Services?

- | Government Spending Government Spending

- | Research Papers Research Papers

Indexing in the Affordable Care Act: The Impact on the Federal Budget

- | Government Spending Government Spending

- | Research Papers Research Papers

The Budget Act at Forty: Time for Budget Process Reform

- | Government Spending Government Spending

- | Books Books

The Economics of Medicaid: Assessing the Costs and Consequences