- | Government Spending Government Spending

- | Policy Briefs Policy Briefs

- |

Are Fiscal Rules an Effective Restraint on Government Debt?

The United States is on an unsustainable fiscal trajectory. Projected spending, deficit, and debt levels continue to grow automatically, fueled predominantly by a rapidly aging population causing expansions in the number of Social Security and Medicare beneficiaries.

The best way to address the United States’ current fiscal dilemma may be found in implementing fiscal rules, as the federal budget process as it exists today has proven inadequate: the budget is rarely completed on time, and the budget process often involves partisan disputes and political scheming, which results in budget crises at regular intervals, fiscal cliffs, government shutdowns, overreliance on stopgap funding bills, and constantly ignored statutory deadlines and budget rules. Much of the debate surrounding budget process reform involves corporate welfare and earmarked spending (items slipped into legislation by lawmakers to benefit particular special interests). As Chris Edwards at the Cato Institute notes, “With more than 1,800 different subsidy programs, the federal budget has become a giant favor factory for organized pressure groups at the expense of average citizens.” It is no surprise then, that each new budget contains more spending than the last.

This policy brief will assess the underlying problems with the United States’ budgetary process and the issues that arise as a result of the country’s current fiscal trajectory. We explore the role that spending rules play in restraining the growth of government spending wherever they are implemented. Through reviewing the existing literature on fiscal rules, we attempt to determine which aspects of effective fiscal rules are most successful in curtailing government largesse. Finally, we highlight four international examples of countries where the implementation of fiscal rules has been associated with a declining debt-to-GDP ratio and broadly sustainable patterns of government spending.

The US Federal Budget Process Is Broken

The budgeting process is broken, and it has been broken for a long time. Since the enactment of the Congressional Budget and Impoundment Control Act of 1974—which dictates the current budgeting process rules and was intended to make Congress more accountable—Congress has passed all 12 of its discretionary spending bills on time only four times. And when Congress has passed the bills on time, it has used omnibus bills (giant spending bills containing all 12 smaller appropriations bills) or short-term continuing resolutions.

This situation has led policymakers and observers to propose fixes to the budget process. One example is the recurring idea that Congress should replace an annual budget with a biennial budget (one that would cover two fiscal years). Supporters argue that a longer budget period would give legislators more time to conduct oversight of federal programs and, thus, more time to weigh competing spending desires.

According to supporters of a biennial budget, with more time, spending would be better targeted toward programs that work, while those that don’t work would either be fixed or see their funding cut, thanks to better oversight. There is a lot of wishful thinking that goes into this belief. In reality, looking at the 19 states that currently have such a process in place (down from 44 a few decades ago), we find quite the opposite. Biennial budget states actually spend more money, owing to the increased likelihood of supplemental appropriations, while oversight remains flat.

In truth, congressional oversight is highly overvalued. In many cases, oversight is merely an opportunity for politicians to make statements that can be used during political campaigns. Basic public choice theory shows that politicians are motivated fundamentally by self-interest rather than by the public’s interest, which is ostensibly the purpose of congressional oversight.

The same can be said about budget-process reform. The late Stan Collender argued that the process actually works exactly like legislators want it to work. Indeed, for all the complaints made about the budget process, it is a great way to enable politicians to do what they want to do (cater to interest groups) while avoiding what they don’t want to do (living within their means).

The problem is made more intense by the growth of mandatory spending. Spending on programs such as Social Security, Medicare, and Medicaid, as well as interest payments on the public debt, aren’t appropriated each year like discretionary programs are (e.g., education, transportation, and defense). As the number of people benefiting from mandatory programs grows and the eligibility rules are relaxed, a large and growing share of the budget is spent on those programs. Today, 70 percent of the budget goes to these programs, as opposed to 40 percent in 1970. Politicians, therefore, have less money to fling around on new spending meant to carry voter favor.

It is true that some members of both houses talk about reforming the budget process to make it more rigorous and fiscally responsible. They have even formed House and Senate budget committees and held hearings on the issue. However, as Collender argued, “[T]his activity is less designed to retool the budget process than it is to placate all those who are so fervently saying that it needs to be reformed: the interest groups, think tanks and associations that make up the inside-the-Beltway federal budgeting community.”

The negative consequence emerging from this chaos and the resulting failure to follow budget rules is an unremitting expansion of the size and scope of government and the US debt. The gross debt has more than doubled in the past 10 years and has now passed $22 trillion. If debt expansion continues as projected, the US government will find itself in a tough spot, exposed to the risk of interest-rate hikes, to an inability to respond to emergencies, and, possibly, to slower growth.

The United States’ public debt problem is often highlighted as a future risk, meaning that most of the discussion surrounding the burden of US public debt is focused on the future risk of default or on the costs to future taxpayers of having to close the funding gap. However, recent research by Thomas Grennes, Qingliang Fan, and Mehmet Caner reveals that the United States’ excessive debt burden has an immediate cost: economic stagnation. The authors estimate that in the period 1995–2014, US economic growth would have been more than 1 higher if not for the excessive debt burden, since fewer funds are available for private investment as the government borrows to increase its spending.

Concerns over how to design a better budget process for limiting the growth of government aren’t new. Discussing Adam Smith’s worries on the issue, F. A. Hayek wrote in 1948 that “Smith’s chief concern was not so much with what man might occasionally achieve when he was at his best but that he should have as little opportunity as possible to do harm when he was at his worst. It is a social system which does not depend for its functioning on our finding good men for running it, or on all men becoming better than they are now, but which makes use of men in all their given variety and complexity, sometimes good and sometimes bad, sometimes intelligent and more often stupid.”

1986 Nobel laureate James Buchanan further developed the notion that good fiscal rules are key to controlling government spending and borrowing. His extensive body of work shows that, in theory, fiscal rules can restrain budgets by tying politicians’ hands. In practice, as the underlying structural roots of budget deficits have become more widely understood, a growing number of countries have adopted fiscal rules to restrict policymakers and reshape democratic governance.

What the Existing Literature Says about Fiscal Rules

With countries around the world experiencing growing debt-to-GDP ratios, resultant stagnation in economic growth, and, in extreme cases, default on debts, academics have been paying an increasing amount of attention to the potential of rules toward restraining unsustainable deficit spending.

Marina Halac and Pierre Yared find that in 1990 only seven countries had fiscal rules in place, but by 2015, 92 countries had adopted them. Governments across the world have been adopting mandated deficit, spending, or revenue limits to restrict fiscal policy and curtail further increases in government debt.

A growing number of empirical studies demonstrate that the introduction of fiscal rules leads to smaller fiscal deficits, lower output volatility, lower sovereign interest rates spreads, and greater fiscal maneuverability.

Several studies among the academic literature provide evidence for the effectiveness of fiscal rules in restraining government spending growth. Data from a panel of EU member states suggest the existence of a procyclical bias in expenditure policy in those countries. However, numerical expenditure rules reduce this bias. The institutional design of fiscal rules reflects political willingness to address high levels of expenditure relative to GDP. Expenditure rules tend to restrain expenditures and also mitigate the effect of shocks on expenditure developments. Another dataset covering 33 expenditure rules from 1985 to 2013 shows that compliance with expenditure rules is greater than compliance with balanced budget rules—particularly if the compliance rules are enshrined in law—and that the presence of expenditure rules is associated with stronger fiscal performance.

Policymakers respond to certain incentives, which leads to a deficit bias in the budgetary process. Alberto Alesina and Francesco Giavazzi describe these incentives as the following: vulnerability to time inconsistency, the burden of an aging population with the need to pay social security and medical benefits, special interests vying for financial favors, and state and local governments expecting to receive transfers from the central government. Any fiscal rule arrangements must offset these perverse incentives. Alesina and Giavazzi recommend (1) delegating oversight to independent agents, (2) binding numerical rules, and (3) a better budgetary process.

Delegating oversight of fiscal rules to an independent agent is a common feature in countries that have adopted broadly successful spending limits. Recent research by Roel Beetsma and coauthors provides some evidence that the presence of fiscal councils seems to eliminate biases in budgetary forecasts and improve the accuracy of those forecasts. Another observation of countries that delegate oversight to an independent council is that those independent councils appear to foster compliance with budget balance and expenditure rules through their influence on the accuracy of budget plans. Xavier Debrun and Lars Jonung highlight the key role that fiscal councils play in amplifying the reputational effects of unwarranted deviations from the benchmark. The authors argue that such deviations should “prompt the fiscal council to raise alarm, encouraging reactions from parliament, the voting public and market participants that improve fiscal behavior.”

An independent fiscal council overseeing the budgetary process is more likely to enhance fiscal discipline if a broad mandate allows it to address various deficit biases. Xavier Debrun finds that a member of the council is more effective if he can trigger a public debate where elected officials would have to publicly explain fiscal slippages deemed inappropriate by the council. By acting as a reliable source on the status of fiscal health, an independent council member can help identify inappropriate policy deviations and hold policymakers accountable.

In an attempt to review existing state budget institutions within the United States, Matt Mitchell and Nick Tuszynski have examined how different budgetary institutions affect per capita spending within the United States. They find that states with strict balanced-budget requirements spend less compared to states with weak requirements, and they also tend to have larger rainy-day funds and larger budget surpluses. However, the institution in their study that reduced per capita spending most significantly was the separation of spending and taxing committees. As Mitchell and Tuszynski explain, the idea is essentially Madisonian: “If one committee has jurisdiction over taxing but not spending, its members—unable to steer spending projects toward their constituents—will have an incentive to block the interests of other committees with spending authority.” In a more up-to-date study on the fiscal effect of separate taxing and spending committees in state legislatures, Matt Mitchell and Pavel Yakovlev find that, controlling for other factors, states with separate taxing and spending committees spend between $300 and $450 less per capita than states without separate committees.

By adjusting the institutions that govern the budgetary process, policymakers can promote the much-needed long-term thinking that is often absent from the fiscal decision-making process. Matt Mitchell and Olivia Gonzalez have outlined four main principles that policymakers can use to guide their design of rules that shape the budget process:

1. Broad scope. Applying a budget rule to all spending categories forces legislators to subject all spending to cuts and reduces the incentive for future lawmakers to place their favorite items beyond the scope of these rules.

2. Few escape clauses. Legislators should not have opportunities to sidestep the rule. If an escape clause is to be used, the threshold for activating it should be high.

3. Minimal accounting discretion. Too much discretion leads policymakers to create new spending categories, such as “off-budget” programs not subject to the rules.

4. Enforcement. Constitutional rules are typically the most binding rules because they provide a check against legislative discretion.

While fiscal rules that are exceedingly tight tend to be unsuccessful owing to conflicts with broad political objectives, fiscal rules that are too soft are ultimately useless. No set of fiscal rules will make much of a difference to the budgetary cycle if it is limited to the short term (a single year), if enforcement is weak, and if potential future impacts are ignored during the budget process. Allen Schick lays out five changes in budgeting that are essential for fiscal rules to be effective: (1) lengthening the time frame from a single year to the medium term, (2) projecting a baseline of future budget conditions, (3) estimating the impact of policy changes on future budgets, (4) developing procedures for monitoring budget outturns and taking corrective action when necessary, and (5) establishing enforcement mechanisms to assure that opportunistic politicians do not breach the rules. Applying these changes in budgeting practices is a matter of finding the fine line between tight and soft fiscal rules and minimizing the deficit bias of policymakers.

Fiscal institutions that are bounded by long-term targets will yield long-term increases in revenue or reductions in expenditures. This is why it is important to embed fiscal restraints within a medium-term or long-term framework that sets a ceiling on expenditures for the coming years and even decades. Allen Schick makes the case for budget allocation decisions to be driven by long-term goals and policies to be based on their estimated effects on budget goals 5, 10, or 20 years into the future. However, this view of long-term budget rules has been criticized by some as an inadequate solution to our fiscal dilemma. Joseph White highlights the severe difficulties in estimating future totals, projecting effects of policy changes, and matching details to totals.

An important measure of success for fiscal rules is the rate of compliance with such rules. Analysis of more than 50 fiscal rules across 20 European countries identified an average compliance of 51 percent. However, rules covering larger parts of the general government finances, independent monitoring, and enforcement bodies are associated with a significantly higher probability of compliance. For advanced economies, compliance rates for expenditure rules tend to be around 70 percent, while debt rules tend to result in lower compliance and balanced budget requirements tend to have the lowest rates of compliance. These findings are also consistent with those of Cordes et al. and Wolf Heinrich Reuter, which show that expenditure rules are complied with more often than other types of fiscal rules, especially if they are set out in coalition agreements or statutory law and entail specific nominal targets.

Strictness of actions in response to noncompliance also has a strong positive relationship with the compliance rate of fiscal rules—the stricter the actions set out for noncompliance, the higher the average rate of rule compliance. In the case of Reuter’s study of European fiscal rules, rates of compliance were 61 percent for countries with automatic sanctions or correction mechanisms, compared to an average compliance rate of 43 percent for countries with no predefined action. The same study also finds that countries that adopt fiscal rules on a higher legal basis tend to have slighter better compliance rates. That is, legally enshrined laws and constitutionally binding rules have greater compliance than political commitments—51 percent and 53 percent versus 43 percent.

Fiscal rules alone may not achieve fiscal restraint without appropriate fiscal budget institutions. For example, an expenditure limit may only be effective in restraining spending if an independent council has the ability to oversee the budget process, evaluate debt sustainability, and determine whether proposed spending is consistent with medium-term projections for public finances.

The results of several studies suggest that compliance with fiscal rules can be as high as 70 percent or more if the conditions to comply are met. Compliance increases by 0.6 percent for every 1 percent larger coverage of total general government finances, and increases on average 29 percent if there is a mechanism of real-time monitoring of rules and an alert if there is risk of noncompliance.

The good news is that the evidence suggests that these fiscal rules are broadly effective at restraining deficit spending. Comprehensive data covering many years show that countries with such rules have annual budget deficits that are smaller by an average of 0.5 percent of GDP when compared to countries without such rules.

The bad news is that not all fiscal rules are effective in restraining government profligacy and curtailing debt growth. For example, Yale University economics professor Marina Halac and Pierre Yared find that rules based on outcomes (such as a constitutional rule limiting spending growth to a certain percentage of GDP) tend to work better than rules based on short-term and arbitrary restraints, such as the sequestration requirement included in the debt ceiling deal of 2011, which can be lifted very easily.

The existing literature tends to show that the debt problem is rooted in factors related to democratic governance. This is particularly the case in the United States, where applying fiscal rules would face several key challenges. Elected officials are primarily concerned with short-term political and economic outcomes at the expense of long-term considerations. This short-term focus is driven, in great part, by an aging population whose concerns about their current situation far outweigh the concerns all other voters have about the future.

What follows is a review of a few international examples of countries and territories that have proven effective at controlling spending.

Hong Kong

While the Hong Kong government has many troublesome aspects, including its lack of democracy, it might actually represent the gold standard of good fiscal policy. In a 2014 speech at the Heritage Foundation, Hong Kong’s Financial Secretary, Mr. John Tsang, explained, “Our commitment to small government demands strong fiscal discipline. . . . It is my responsibility to keep expenditure growth commensurate with growth in our GDP.” While that may sound like merely the empty campaign promise of a politician, in Hong Kong it’s actually a constitutional requirement: Article 107 requires that the government should strive to achieve a fiscal balance, avoid deficit, and more importantly, make sure government spending doesn’t grow faster than the growth of the economy.

When a country’s constitution actually requires such fiscal restraint, politicians go out of their way to anticipate the problems they might encounter in the future. For instance, Mr. Tsang added during his speech that he created a working group on long-term fiscal planning the year before, which he directed to conduct a fiscal sustainability health check because he and fellow officials were “keenly aware of Hong Kong’s low fertility rate and ageing population, not unlike many advanced economies. And that can pose challenges to public finance in the longer term.”

Hong Kong’s spending-to-GDP ratio has fluctuated between 14 and 20 percent since the 1990s, its debt as a share of GDP is zero, social welfare spending remains steady at less than 3 percent of GDP, and the share of the population relying on social security assistance has gone down from 4.1 percent in 2007 to 3.1 percent in 2017.

Switzerland

The Swiss are broadly recognized for the comparative excellence of their fiscal rules. After public referenda in 2001, the Swiss government in 2003 implemented a new constitutional fiscal expenditure rule aimed at ensuring a structurally balanced annual budget through a cyclically adjusted expenditure ceiling. The short story is that Swiss politicians are not allowed to increase spending faster than average revenue growth over a multiyear period (as calculated by the Swiss Federal Department of Finance), which confines spending growth to a rate no higher than the rate of inflation plus population growth.

The Swiss debt brake rule is significant in that it appeals to economists and policymakers on both sides of the aisle. Advocates for fiscal restraint support this rule because it is effectively a spending cap, while social democrats support the rule as it allows for deficit spending during recessionary periods.

Key to this design is the fact that it is very difficult for politicians to increase the spending cap by raising taxes. As economist Dan Mitchell of the Center for Freedom and Prosperity explained in the Wall Street Journal, “Maximum rates for most national taxes in Switzerland are constitutionally set (such as 11.5% for the income tax, 8% for the value-added tax and 8.5% for the corporate tax). The rates can only be changed by a double-majority referendum, which means a majority of voters in a majority of cantons would have to agree.”

The United States’ current federal budget process focuses too little on the long-term implications of budget decisions; from public debate over spending and taxes to the president’s annual budget, policymakers remain largely shortsighted. The Swiss rule focuses attention on long-term budget trends while maintaining the positive aspect of fiscal discretion, such as the ability to quickly respond to unanticipated developments. This rule appeals to more interventionist economists and policymakers who favor deficit spending when revenues plummet during economic downturns.

There’s no arguing with the results: Annual spending growth fell from an average of 4.3 percent to 2.5 percent since the rule was implemented. Also, in 10 out of the past 14 years, Switzerland has had budget surpluses, while deficits have remained rare and small, averaging −0.85 percent during this period. At the same time, the Swiss debt-to-GDP ratio has fallen from almost 60 percent in 2003 to around 42 percent in 2017 (see figure 1). Switzerland now finds itself in an unusual situation whereby its policymakers frequently debate what to do with all of their additional surplus revenue—a circumstance that seems a million miles away from fiscal conditions in the United States.

In 2010, Germany adopted a rule that is quite similar to the Swiss debt brake. The two rules parallel each other in that each follows the small government Keynesianism model that allows the government to spend in a recession, but actually cuts back spending in good times to create surpluses to be spent during recessions. While the German rule isn’t as strict as the Swiss one, Germany’s public debt has fallen from 81 percent of GDP in 2010 to 64 percent of GDP in 2017.

Denmark

In recent years, left-leaning American politicians have put Denmark on the map as a model welfare state. However, since the 1970s Denmark has undertaken large-scale reforms to address the massive fiscal issues brought on by its very generous welfare programs. Among other reforms, Denmark has lowered its top income tax rate from 73 percent to 63 percent, lowered the corporate tax rate from 50 percent to 22 percent, abolished the wealth tax, shortened the length of time people that may receive government-supplied unemployment benefits from indefinitely to two years, and raised the retirement age.

The Danish government also implemented some interesting budget process reforms for a more systematic control of spending. In 2014 Denmark implemented The Budget Act to ensure more efficient management of public expenditures. The act is aimed at ensuring a balance or surplus on the general government balance sheet, as well as appropriate expenditure management at all levels of government.

In practice, the rule sets a limit of 0.5 percent of GDP on the structural budget deficit. Policymakers decided that managing fiscal policy on the basis of a balanced structural budget would lead to an appropriate fiscal position in the long term. They also designed the system to take discretion out of their own hands by making the cuts automatic. In addition to structural deficit rules, the Budget Act introduces four-year rolling expenditure ceilings. These ceilings set legally binding limits for spending at all levels of government and for each program. If one program spends under its cap, any money not spent cannot be reallocated to another program.

The Danish Economic Council assesses (annually) whether economic policy adheres to the target of the structural public balance and whether the proposed expenditure ceilings are consistent with medium-term projections for public finances.

According to data from the Organisation for Economic Co-operation and Development (OECD), Denmark ran a budget surplus of 1.1 percent in 2017, while the latest data from the International Monetary Fund (IMF) show that Denmark’s fiscal position has improved significantly in the first three years after implementing the Budget Act: general government gross debt as a percentage of GDP fell from 44 percent in 2014 to 35 percent in 2017 (see figure 2).

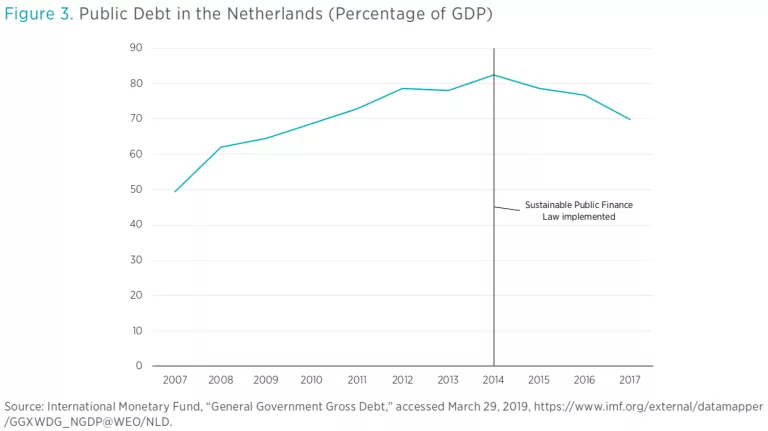

Netherlands

The Netherlands has a lot going for it despite being such a small country. The IMF, the OECD, and the European Commission have regularly highlighted the Dutch fiscal framework as an example of good practices that achieve a high degree of budgetary transparency. The framework has commendable features, such as medium-term orientation and the use of independent macroeconomic forecasts.

Under the Sustainable Public Finance Law of 2014, expenditure ceilings are set for three main budgetary areas (central government, social security, and health care), and benchmarks are set for revenues. While revenues are free to fluctuate over the cycle, the expenditure ceilings must be respected as statutory requirements.

The Dutch fiscal arrangement is special in that it combines both rules and institutions. The rule is based on a path for the budget ceiling, while the institutional apparatus rests on an explicit agreement among coalition parties before they take office and is valid until the next election. The independent agency that oversees this budgetary process is the highly respected Netherlands Bureau of Economic Analysis, which is responsible for producing budget forecasts and evaluating debt sustainability.

One weakness with the Dutch fiscal rule is that it fails to prevent wild fluctuations in expenditures over the business cycle. For example, the deficit ballooned beyond 3 percent from 2009 to 2013. However, compared to other fiscal frameworks, the Netherlands has seen noticeably improved fiscal conditions since 2014. In 2017, the government ran a budget surplus of 1.22 percent, compared to a deficit of −2.15 percent in 2014. According to the IMF, general government gross debt as a percentage of GDP has fallen over the same three-year period from 70 to 57 (see figure 3).

Fiscal outcomes in countries with despotic or monarchic institutions, which reflect the interests and desires of rulers, are different from those in countries with democratic institutions. Outcomes in democratic countries are the result of interactions among competing interest groups. One should also view these broadly successful international examples in light of the institutional budgetary setting in the United States. Richard Wagner has written extensively on the subject of federal budgeting as it relates to democratic governance in the United States. Policymakers often talk about fixing the budgetary system, but Wagner argues that they should instead be discussing restoring its founding constitutional framework of sound finance and limited government. While restoring a constitutional budgetary framework might be challenging, legally binding fiscal rules with strong reputational mechanisms would represent a strong commitment towards sound finance and limited government.

Conclusion

Governments around the world and across the ideological spectrum have implemented prudent budget rules or policies. All rules that are effective share some common features. The most successful rules place limits on the growth of spending or debt (as opposed to a balanced-budget constitutional rule favored by James Buchanan and some other economists). Rules that tend to have the greatest rate of compliance also set automatic triggers to reduce politicians’ discretion and restrain excessive government expenditure.

Delegating oversight of fiscal rules to an independent agency is a common feature in countries that have adopted broadly successful spending limits. Such oversight means that the budgetary process is more likely to enhance fiscal discipline if a broad mandate allows the agency to address various deficit biases, help identify bad policy deviations, and hold policymakers accountable.

The debt problem is rooted fundamentally in factors related to democratic governance. This is particularly the case in the United States, where the application of fiscal rules would face several key challenges. One challenge would be ensuring that the design of an independent fiscal agency does not contradict the power of the purse vested in Congress under the appropriations Clause and the taxing and spending clause of the US Constitution. Elected officials must shift their primary concerns away from short-term political and economic outcomes and instead consider the long-term fiscal implications of inaction.

Both the academic literature and analysis of international fiscal rules demonstrate that no set of fiscal rules will make much of a difference to the budgetary cycle if it is limited to the short term (a single year), if enforcement is weak, and if potential future impacts are ignored during the budget process. Applying these changes in budgeting practices is a matter of finding the fine line between tight and soft fiscal rules and minimizing the deficit bias of policymakers.