- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

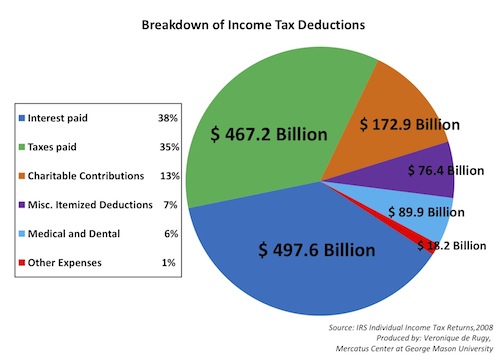

Breakdown of Income Tax Deductions

Mercatus Center Senior Research Fellow Veronique de Rugy characterizes the deductions claimed on the individual income tax in 2008.

Federal tax code allows taxpayers to deduct certain expenses from their taxable income, thereby lowering taxpayers’ overall level of tax liability. This week, Mercatus Center Senior Research Fellow Veronique de Rugy characterizes these income tax deductions claimed in 2008. By magnitude, the top three categories of deductions claimed were on interest paid, taxes paid, and on charitable contributions.

The many tax deductions endemic to our tax system have recently been identified as potential targets for deficit reduction. Setting aside the issue of whether this foregone revenue constitutes a spending issue or not, the fact remains that income tax deductions are yet another component of a riddled and biased tax system. Tax reform that moves us toward a broader based, lower rate tax system is needed to help address our debt and deficit issues.

The largest category of deductions, deducted interest payments, accounted for $497.6 billion in foregone revenue in 2008. This category of deductions contains the largest single income tax deduction - $470.4 billion in reduced income taxes due to reimbursed home mortgage interest payments. The remaining 5.5% of tax deductions in this category were from investment expenses and qualified mortgage insurance premiums.

Deductions in the second largest category, noted above as “taxes paid”, account for $467.2 billion in foregone income tax revenue. 62% of these deductions were state and local income and sales taxes paid, 36% of these deductions were due to real estate taxes, and the remaining 2% of deductions in this category were due to personal property taxes and other taxes paid.

Eligible charitable contributions, medical and dental expenses, and other smaller expenses comprise the remaining deductions.

Veronique de Rugy blogs the mortgage-interest deduction at The Corner.