- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

Can We Grow Our Way Out of Debt?

The United States has both a debt and deficit problem, driven by years of overspending and unfunded promises made by politicians of both parties to pay for health care and retirement benefits to current and future seniors. The solution to the problem is relatively straightforward (although far from simple) and involves cutting spending; in particular, reforming programs like Social Security, Medicare, Medicaid, and the Affordable Care Act.

The United States has both a debt and deficit problem, driven by years of overspending and unfunded promises made by politicians of both parties to pay for health care and retirement benefits to current and future seniors. The solution to the problem is relatively straightforward (although far from simple) and involves cutting spending; in particular, reforming programs like Social Security, Medicare, Medicaid, and the Affordable Care Act.

Recent commentary from Lawrence Summers, Ezra Klein, E. J. Dionne, and others, however, suggests that Washington’s focus on debt and deficit is misplaced because modest increases in economic growth can resolve the current fiscal dilemma. But economic growth alone cannot rescue the United States from the consequences of fiscal profligacy.

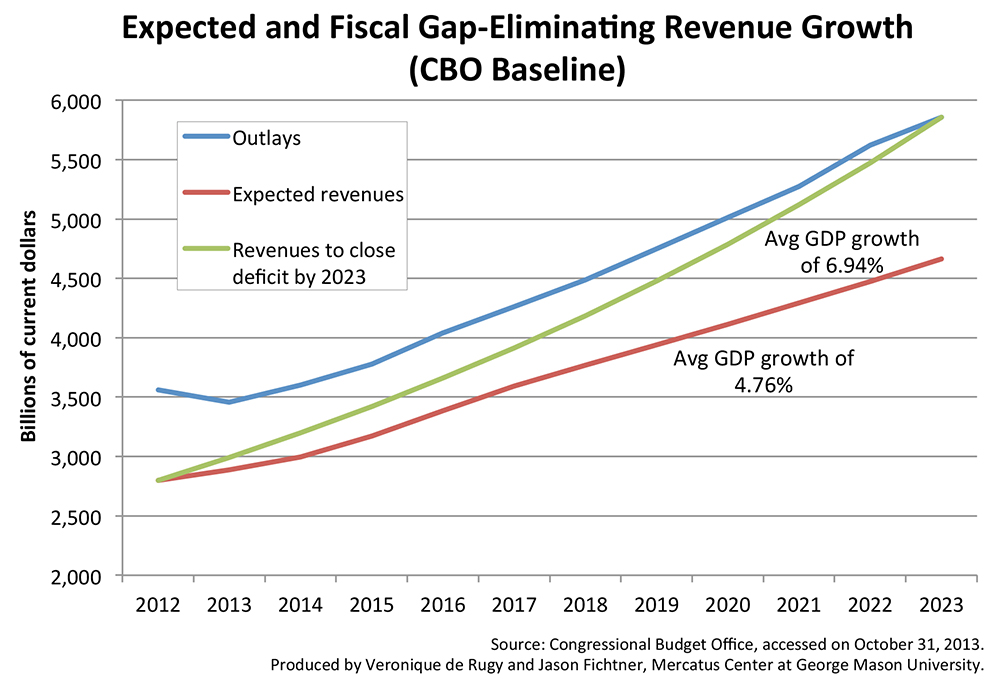

This week’s charts use data from the Congressional Budget Office to highlight the US fiscal position over the next ten years. These charts display projected outlays and revenues under the CBO baseline scenario and alternative baseline scenario, along with the revenues needed to eliminate the fiscal gap over the next decade and the average GDP growth rates needed to generate each revenue line.

The first chart displays outlays and revenues under the CBO baseline scenario. The CBO’s projected outlays are plotted along with expected revenues, which are calculated as the historical average of 18 percent of projected GDP. Keeping in mind that GDP projections are typically optimistic, the chart shows that the United States will maintain a considerable fiscal gap over the next ten years, even with a projected nominal average growth rate of 4.76 percent.

To close the fiscal gap solely through increased revenues from increased economic growth by 2023, the US economy will have to grow by 6.94 percent per year. This is considerably higher than the simple average growth rate of 3.9 percent a year from 2002 to 2012 that the US economy actually achieved, reaching a maximum of 6.7 percent in 2005 and plunging to a minimum of negative 2.1 percent during the depths of the recession in 2009.

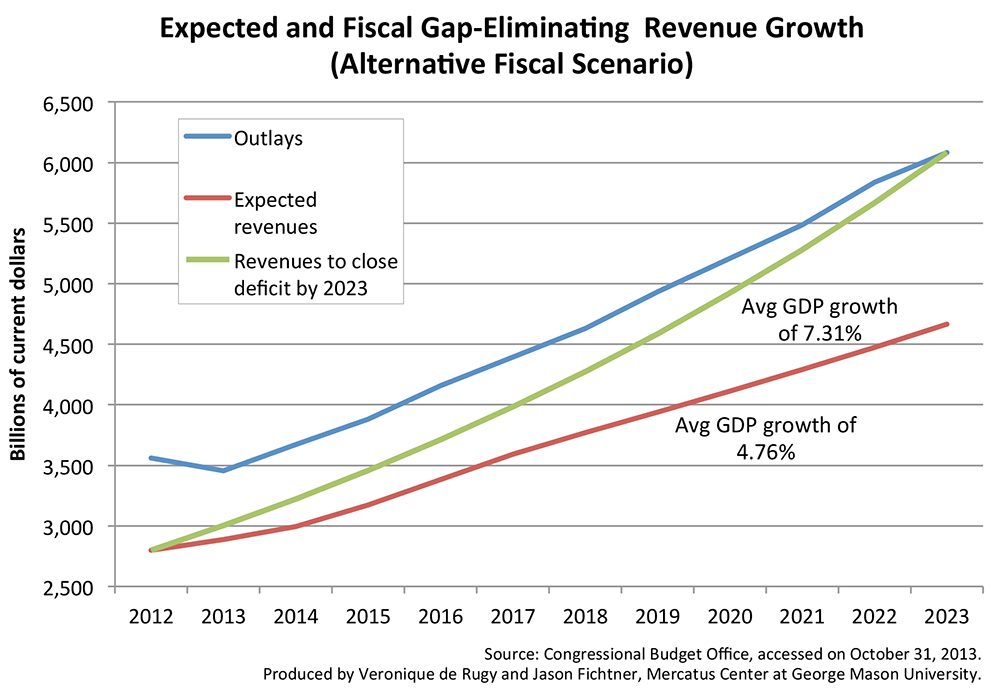

The second chart, which displays the same information under the CBO’s alternative fiscal scenario, is even direr. Under these assumptions, the US economy would need to grow by 7.31 percent nominally each year to generate enough revenues to close the fiscal gap by 2023.

If the CBO’s projections are accurate, the US economy will need to exhibit unprecedented sustained nominal growth rates of 6.9 to 7.3 percent per year to eliminate our 10-year fiscal hole without fundamental entitlement and tax reform.

There is little reason to expect that the US economy will depart from recent historical trends and begin to grow at miracle rates of seven percent a year. Many of the policies that contribute to the debt and deficit will also hinder economic growth. Policymakers in the United States need to get serious about entitlement and tax reform, instead of just waiting for a miracle to rescue them from their fiscal woes.

Related Content

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

Spending Cuts vs. Revenue Growth: How Best to Eliminate the Fiscal Gap?

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

How Does the US Debt Position Compare with Other Countries?

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

Who Owns the US Debt Held by the Public?

- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

Thirty-Two Years of Bipartisan Debt-Ceiling Raises