- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

CBO: Export-Import Bank, FHA Mortgage Guarantees, and DoED Student Loan Programs Yield Losses, Not Profits

This week’s charts use data from this CBO report to display the discrepancies between the two accounting methods in each bodies’ reported costs. The charts show that these programs are in a far more dire fiscal position than their administrators have reported to the public.

What do the Export-Import Bank (Ex-Im), the Federal Housing Administration (FHA), and the Department of Education (DoED) have in common? A recent Congressional Budget Office (CBO) report suggests that these federal bodies share more than criticisms that their respective interventions have inflated bubbles in aircraft, housing, and student loan prices. The CBO finds that these programs are actually deep in the red, contrary to their administrators’ claims of profits in recent years.

Released in May of 2014, the report estimates the expected budgetary costs of the DoED’s four largest student loan programs, Ex-Im’s six largest export credit programs, and the FHA’s single-family mortgage guarantee program using CBO’s “fair value” accounting method for FY 2015 to FY 2024. The report then compares these calculated costs to those reported by Ex-Im, the FHA, and the DoED. These federal bodies employ an unusual accounting method first prescribed by the Federal Credit Reform Act of 1990 (FCRA). The CBO found that the FCRA budget cost estimates were considerably rosier than the costs calculated by its fair-value method. Rather than saving taxpayers billions of dollars, as program administrators claimed, the CBO reports that these programs will actually cost taxpayers a combined total of roughly $120 billion over the next ten years.

This week’s charts use data from this CBO report to display the discrepancies between the two accounting methods in each bodies’ reported costs. The charts show that these programs are in a far more dire fiscal position than their administrators have reported to the public.

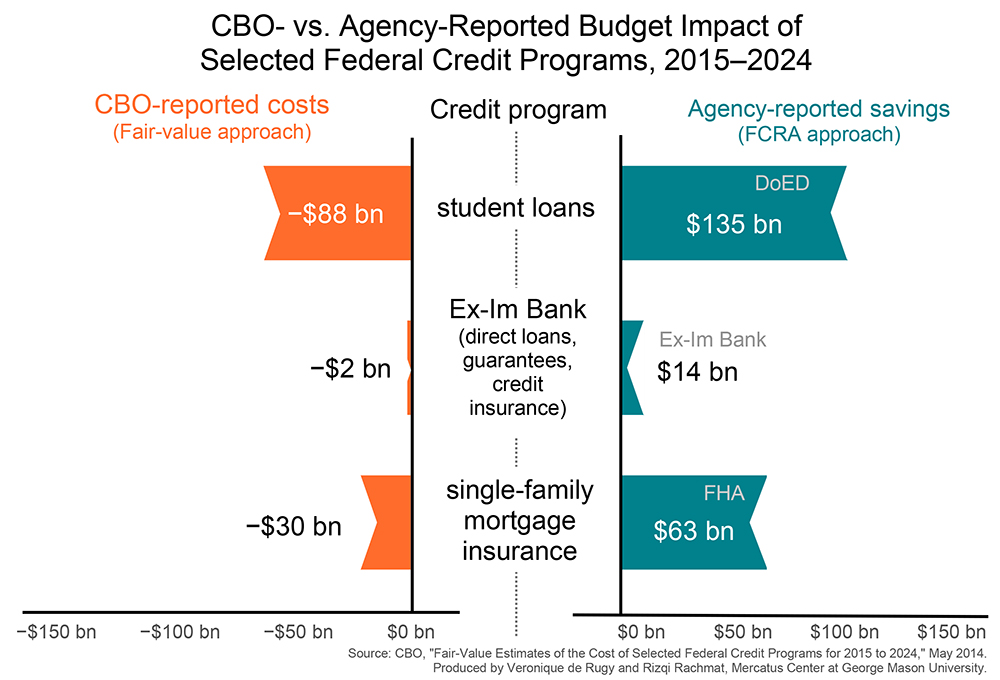

The first chart compares the total budgetary impacts projected through the FCRA accounting method to the projected budgetary impact estimated through the CBO’s fair-value method. Each agency reported handsome profits using their own accounting methods: the DoED boasted of a -$135 billion subsidy cost (which translates to $135 billion in savings to taxpayers); Ex-Im projected $14 billion in taxpayer savings; and the FHA expected $63 billion in taxpayer savings over the next decade.

However, the CBO’s fair-value method paints a bleaker picture. According to the CBO, DoED student loan programs are projected to cost taxpayers $88 billion; Ex-Im direct loans, guarantees, and insurance policies stand to cost $2 billion in tax dollars; and the FHA’s single-family mortgage program is on track to cost taxpayers $30 billion by FY 2024. Rather than yielding handsome profits, the CBO’s calculations project that these programs will cost taxpayers dearly.

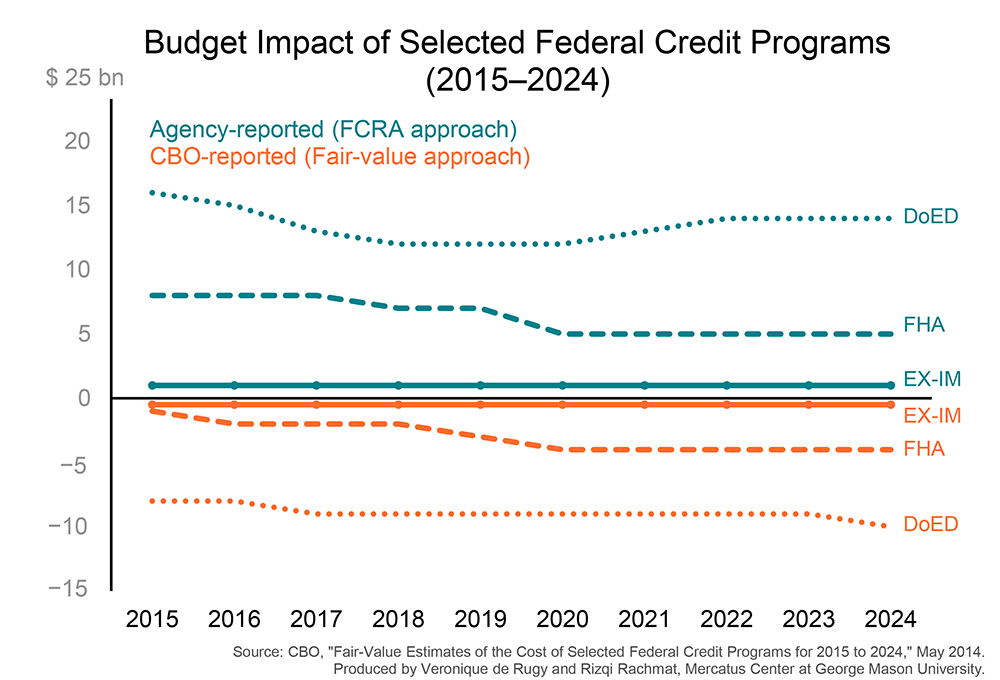

The second chart displays the annual projected budget impact of both accounting methods for each agency in a time series. The chart suggests that, barring rapid reform, the concealed budget impact of each program will impose substantial costs on taxpayers for years to come.

In order to understand the large discrepancies between the calculations yielded by each accounting method, we need to first understand a few basics of federal budgeting. While most federal spending is recorded in the budget on a cash-flow basis that logs inflows and outflows at the time that they occur, these federal credit programs employ a special accounting method that records the lifetime costs of the program up front on an accrual basis. This means that inflows and outflows are logged during the year in which the loan in made, rather than the specific date.

The present value of each program is calculated by expressing current and future inflows or outflows in terms of a single value equivalent to a lump sum that would be received or paid today. This value, in turn, depends on the rate of interest that translates future cash flows into current values.

The discrepancies between the calculations yielded through FCRA accounting and those from CBO’s fair-value accounting rest in the different interest rates that each method employs. The Ex-Im Bank’s FCRA calculates present value using US Treasury securities rates as a guide. The CBO’s fair-value approach, on the other hand, uses market interest rates to calculate the present value of expected future cash flows. A previous CBO report from May 2012 explains in detail how using market values can better account for the cost of the government’s risk.

Supporters of the Export-Import Bank have defended its programs in part because the programs were believed to “make $1 billion for taxpayers.” The Department of Education’s student loan programs have been characterized as “a profit-making machine” for the federal government. The Center for American Progress praised the Federal Housing Administration’s mortgage insurance program, gushing that “recent years are likely to be some of its most profitable ever, generating surpluses as these loans mature.” This recent CBO report debunks these myths of profit-making federal programs and provides a compelling reason for dramatically reforming these programs so as to reduce federal spending on them over the coming decade.