- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

Export-Import Bank Exposure Grows as Private Lenders Profit

The large numbers that spill across Ex-Im balance sheets concern all US taxpayers. Although names like JP Morgan and TD Bank are listed on these records, taxpayers are ultimately responsible for these liabilities. The US government should not exploit taxpayers’ credit to funnel risk-protected assets to large private corporations. It is past time to put this cash cow for cronies out to pasture.

The Export-Import Bank is one of the least defensible corporatist boondoggles that taxpayers are forced to subsidize. This US government-owned corporation styles itself as a self-sustaining independent executive agency that selflessly serves the public by “support[ing] jobs in the United States,” “facilitating the export of US goods and services,” “provid[ing] competitive export financing,” and “ensur[ing] a level playing field for US exports in the global marketplace.” In reality, the Ex-Im Bank is little more than a publicly subsidized piggy bank for large corporations, who retain private profits while transferring risk to taxpayers.

This week’s charts use data from the Export-Import Bank’s Annual Reports, public data on Export-Import FY 2012 Applications, to display Ex-Im activity from 2007 through 2013 and major private lenders for FY 2012. The data reveal an agency that funnels taxpayers’ dollars to prop up profits for some of the largest financial corporations in the United States and abroad.

The first chart displays the total amount of exposure, authorizations, and deals made using data from the Ex-Im Bank’s series of annual reports for the years 2007 through 2013. Measured on the left axis, the total amount of exposure—defined by the Ex-Im Bank as “authorized outstanding and undisbursed principal balance of loans, guarantees, and insurance” plus “unrecovered balances of payments made on claims . . . under the export guarantee and insurance programs”—has consistently grown over time. In layman’s terms, this is the amount of risk for which taxpayers are on the hook. Total Ex-Im Bank exposure grew from $57.42 billion in 2007 to $113.83 billion in 2013—never dropping once during this period. Meanwhile, total authorizations, or normal budget funding totals, while small in comparison to the high exposure levels sustained for the past seven years, still grew steadily from $12.37 billion in 2007 to $35.73 billion in 2012 before dropping slightly to $27.29 billion in 2013. Finally, the total number of deals that the Ex-Im Bank makes each year is represented by the gray line and measured on the right axis. Since 2009, far more private corporations have gotten in on the corporatist gravy train. The total number of Ex-Im Bank deals made expanded from a relatively modest 2,951 deals in 2009 to 4,061 deals in 2013.

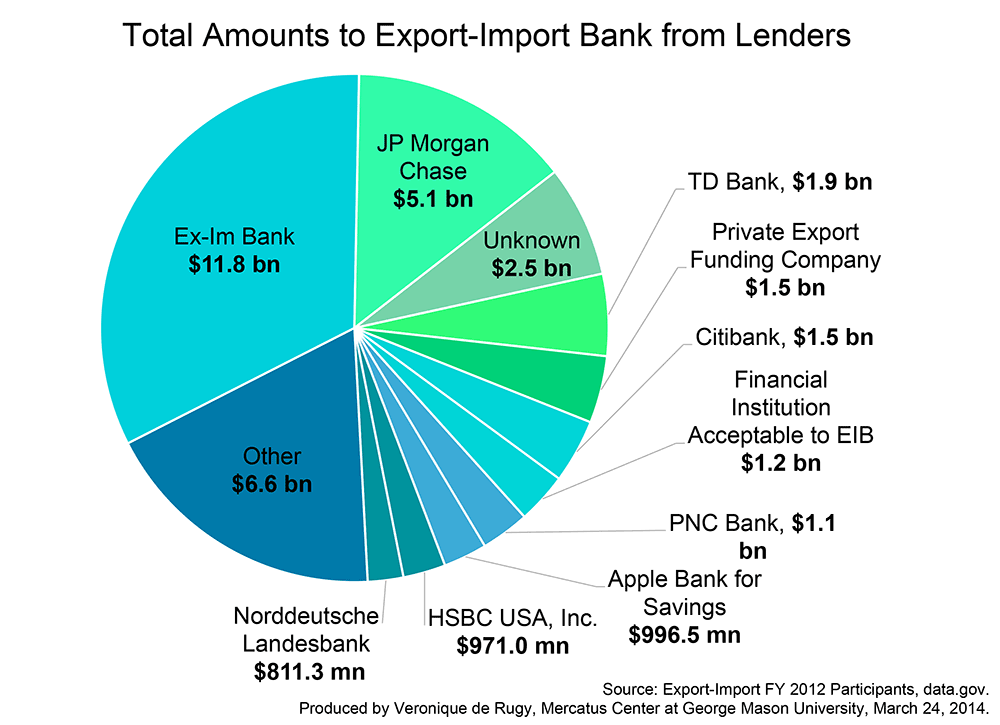

The second chart displays internal Ex-Im Bank data on private lenders that participate—and profit from—Ex-Im projects. As the vast discrepancy between total exposure and total authorization hints, the Ex-Im Bank does not fund or underwrite all of its schemes by itself. According to their website, the Ex-Im Bank “guarantees to lender[s] that, in the event of a payment default by the borrower, it will pay to the lender the outstanding principal and interest on the loan.” We sorted these lenders by instrument amounts and displayed the top 10 heavy hitters for FY 2012, along with a consolidated group of all other lending amounts.

As the second chart shows, the top corporate beneficiaries of Ex-Im Bank activities include some of the usual suspects—JP Morgan Chase, TD Bank, Citibank, and Wells Fargo—familiar to Americans as recipients of the generous taxpayer-funded bailout packages during the 2008 financial crisis. Foreign banks like Norddeutsche Landesbank also figure in the list, along with the Ex-Im Bank itself. Curiously, and somewhat distressingly, the Ex-Im Bank’s own internal records lists its third-largest lender only as “Unknown.” Another top contender, “Institution Acceptable to EIB [Ex-Im Bank],” is similarly scant on relevant details. This placeholder is included in Ex-Im Reports going back to 2007 and likely refers to loans that were still being shopped around for private partners while the report was being written. While it is very probable that many of these loans were assigned to power players like JP Morgan and TD Bank, the failure to retroactively update these private records with the final details means that taxpayers have no way to know where the funds ultimately went.

The Ex-Im Bank likes to boast about supporting small business, boosting exports, and financing promising projects, but a quick look at their biggest beneficiaries suggests that the Bank is little more than a slush fund for special interests; there is a reason that its nickname is “Boeing’s Bank.” What’s more, the GAO has been sounding the alarm about the Ex-Im Bank’s suspicious underwriting practices and massive expansion for years.

The large numbers that spill across Ex-Im balance sheets concern all US taxpayers. Although names like JP Morgan and TD Bank are listed on these records, taxpayers are ultimately responsible for these liabilities. The US government should not exploit taxpayers’ credit to funnel risk-protected assets to large private corporations. It is past time to put this cash cow for cronies out to pasture.