- | Government Spending Government Spending

- | Federal Testimonies Federal Testimonies

- |

Regulation, Growth, and Labor Market Recovery

Testimony before the House Committee on the Judiciary

The biggest problem with the US labor is a lack of economic growth. And according to our biggest job creators, small business owners, government is playing a big role in holding back the economy.

Chairman Goodlatte, Ranking Member Conyers, Subcommittee Chairman Bachus, Subcommittee Ranking Member Cohen, and members of the committee, thank you for the chance to discuss regulation and the current state of the US labor market. I appreciate the opportunity to testify today.

INTRODUCTION

It has now been a full four years since the end of the Great Recession. Unfortunately, the US labor market is far from recovery. At the end of the recession, just 59.4 percent of working age Americans had employment. Today that number is even lower, at 58.7 percent. Over 100 million people are now jobless and there are about four and a half million long-term unemployed. There are likely millions more long-term jobless that are not being counted. We are looking at a decade before the labor market is close to fully recovered. Many of the long-term jobless will never fully recover their lost earnings. Our primary focus should be on encouraging the economic growth that we need to push our labor market into full recovery mode.

The biggest problem with the US labor is a lack of economic growth. And according to our biggest job creators, small business owners, government is playing a big role in holding back the economy. Remarkably, surveys of small business owners show they are more worried about government than the weak economy. For example, according to the Gallup/Wells Fargo Small Business Index, a third of respondents reported that their most important challenge is government regulation, taxes, healthcare/Obamacare, or just government generally—more than are concerned about attracting new customers or the economy generally.[1] According to the National Federation of Independent Business, nearly half of all small business owners cite either taxes or government regulation as their biggest single problem.[2] According to both surveys, only six percent of owners are primarily worried the quality of their employees.

So the answer to our labor market problems right now is doing what we can to eliminate the tremendous amount of uncertainty over economic policy that is holding back consumers and the economy. One important thing that we need to realize is that regulation has a cost. Poorly designed regulation can cause significant economic distortions that affect labor markets. Even a well-designed regulation where there are significant benefits has an economic cost that needs to be considered. For example, any regulation that raises the cost of production for an industry lowers productivity and likely creates unemployment. Unemployment any time is costly for those involved, but in a bad labor market like today’s it can be devastating. At this time we should also be particularly concerned with who bears the unemployment burden of regulatory changes. Youth and older workers have been particularly hard hit by the recession and weak recovery. Youth have a higher unemployment rate and are overrepresented in the long-term unemployed, while it takes on average over 30 weeks for someone over 55 years old to find new work. The disparate impact of the recession on demographic groups is a matter of concern.

THE EMPLOYMENT COST OF REGULATION

Regulation has a cost. Economic studies have made it clear that ill-designed regulation can cause significant economic distortions that damage investment and entrepreneurship, reduce competition, lower productivity and economic growth, and raise unemployment. Even well-designed regulation that addresses a significant market failure, such as the existence of externalities, incomplete markets, information asymmetries, or public goods, has a cost. This fundamental economic principal has been acknowledged in presidential executive orders for decades now. In particular, Executive Order 12866 in 1993 and Order 13563 in 2011 direct US regulatory agencies to follow some basic principles that include:

- Identify the problem that a regulation intends to address (e.g., identify the market failure) and state regulatory objectives

- Propose or adopt a regulation only upon a reasoned determination that its benefits justify its costs

- Tailor regulations to impose the least burden on society, consistent with regulatory objectives

- Maximize net benefits (benefits minus costs), taking into account distributive impacts and equity

An important part of the cost of regulation is its effect on labor markets. Both of the above referenced executive orders explicitly mention employment effects. Most recently, the Office of Management and Budget made this very clear when they stated that “job creation is an important consideration in regulatory review” in their Draft 2013 Report to Congress on the Benefits and Costs of Federal Regulations and Unfunded Mandates on State, Local, and Tribal Entities.[3]

The employment impact of a regulatory change that raises the cost of production in an industry is basic economics. Higher production costs from a regulatory change lower productivity in the regulated industry. This raises market prices, and the higher prices lower demand. Lower production means lower demand for labor, and production workers become unemployed. Production is lowered by more if substitute products exist, particularly if they are imported goods and services. If additional labor is hired as a result of compliance efforts, this raises the economic cost of the regulation as labor is pulled from other uses in the economy. There is no reason to believe that any of the production workers in the industry that become unemployed will be rehired into compliance occupations. In summary, within the regulated industry:

- Productivity is reduced as more resources are used to produce less output. Some of these resources may be labor resources.

- Industry prices rise and production is lowered in the industry.

- Unemployment is created as employment of production workers declines.

In addition to the direct effects in the regulated industry, there will be indirect effects on other industries and on consumers. If the regulated product is purchased by other industries, then their costs rise, prices will rise, demand for their products will fall, and there will be an increase in unemployment. If consumers purchase the regulated product, then their buying power declines and there will be a loss of employment as consumers buy less. Although the price increases can be small in percentage terms, the potential employment effect can be quite large. For example, the EPA estimated that a proposed Toxics Rule would raise electricity prices by nearly four percent, and this would raise costs of production in at least 19 downstream industries. Though the reduction in consumption could be very small in percentage terms in most industries, the employment in those industries is so high that the job loss could be significant. In fact, by my calculation, for every one production job lost in the electrical generation industry by this regulatory change, an additional eleven workers in other industries could become unemployed. Several points about the employment cost of regulation are worth making:

- Unemployment is created. The economic cost of that unemployment is not trivial, especially with a bad labor market.

- While there may be increased demand for occupations needed in compliance, this is not a benefit to the economy but part of the cost, as these resources are unavailable for producing other goods and services.

- Compliance hiring comes at the expense of production workers in other occupations. There is therefore a redistributive effect of regulation that places a burden on particular workers in particular occupations.

- There may be long-run impacts of regulation on overall economic growth, job growth, and even the long-run unemployment rate. Economic studies comparing countries with different regulation levels make this clear. Because these macroeconomic and dynamic effects are impossible to project for individual regulatory changes, we run the risk of a “death by a thousand cuts” if we do not at least occasionally look at regulation levels and try to assess their cumulative effects.

THE COST OF UNEMPLOYMENT

For years now there has been a significant amount of economic evidence that unemployment is very costly and results in significant and sustained earnings losses for individuals. The immediate impact of job loss includes lost wages, job search costs, and retraining costs (sometimes with taxpayer assistance). Even after being reemployed, the permanent lost earnings for the jobless will likely be significant. Studies have shown that it can take as long as 20 years for reemployed workers to catch up on lost earnings, largely due to skill mismatches between the jobs lost and the new jobs created in the economy. These losses occur for workers with different lengths of previous job tenure, in all major industries, and for workers of any age. One recent estimate using data between 1974 and 2008 found that permanent earning losses range from 1.4 years of earnings in good times to 2.8 years during times of high unemployment.[4] I anticipate that the poor performance of the labor market since 2008 will lead to an even greater earnings loss for the currently unemployed. Even beyond these direct effects, there is evidence of future job instability, increased earnings volatility, and a reduction in life expectancy for unemployed workers. There are even negative impacts on family outcomes such as the educational and future labor market performance of children and bad spillover effects on communities that experience significant unemployment.

Despite this clear evidence of the horrible effects of unemployment on US workers, it is routine practice for regulatory agencies to estimate the benefits and costs of regulatory changes under what economists generally refer to as the “full employment” assumption. This is literally the view that there is no unemployment either before or after a regulatory change. In other words, this is the assumption that any individuals that become unemployed are instantly and costlessly reemployed in nearly identical jobs. This, of course, results in a systematic and significant underestimation of the cost of regulatory changes.

CURRENT STATE OF THE US LABOR MARKET

It has now been four years since the end of the Great Recession. However, these four years have not been kind to millions of American workers. In the immediate aftermath of the recession, just 59.4 percent of us had employment. Now, that number is even lower—58.7 percent. Over 100 million people are now jobless. At 200,000 jobs per month, the labor market is growing but leaving millions of long-term jobless behind. At this rate, it could take a decade for the labor market to fully recover. Our biggest economic concern should be encouraging enough economic growth to push the labor market into a full recovery.

Joblessness is costly, particularly for high-tenure workers who have invested time and resources in job-specific knowledge and skills. Studies consistently show that the longer someone is unemployed, the less likely they are to find new work. They may have lost job skills over time, have less connection with informal job networks, and may face potential employers more reluctant to hire the long-term jobless. And because those with job skills in shortest supply will be reemployed first, the ranks of the long-term jobless may accumulate those that worked in permanently declining industries and those that have job skills that don’t translate well to new employers or industries.

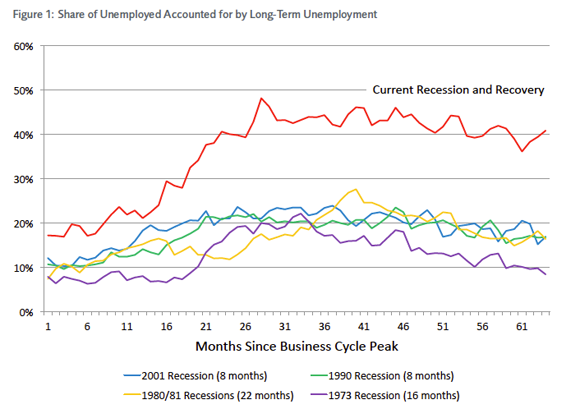

There are currently about 4.5 million long-term unemployed in the United States. Two-thirds of these people have been jobless for over a year and might be classified as “very long-term unemployed.” Large as these numbers are, they dramatically underestimate the long-term jobless problem. Millions of people, after struggling unsuccessfully to find work, have stopped looking altogether. This disengagement from the labor force has driven down the unemployment rate without reducing joblessness. To be counted as “long-term unemployed” (as opposed to “long-term jobless”), an individual needs to have no work whatsoever for six months, be nearly instantly available if offered work, and be actively looking for work. By actively looking, he or she must send out a resume, interview for a job, engage an employment agency, or engage in some other sort of activity that, by itself, could result in employment. Checking for new job openings on the Internet or in the newspaper alone does not qualify as active job search.

This sets a high bar for someone to remain unemployed for long enough to be considered long-term unemployed. In 2007, the average unemployed person who eventually exited the labor force looked unsuccessfully for work for just under 9 weeks. In 2011, this had risen to over 21 weeks. That means the average person that left the labor force did so before being even classified as long-term unemployed and almost certainly could eventually be called long-term jobless. Millions of people have dropped from the labor force over the past five years who perhaps should still be counted as long-term unemployed.

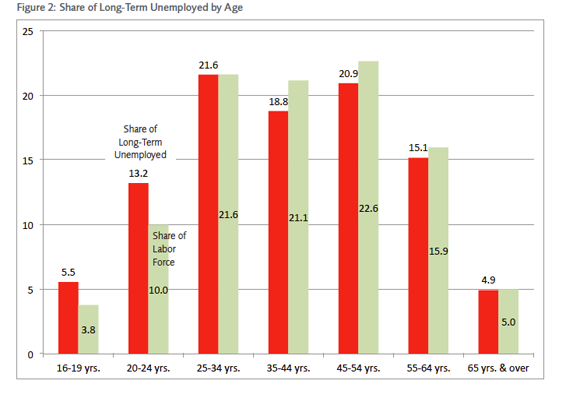

The impact of long-term joblessness has not been even. Youth have been particularly hard hit by the recession and slow recovery. They are less likely to be in the labor force, more likely to be unemployed, and despite their age, more likely to be long-term unemployed. Less than half (46 percent) have employment. Their unemployment rate, at 16.1 percent, is over twice the national average. Those age 20 to 24 years old make up 13.2 percent of the long-term unemployed but just 10.0 percent of the labor force. This problem of high youth unemployment is not necessarily an indication of anything lacking in education or skills. In a sense, youth are taking a double hit from this recession. First, when employers cut jobs, they do what they can to let attrition reduce employment levels and don’t generally layoff more than they need to. This leaves fewer open positions for new graduates attempting to enter the labor force. As a result, youth unemployment rises by more than for older cohorts. Second, experienced workers have been much less likely to be able to shift jobs as they normally do to advance in their careers. Older workers have even delayed retirement as their wealth has taken a big hit from the recession. This slowdown in advancement may continue to severely impact younger workers for years. According to the Bureau of Labor Statistics, two-thirds of new jobs are replacement jobs. This means that even when younger workers find jobs, many will likely remain behind in their careers and suffer from years or even decades of lower earnings growth as they have fewer opportunities for advancement.

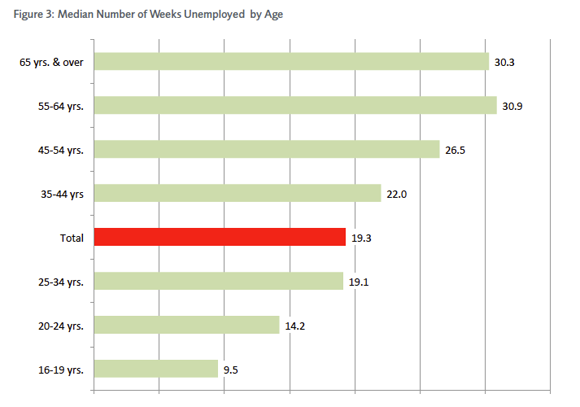

Older workers have also been particularly affected by the slow recovery. Not only have many had their retirement delayed because of lost wealth from the financial market collapse, but once an older worker becomes unemployed, he or she is more likely to remain unemployed. In fact, they are the only age group more likely to become long-term unemployed once losing a job. The median number of weeks unemployed nationally has surged since the start of the recession. It rose from 8.5 weeks in 2007 to well over 20 weeks—over double the previous record. It remained at 19.3 weeks last year. For workers over 55 years old, the median time unemployed is a remarkable 30 weeks.

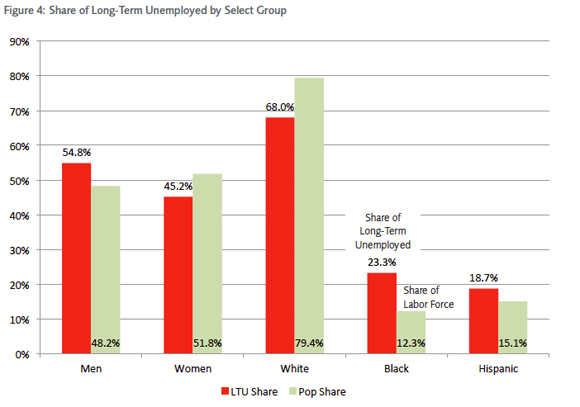

There are other groups that have also been particularly hard hit. The lower the educational attainment, the higher the unemployment rate and the lower the labor force participation. Today, only 39.6 percent of those without a high school degree have employment. African Americans are more likely to be unemployed and much more likely to be long-term unemployed. Their unemployment rate is 13.2 percent, well above the national average, and they represent 23.3 percent of the long-term unemployed but only 11.9 percent of the labor force. Similarly, Hispanics have a higher unemployment rate (9.0 percent) and represent 18.7 percent of the long-term unemployed but just 15.7 percent of the labor force.

Thank you for your time, and I look forward to your questions.

Footnotes

1. “Small Business Survey Topline,” Gallup, Wells Fargo, Quarter 2, 2013, https://wellsfargobusinessinsights.com/File/Index/y1o9AemryEuwEcD31jekgA.

2. “Small Business Economic Trends,” National Federation of Independent Businesses, June 2013, http://www.nfib.com/research-foundation/surveys/small-business-economic….

3. Office of Management and Budget, Draft 2013 Report to Congress on the Benefits and Costs of Federal Regulations and Unfunded Mandates on State, Local, and Tribal Entities (Washington, DC, April 2013), http://www.whitehouse.gov/sites/default/files/omb/inforeg/2013_cb/draft…;

4. Steven J. Davis and Till M. von Wachter, “Recessions and the Cost of Job Loss” (NBER Working Paper No. 17638, National Bureau of Economic Research, Cambridge, MA, 2011).