- | Housing Housing

- | Research Papers Research Papers

- |

Build More Houses

How an Incorrect Perception of Housing Supply Fueled the Great Recession and Slowed Recovery

Most debates about the causes of the Great Recession and the financial crisis accept the following premise: Too many homes had been built in the United States before 2007, and excessive construction was a fundamental cause of the resulting economic upheavals. Kevin Erdmann rejects this premise in his “Build More Houses: How an Incorrect Perception of Housing Supply Fueled the Great Recession and Slowed Recovery.”

Pre-Recession Housing Boom? What Housing Boom?

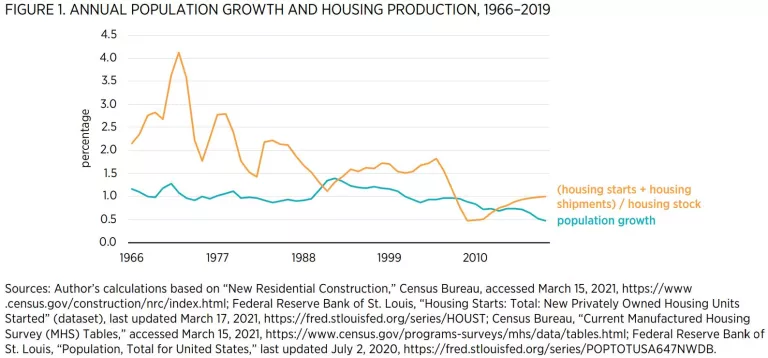

Despite the importance of housing supply as a purported cause of the Great Recession, the conventional view ignores some important data about pre-2007 housing supply. This has permitted unsupported assumptions about the causes of steeply declining construction activity and rising vacancies during the Great Recession.

- Basic historical comparisons (see figure 1) show that there just wasn’t a particularly large building boom during this period.

- At the national level, consumption of housing was either moderately rising or even declining relative to other income and consumption trends in the years leading up to the Great Recession.

- Excessively high prices were the result of severe local limits on housing supply.

- The Federal Reserve increasingly calibrated its monetary policy decisions to promote a level of economic activity that would coincide with an unprecedented decline in housing starts.

- Erdmann shows that the ensuing economic contraction interrupted long-standing migration and population patterns.

- The excessive housing vacancies that eventually burdened states such as Arizona and Florida were the result of severe declines in trend population growth rather than previous overbuilding.

What About Housing Now?

Fear of cyclical building, both before the Great Recession and after, has been misguided. Housing construction has been decreasingly cyclical for decades, following a pattern of moderation similar to GDP growth.

Some of the reduced cyclicality in housing construction is likely related to regulatory barriers that prevent construction from responding to demand for migration into what Erdmann refers to as Closed Access cities—those with low rates of building and very high costs. Given this constraint, systematic oversupply of housing was not a legitimate macroeconomic concern in 2007 and is unlikely to be one in the foreseeable future.

The best time to encourage more homebuilding would have been (surprisingly, in hindsight) 2007. The second-best time is now. The next best time is tomorrow.

Key Takeaway

Americans are right to be concerned that rents are rising and families aren’t able to find adequate housing. But they should not believe that a financial crisis was caused by building too many homes—this is not the case. Building more homes, just about everywhere, will produce broad economic benefits today