- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

Consumer Inflation Uncertainty Is Rising

The Federal Reserve (Fed) is in the middle of a cycle of interest rate hikes intended to bring extremely high inflation back toward its target. In recent months, Fed officials have repeatedly reiterated the importance of keeping the public’s inflation expectations anchored and have paid careful attention to the University of Michigan Surveys of Consumers (MSC) and the Federal Reserve Bank of New York Survey of Consumer Expectations (SCE). These surveys provide measures of what consumers expect about inflation in the next year and beyond.

In this policy brief, I first show that whereas shorter-run inflation expectations have risen substantially, the rise in longer-run inflation expectations has been much more modest. I suggest that the relatively small rise in longer-run expectations is not evidence that inflation expectations are firmly anchored. It is not just the level of consumer inflation expectations that matters, but also consumers’ uncertainty about future inflation. I provide evidence on consumer inflation uncertainty from the SCE and my own measure that I developed in a previous paper. Inflation uncertainty, even at longer horizons, is rising. I conclude by discussing the macroeconomic policy implications of this rise in long-run uncertainty.

Median Expectations at Shorter and Longer Horizons

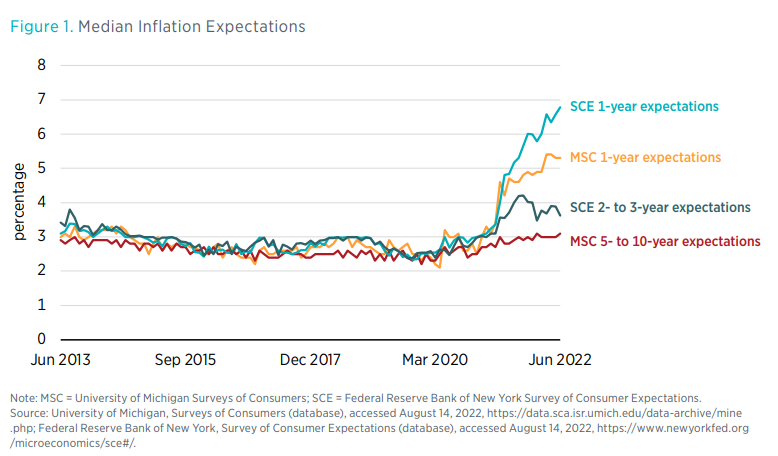

The headline numbers from the MSC and SCE data releases are usually the median inflation expectations. The median consumer’s one-year inflation forecast from both surveys has increased quite dramatically as inflation itself has risen—from less than 3 percent before the pandemic to well greater than 5 percent in 2022, as shown in figure 1.

But policymakers can take some solace in the fact that median long-run inflation expectations have remained much steadier. Figure 1 shows that the 2- to 3-year inflation expectation from the SCE peaked at 4.2 percent in October 2021 and fell to 3.6 percent in June 2022. June’s number is higher than typical prepandemic readings of just less than 3 percent, but it is much lower than the median one-year expectation. Likewise, from the MSC, the median 5- to 10-year inflation expectation rose only slightly, from around 2.5 percent before the pandemic to 3.1 percent in June 2022. These measures indicate that average consumers know inflation is high and they expect it to remain high for the next year, but they expect it to moderate afterward.

Inflation Uncertainty at Longer and Shorter Horizons

The relative stability of median longer-run inflation expectations is not, by itself, a clear sign that consumers’ inflation expectations are firmly anchored. It is important to consider how uncertain consumers feel about their inflation forecasts. One might expect consumers with well-anchored expectations not only to report a long-run inflation forecast that is near the Fed’s target, but also to have significant confidence in their forecast. If consumers report an inflation forecast of 2 percent, for example, but believe that there is a good chance that inflation could be much higher or much lower, then those consumers do not have a lot of confidence in a near-target outcome. Moreover, high uncertainty about longer-run inflation can make it very hard for households to make sound financial decisions.

Measuring inflation uncertainty is not entirely straightforward. The MSC, which has been conducted monthly since 1978, asks consumers for only their point forecast of inflation; it does not ask them how certain they are about their forecast. The SCE, introduced in 2013, gauges the level of respondents’ uncertainty. Specifically, the SCE asks for respondents “density forecasts” of inflation. That is, respondents assign probabilities to various ranges, or “bins,” of future inflation. These probabilities should add up to 100 percent. If respondents assign all probability to a single bin, one can infer that they are certain about the inflation outcome that they expect. By contrast, if respondents distribute probability across many bins, they are uncertain.

The researchers at the Federal Reserve Bank of New York who run the SCE use each respondent’s bin probabilities to estimate the parameters of a smooth distribution representing the respondents’ density forecast of future inflation. From those parameters, they compute the interquartile range of the respondents’ density forecast. The width of this interquartile range can be used as a proxy for the respondents’ inflation uncertainty.

An Alternative Measure of Inflation Uncertainty

In 2017, I wanted to find a way to measure inflation uncertainty using the MSC data, given that they are available for a much longer period than those of the SCE and given that the 5- to 10-year forecast horizons are of great interest to policymakers. I wanted this measure also to not rely on the assumptions the Federal Reserve Bank of New York needs to fit distributions to respondents’ bin forecasts. In creating such a measure, I discovered that respondents have a notable tendency to report round-number point forecasts for inflation—that is, multiples of 5 percent. This rounding tendency varies substantially over time. On the basis of the literature in psychology, cognition, and communication, I inferred that at least some respondents use round number forecasts to convey their high uncertainty about their responses.

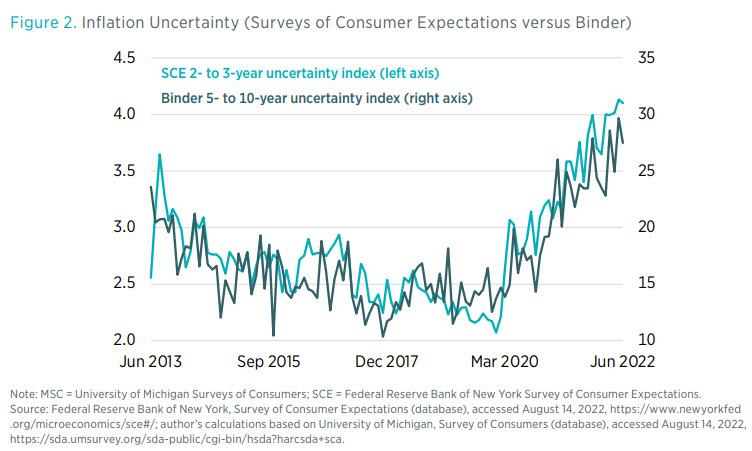

My 2017 paper provides the technical details of how I used that rounding behavior to construct inflation uncertainty indices for the 5- to 10-year forecast horizons and how I verified that the rounding behavior is a good proxy for uncertainty. In short, the indices capture the percentage of respondents who are likely to be highly uncertain about inflation, given their survey responses. A round number forecast alone is not enough to categorize a respondent as uncertain, but if a respondent provides a round forecast—say, 10 percent—in a month when very few respondents report expectations of neighboring nonround numbers (9 percent and 11 percent), then I assigned the respondent a high probability of being highly uncertain. In figure 2, I plot both the SCE 2- to 3-year inflation uncertainty measure, which corresponds to the median respondent’s forecast interquartile range, and the 5- to 10-year inflation uncertainty index using my methodology based on rounding behavior. The two series have a very strong positive correlation coefficient of 0.85.

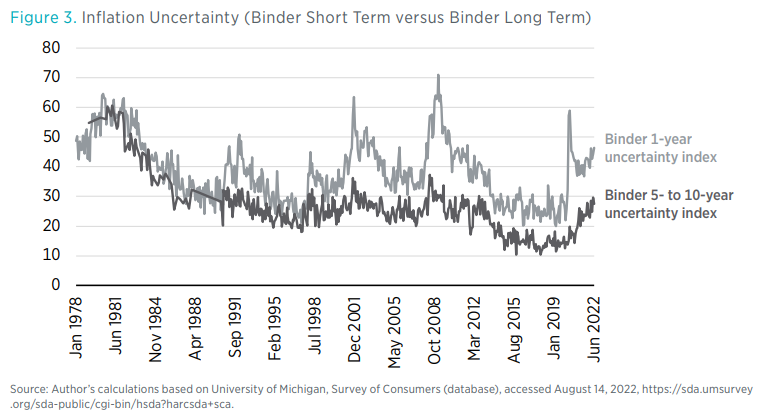

Both series show a marked rise in longer-run inflation uncertainty since 2020. Consumers have become much less certain about inflation developments in the coming years. About 30 percent of respondents are highly uncertain, according to my estimates. For the SCE, inflation uncertainty is at a series high. For the MSC, data availability allows me to consider inflation uncertainty in a longer historical perspective. Figure 3 shows both the shorter-run and the longer-run inflation uncertainty index since 1978. The figure shows that longer-run inflation uncertainty is still well-below shorter-run inflation uncertainty and well below its 1981 peak, when around 60 percent of respondents were highly uncertain. This is good news.

The bad news is that longer-run inflation uncertainty is back to roughly its 2009 level. All of the reduction in longer-run inflation uncertainty that occurred after the Federal Open Market Committee announced a formal 2 percent inflation target in 2012 has been wiped away.

Policy Implications

The data on consumer inflation expectations are mixed news for policymakers. Neither the level nor the uncertainty surrounding longer-run inflation expectations is nearly as high as in the early 1980s. This is a hopeful sign that the Fed can restore its credibility for promoting price stability. The less hopeful sign is that longer-run inflation uncertainty has been rising steadily, eroding more than a decade of progress. This uncertainty may be part of the reason that consumer confidence has plummeted.

Consumers will have trouble making major consumption, investment, and labor-market decisions if they do not know what to expect about the price level in several years. Uncertainty about inflation contributes to uncertainty about real interest rates, real wealth, and real income. These uncertainties lead to poor economic decision-making and mental stress. Congress gave the Fed a price stability mandate to help minimize these kinds of mostly avoidable uncertainties.

The Fed has claimed that it is committed to restoring price stability. I will continue to update and publicly share the inflation uncertainty indices in coming months and to hope that the longer-run index will begin to decline. I would consider a decline over several months to be a good signal of restored Fed credibility.