- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

The Danger in Using Monetary Policy to Address Housing Affordability

A Lesson from the Great Recession

One of the factors that played a role in the Great Recession was the excessive amount of debt-fueled consumption that led up to it. Lending terms were generous at the time, and home prices were far above historical norms. Homeowners were able to tap into that growing home equity. According to conventional wisdom, consumers who were spending borrowed money would have to pay that money back in the future. When home prices inevitably moved back to historical norms, not only would Americans have debt to pay off, but they would have fewer assets also. The bubble felt so good, but when the bubble eventually burst, Americans would be doubly poor because of their profligacy.

It seems like this is what came to pass. But in the book Shut Out and elsewhere, I have presented evidence that high home prices before the financial crisis were largely owing to a lack of supply. A lack of supply leads to rising rents. Credit markets may have facilitated rising prices, but prices were largely justified by the rising rental values in the most expensive cities: Boston, Los Angeles, New York, San Diego, and San Francisco. I call these the Closed Access cities.

This means that a collapse in prices was not inevitable. But more importantly, this means that calls for tighter monetary policy during the boom were calamitous. Loose monetary policy has been widely blamed for high home prices and for the debt-fueled consumption that they funded. Critics, and even Federal Reserve policymakers, generally agree that monetary policy should have been tightened sooner. But this is the wrong conclusion. In fact, monetary policy was powerless to counteract the debt-fueled consumption of the boom period, and the bust was only inevitable because the Fed tried to solve a problem that it could not functionally solve with tighter monetary policy.

Debt-Fueled Consumption

Atif Mian and Amir Sufi studied this issue and concluded, “The entire effect of housing wealth on spending is through borrowing, and, under certain assumptions, this spending represents 0.8% of GDP in 2004 and 1.3% of GDP in 2005 and 2006. Households that borrow and spend out of housing gains between 2002 and 2006 experience significantly lower income and spending growth after 2006.” They document how this spending comes mainly from credit- and income-constrained households, for whom home equity provided a temporary means for more current consumption.

An examination of the borrowers Mian and Sufi analyzed shows that the importance of rising rents and constrained supply as the source of rising prices would not change expectations of borrower behavior or its effect on current consumption. It should still be expected that the more credit- and income-constrained homeowners in cities with high prices would be the main borrowers.

Under the presumption that these homeowners’ capital gains were temporary, this borrowing and consuming activity was presumed to be destabilizing. This is where it is important to understand the correct source of high prices. Their newfound wealth wasn’t the result of a temporary credit bubble; it was the result of the persistent rise in the rental value of their homes. Their new consumption wasn’t destabilizing. It was stabilizing. They were economic rentiers. They were wealthier for it. And they were engaging in consumption smoothing. Since they were wealthier than they had been previously, their future expected levels of consumption also increased, so they were engaging in the common and normal process of shifting some of that future consumption into the present.

One refrain about the boom and bust has been that Americans turned out not to be as wealthy as they thought they had been, and the bust was simply a realization of that. But for homeowners in the Closed Access cities, the story is the opposite. It turned out that in 2005 they were wealthier than they thought they were. But where did that wealth come from? It came from the rental value and the expected future rental value of their homes.

The prices of their homes contained information about the future. Their future economic rents were capitalized into the value of those homes. Their wealth came from claiming future income from workers. Therefore, they were wealthier than they had thought. And everyone else—everyone who would be tenants in those homes in the future, everyone who would be willing to pay exorbitant rents in the future in order to gain access to lucrative urban jobs—would be poorer than they had thought they would be in the future.

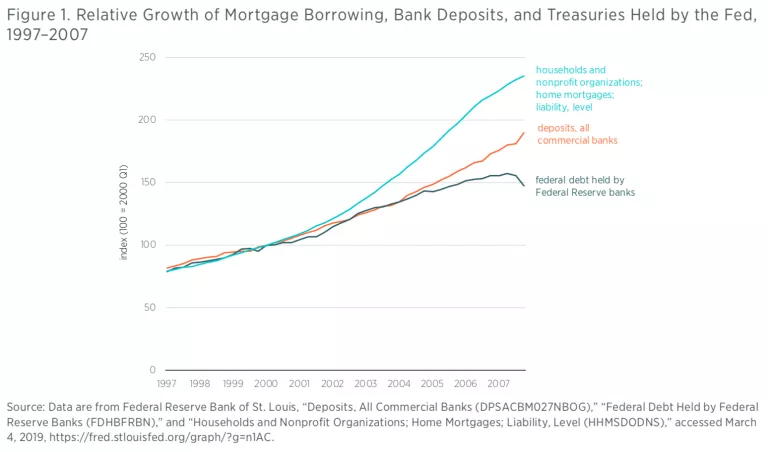

That rentier consumption smoothing would be inflationary, so an inflation-targeting central bank would react by tightening monetary policy. The fact that in 2004–2006 inflation did remain fairly close to target suggests that the Fed was, indeed, reacting with tighter monetary policy than it would have implemented otherwise. At the time that mortgage growth was high, bank deposits continued to grow at relatively normal rates, but the Fed’s asset base and currency growth slowed considerably. For all the criticism of Fed accommodation, it was not purchasing many Treasury bills during the boom, as shown in figure 1.

But note that while the consumption of these newly wealthy real estate owners was inflationary, there is little that monetary policy could have done to change that. In other words, they were using newfound wealth to claim an additional 1.3 percent of GDP for their own consumption, according to Mian and Sufi. That claim on current consumption would remain whether the Fed produced 10 percent inflation or 2 percent deflation. In fact, as the United States discovered in the end, the only way for monetary policy to affect that claim on current consumption would be to allow disruptions in capital markets to become so severe that these rentiers would not be able to access their wealth. The future rental value of their homes has not changed. That future rental value is a product of high demand for living in cities with restricted supply of housing. Monetary policy can’t fix that. It didn’t fix it. Rents in the Closed Access cities are at least as high as anyone might have expected them to be in 2005. The only thing the housing bust accomplished was to prevent the value of those future rents from being fully capitalized into home prices after 2007.

If, before the housing bust became catastrophic, monetary policy within a functional range could not change the ability of these rentiers to claim more current production, then what economic adjustments must happen to satisfy their new consumption demands? If these rentiers were claiming 1.3 percent of additional GDP, where was it going to come from? If they were increasing their current consumption but not their current production, the gap must be met somewhere. Either other Americans would have to reduce their consumption by 1.3 percent of GDP, or an additional 1.3 percent of GDP would need to be imported, or some combination thereof. That had to happen regardless of the stance of the Fed.

But this is only one part of the story. Homeowners who tapped their housing wealth by borrowing were only a small portion of the new class of housing rentiers.

Mortgage Growth through the Exodus from Home Equity

Some homeowners also sold their homes in order to realize the capital gains from their newly high prices, but at what scale? This is tough to track because the gains from real estate sales are fungible. They are reabsorbed into a household’s financial portfolio, and there is no way to track exactly what happens to them. According to Census data, homeownership peaked in early 2004.

Existing homeowners were increasingly selling out of the market. According to the Survey of Consumer Finances, mortgaged homeownership was rising, but unmortgaged homeownership declined by 3 percent from 2001 to 2007. Closed Access homeowners were also reducing their exposure to home equity by selling and buying less expensive homes outside the Closed Access housing markets. There was an exodus of existing owners from home equity. This happened in various ways: owners with no mortgages or small mortgages selling their homes to new mortgaged buyers or investors, a shift of owners to less expensive markets, and eventually, by 2006, a sharp decline in home building.

Just consider one of those avenues for reducing exposure to home equity. In the years since the crisis, about 100,000 households who are homeowners have moved away from Closed Access cities each year, according to the American Community Survey. But during the housing boom, that number spiked: in 2005, it was more than 220,000. Closed Access in-migration didn’t change much, so in net terms, compared with recent years in which about 50,000 homeowners move away from Closed Access cities, in 2005 it was more than 150,000.

To put this in context, in a given year, existing home sales in the five Closed Access metropolitan areas add up to a little more than half a million transactions. In other words, about a quarter of home sales in the Closed Access cities during the boom involved a household moving out of the city. That is a tremendous amount of selling pressure. Home prices were so high at the time that the marginal demand for Closed Access homeowners was quite inelastic. The new mortgage products that allowed young households in the Closed Access cities to buy expensive homes on unconventional terms created pricing pressure, but that pricing pressure triggered selling by existing homeowners. High prices triggered new housing supply in the Closed Access cities, but it couldn’t come in the form of much new building. It came by inducing existing homeowners to move away, making their units available for others.

The average price of a Closed Access home in 2005 was about $500,000. So as much as $75 billion in transactions (about 0.5 percent of GDP) involved typically new buyers with large mortgages purchasing homes from others who were moving to less expensive cities. New debt representing some portion of that amount was taken on to complete those transactions. A thorough estimate of this activity is beyond the scope of this paper. My point is to simply establish that this activity was significant and was peculiar to the boom period.

What are the monetary implications of transactions that involved an exodus from home equity by selling an unmortgaged or lightly mortgaged home to a highly indebted buyer? In other words, what is the effect on consumption and inflation when home equity is liquidated by the use of new mortgages, but the mortgage is taken by a new owner and the liquidated equity is taken by an old owner?

In the case where the home has especially high value because of supply constraints, again, this is a transaction involving current and future wealth transfers. The old owner was wealthier because the home was expected to have high future rental value. The new owner, by purchasing the home, was hedging against those future rent increases. For the old owner, the home had become a claim on the incomes of future tenants, and the new buyer was prepaying those future rents by taking ownership of the home. The mortgage for the new buyer might be considered a form of consumption smoothing, but here, current consumption is being reduced. The high mortgage payments buyers were committing to in the present were constraining current consumption in order to provide certainty and control over those high future rental expenses.

This reduction in nonhousing consumption by the new buyers would not typically be counteracted by additional consumption of the home sellers. Home sellers are unlikely to consume all of their capital gains quickly. They are more likely to reinvest them into other low-yield securities—things such as the AAA tranches of securitized mortgages. The net effect of these transactions, triggered by high home prices, would be to reduce nonhousing consumption and increase saving. That saving would supply rising debt.

Implications for Monetary Policy

What do these factors add up to in relation to the posture of the Fed throughout the crisis?

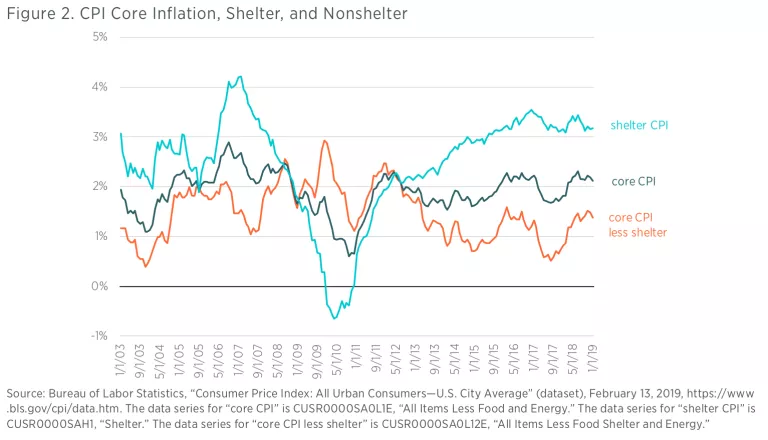

Figure 2 is a graph of Consumer Price Index (CPI) core inflation, disaggregated between the shelter component (which is mostly imputed rent of homeowners) and nonshelter components.

2003–2005

Up to the end of 2005, monetary policy was on point. The Fed was aiming for about 2 percent inflation, and generally, after briefly receding coming out of the 2001 recession, that’s where inflation recovered to. Since the mid-1990s, when the recent problem of urban housing costs first started to develop, shelter inflation had been especially high. While from 1998 to 2005, core CPI averaged about 2 percent, the nonshelter components never really moved above 2 percent.

Most of the shelter component of core CPI inflation is from the estimated rental value of owner-occupied homes, which has nothing to do with monetary transactions and thus is not directly influenced by cyclical monetary policy positions. The nonshelter components of inflation suggest that the Fed was more than counteracting the inflationary effects of growing mortgage debt on other types of spending. At the top of the housing boom at the end of 2005, even though housing starts were capped politically in the Closed Access cities, enough homes were finally being built in the rest of the country that rents in many other cities were moderating. By the end of 2005, rent inflation was finally meeting general inflation right near the Fed target level of about 2 percent. The problem is that in order to achieve that moderate level of rent inflation, a mass migration was triggered out of the Closed Access cities. People had to move to where the homes could be built. The character of that migration was such that states such as Florida, Arizona, and Nevada experienced a rush of households and capital that overwhelmed their local ability to build, and that was destabilizing.

As described previously, the relative distribution of consumption during the boom period was largely out of the Fed’s control. But to the extent that the Fed tried to maintain stable spending in spite of this uneven distribution, nonshelter inflation was below target, and nominal GDP growth was more moderate than it had been in any expansion since World War II. During the boom, in other words, monetary policy was relatively tight, even accounting for mortgage-funded spending.

Yet the Fed is nearly universally panned for having maintained policy that was too loose, and it is blamed for the housing bubble. To this day, both Fed officials and their critics frequently maintain that the primary Fed error of the past 20 years was that it did not produce tighter monetary policy in the boom years. Recognizing that the permanence of urban land values changes this conclusion, Fed policy at the top of the bubble in 2005 was reasonable. Shelter inflation was near the 2 percent target in spite of local structural rent inflation, and nonshelter inflation was near 2 percent in spite of the consumption smoothing of homeowners.

2006–2007

The Fed began to raise the target interest policy rate in 2004, and by the end of 2005, short-term yields were as high as long-term yields. By early 2006, housing starts and residential investment were beginning to drop. Since the primary problem in the housing market was a lack of well-placed supply, this was not a good sign. This development is another example of how the different conceptions of the source of home values lead to vastly different conclusions about the appropriate response. Notice in figure 2 what happened immediately: shelter inflation exploded, but nonshelter inflation collapsed to barely over 1 percent by the time the Fed began to lower rates in September 2007.

Here, policy was problematically too tight, but not disastrously so. And the demand-side conception of the source of high home prices was again the core issue misleading the Fed. First, it blinded them to the negative implications of collapsing housing construction. Secondly, collapsing construction was only reinvigorating the claim of real estate owners to economic rents, and the Fed was measuring that income transfer as inflation.

By August 2007, with the collapse of the private securitization markets, the Fed had finally pushed monetary policy tight enough that it could actually change the distribution of consumption between rentiers and producers. Until then, the declining ability and willingness of American households to own home equity had mostly led to a decline in housing starts. Now prices were starting to collapse. Finally, rentiers were losing their ability to capitalize their future incomes.

The economic contraction that followed the collapse in home values caught policymakers off guard. A negative wealth effect suddenly pulled nominal GDP growth down. But the future rents that had justified that wealth weren’t affected. So, at once, the wealth of the rentiers was reduced, and their ability to shift consumption of that wealth to the present was undercut. But that wealth wasn’t transferred back to future renters. The future rental claims on their incomes were just as strong as they had been. There wasn’t a transfer of wealth back from rentiers to consumers. There was just a negative wealth effect imposed on rentiers by preventing them from capitalizing that future income and consuming some of it in the present.

They now stopped shifting their consumption to the present, and other consumers were not increasing their current consumption to make up for it. During this period looser monetary policy would have been stabilizing, but any stabilizing monetary policy would have invariably increased residential investment and home prices, and both of those outcomes would have been highly unpopular, both inside and outside the Fed.

2008 and After

Nothing has changed the claims that urban real estate is expected to have against future incomes. So, once the volatility of the crisis passed, monetary policy moved back toward a pre-2008 regime, where much of measured inflation is really a transfer of income to real estate owners. Shelter inflation is running greater than 3 percent, and nonshelter core inflation has ranged between 1 percent and 2 percent. This is back to a monetary regime that tends to be below the stated target, but not disastrously so.

Real estate owners continue to face some obstacles that prevent them from consuming from home equity. The value of future rents is as high as it was during the boom, but future rents aren’t fully capitalized in today’s prices. Since the policy reactions to high home prices were based on the notion that loose credit markets were responsible for high prices, prices have been pushed down by obstructing credit rather than reducing the value of future rents by encouraging urban housing supply. Credit markets are being constrained nationally, not just in the Closed Access cities where homes have extra value, so this policy does not counteract the fundamental cause of expensive homes at all.

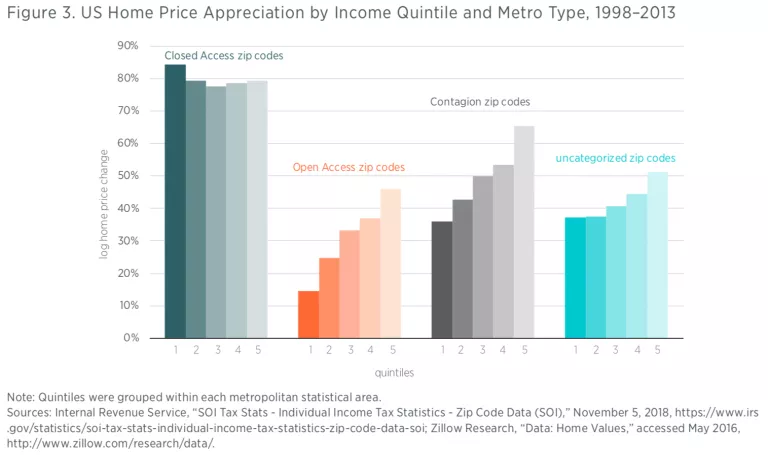

Figure 3 compares the relative changes in home prices in the Closed Access cities and in other cities from 1998 to 2013. (The same basic pattern holds in 2019.) The figure measures the 20 largest metropolitan areas. “Open Access” cities include Dallas, Atlanta, and Houston, where housing supply is ample and prices remained moderate. “Contagion” cities are cities that experienced high in-migration rates that triggered housing bubbles, such as cities in Florida, Arizona, and inland California. The figure shows that rentiers in the Closed Access markets do still get to capitalize some of their new wealth. Regardless of neighborhood income levels, homes in Closed Access cities tend to have gained more than 30 percent in home value compared with other cities.

In other cities, in zip codes with higher incomes, home values tend to typically be around 50 percent higher in 2013 than in 1998—about the same amount that rents have risen over that time. But in zip codes with lower incomes, which face higher credit constraints, prices have been driven much lower. Those zip codes generally contain houses that would sell at near the cost of replacement because they are located in cities that allow the creation of new supply. They were never engaged in the capitalization of economic rents. They instead held assets that tend to earn a fair, competitive rental income, and they are being prevented from capitalizing the value of those rents into today’s prices. This obstacle has been most unfortunate for homeowners in those areas who have been forced to sell.

Regarding its effect on monetary policy, the Fed finds itself, yet again, in a position where it can certainly change the general rate of inflation, but it is relatively powerless to change the distribution of consumption that has been created by tight lending policies. Looser monetary policy could help to reverse the negative or low equity that some low-tier homeowners still have as a result of this shift in real estate values. To some extent, inflation would be helpful. But more nominal spending would be a weak tool to help America’s most economically vulnerable households. They would have a few extra dollars to spend, but so would the Closed Access rentiers and the high-end homeowners in other cities. As in 2005, the primary stresses that characterize the American economy do not have a monetary source or solution, but mistaken monetary attempts at solutions are capable of adding to those stresses. Certainly, there is no reason to tighten policy today as a reaction to high home prices.

Looser credit standards would allow low-tier home prices to rise back to a level reflecting the norms of decades of precrisis, liquid housing markets. Loosening credit standards would be inflationary, but to the extent that low-tier homeowners could make it through the crisis without being foreclosed on and without selling their undervalued homes, the re-attained wealth of a normalized lending market would be highly progressive. It would be progressive because (1) it would allow home equity of low-tier homes to recover, and (2) recovery in those markets would lead to recovered rates of building, adding new supply that would reduce rents for households that rent. The net effects on inflation would be mixed. New credit growth would be inflationary, but more housing supply would be disinflationary, creating an economic situation similar to that in 2005. However monetary policy responds, the key is to avoid triggering a contraction in new housing supply.

Unfortunately, much of the damage of a decade of depression-level housing starts and foreclosures cannot be healed. But at least cyclically stabilizing monetary policy can stop the bleeding.