- | Monetary Policy Monetary Policy

- | Policy Briefs Policy Briefs

- |

A Rule to Preserve Monetary Stability

A perennial criticism of the Federal Reserve (Fed) is its adherence to discretion rather than to an explicit rule in the formulation of monetary policy. With a rule, the FOMC would announce an explicit strategy that imposes discipline on period-by-period changes in its instrument, the funds rate. Specifically, the FOMC would specify a reaction function conditioning how it sets the funds rate in response to incoming information on the economy. With discretion, by contrast, each period the FOMC sets the funds rate based on information available that period without reference to an unchanged reaction function. Because of the lack of explicitness, discretion conveys the message “trust me.”

A rule would increase transparency because the FOMC would have to address explicitly the most basic issues concerning monetary policy. For example, how does the FOMC control inflation? How does monetary policy interact with the price system? Does the price system work well, implying that the FOMC needs procedures for setting the funds rate that track the natural rate of interest (the interest rate determined by market forces unaffected by any interaction between the FOMC’s influence on aggregate nominal demand and “sticky” prices)? Or does the price system work poorly, implying that the FOMC needs to supersede its working by influencing the behavior of real variables through exploiting how changes in aggregate nominal demand interact with sticky prices?

The first section of this policy brief presents a proposed reaction function (rule) and explains the need for it to receive substance through publication of the Board of Governors staff forecasts of the economy that underlie FOMC decision making. Next, the brief discusses how to understand the operation of the reaction function in the context of the New Keynesian model. In the third section, the brief illustrates the reaction function under two versions: one that allows inflation to occur in economic recoveries and one in which policy is preemptive with respect to inflation. The final section distinguishes between uncertainty over the FOMC’s strategy for achieving its objectives and uncertainty produced by the uncertain evolution of the economy.

An FOMC Reaction Function: The Proposal

Monetary policy works through the way in which the FOMC influences the term structure of interest rates (the yield curve). The reaction function (rule) proposed here makes explicit the implicit communication already conveyed to financial markets by the FOMC. Markets arbitrage market interest rates based on the inferred future funds rate path and on an understanding of how incoming information on the economy alters that path. Monetary policy, as opposed to the individual monetary policy actions of setting the funds rate, then works through a reaction function. For monetary policy to exercise a stabilizing influence on the economy, the FOMC must have a reaction function that causes the yield curve to move in a way that offsets unsustainable strength and weakness in the economy.

The FOMC understands that it must communicate to markets a consensus over its expectation for the funds rate path. It does so through the language in the first and second paragraphs of the statement after an FOMC meeting. Changes in the language of the first paragraph express the way in which incoming news about the economy changes the FOMC’s understanding of how the economy is evolving. The second paragraph explains the FOMC’s decision about the funds rate given that understanding. Together, the two paragraphs give content to the FOMC’s lean-against-the-wind (LAW) procedures in a way that reflects the FOMC’s predominant concern. That is, they communicate a concern for unsustainable strength or weakness in growth and a concern for whether markets believe that the funds rate will move sufficiently quickly to restore output growth to trend to maintain price stability. Through consistency in its behavior, the FOMC implicitly communicates a reaction function.

Traditionally, inferring the FOMC’s reaction function was the province of a small number of Fed watchers, often former employees of the New York Fed. The FOMC has enhanced its communication to markets in three major ways: commentary in the first and second paragraphs in the statement issued after an FOMC meeting, the quarterly forecasts summarized in the Summary of Economic Projections (SEP), and the chair’s postmeeting press conference. By becoming more explicit about its forecasts of the economy, the FOMC has broadened the set of Fed watchers capable of inferring monetary policy—that is, a systematic strategy for responding to incoming information on the behavior of the economy.

At the same time, the FOMC has tightly controlled this increased transparency. Athanasios Orphanides refers to the FOMC’s “overly Delphic language.” The FOMC does not explicitly articulate its reaction function. That omission limits the Fed’s accountability and its ability to learn. Monetary policy is complex because evaluation of its influence requires untangling the two-way causation between the Fed’s reaction function and the behavior of the economy. Economists use models to disentangle causation. An explicit reaction function would allow economists to evaluate and debate monetary policy by combining it with a model. In this way, is it possible to learn from experience what monetary policies have stabilized or destabilized the economy. The following accepts actual FOMC decision-making but proposes structuring it within a framework that elucidates the underlying consistency over time. The goal is to make the FOMC’s implicit reaction function explicit.

The reaction function proposed here builds on the work of Orphanides, Orphanides and Simon van Norden, and Orphanides and John Williams. Orphanides explores first-difference rules, which do not require consensus over a numerical value of the output gap, and forecast-based rules, which capture the integral part played by the FOMC’s forecasting.

The reaction function advanced here as a benchmark is

it = it–1 + 0.5 (πt+3|t – π*) + 0.5(yt+3|t – y*t+3|t)+0.5ogt+3|t. (1)

The funds rate for quarter t is it. πt+3|t is forecasted inflation for the quarter three quarters ahead, at time t, and π* is the inflation target. Real GDP and potential GDP (in logarithms) are qt and q*t, respectively. Expressing the variables in logarithms causes the differences to represent percentage changes. Quarterly annualized real GDP growth is yt = (qt – qt–1) x 400, and the potential growth counterpart is y*t = (q*t – q*t–1) x 400. (yt+3|t – y*t+3|t) is forecasted three-quarters-ahead quarterly real GDP growth relative to potential growth. The output gap is ogt = (qt – q*t) x 100. Formula (1) absent the output gap term is from Tealbook (TB) Book B, which is the staff document circulated prior to FOMC meetings to participants and which lays out alternatives for setting the funds rate.

Formula (1) captures the essence of the FOMC’s LAW procedures. Output cannot grow indefinitely above trend without raising inflation; conversely, output cannot grow indefinitely below trend without causing disinflation. The FOMC implicitly agrees on a funds rate path that will cause output to move to and then continue along the path for potential output; that is, one that will keep (yt+3|t – y*t+3|t) = 0. The FOMC gauges expectations of inflation to check that markets do not believe that it is “behind the curve.”

Orphanides estimated the reaction function, formula (2), which is similar to formula (1).

it = it–1 + 0.5(πt+3|t – π*) - (ut+3|t – ut–1|t). (2)

The forecasted change in the unemployment rate captures whether the economy is growing faster or slower than its potential, as measured by whether the rate of resource utilization in the labor market is declining or rising. As a proxy for the forecasted values, Orphanides uses the Survey of Professional Forecasters (SPF) and, when it becomes available, the FOMC SEP forecasts made quarterly by FOMC participants, measuring inflation by the core personal consumption expenditures (PCE) deflator. Orphanides writes,

Evidently, even though the FOMC has not clearly articulated a policy strategy, its policy decisions can be broadly characterized with a simple and robust monetary policy rule that is based on participants’ economic projections . . . . Simple policy rules based on near-term projections of inflation and economic activity can serve as a useful tool to communicate the Federal Reserve’s strategy and provide a rationale for policy decisions.

The terms in the reaction function shown in formula (1) are forecasts, not hard data. That fact reflects actual practice, which, in part, reflects lags in the availability of data. The formula also possesses the advantage that a forecast removes the idiosyncratic noise of the contemporaneous behavior of the economy. The issue is how to make the FOMC accountable for those forecasts through public scrutiny. The proposal here builds on that concern: at its first meeting of the year, FOMC participants would articulate a reaction function. For the remainder of the year, the Board of Governors staff would prepare their forecasts using that reaction function. As now, at quarterly meetings, the FOMC would release an SEP, but the SEP would be a consensus FOMC forecast. As essential background, the FOMC would also release the TB Book A, containing the Board of Governors staff forecasts. Presently, TBs are released only with a lag of five calendar years.

The staff makes a state-of-the-art forecast of the economy based on discussions among numerous economists devoted to following the economy. The TB accompanies its forecast with an encyclopedic review of the economy. As captured by formulas (1) and (2), the FOMC works off forecasts of the economy. There is no feasible way, however, that the 19 participants sitting around the boardroom table could by themselves arrive at a consensus forecast of the economy. Necessarily, they start with and then modify the TB forecast. In the case of the regional bank presidents, contacts in the business community furnish additional near-real-time information on the economy. Scrutiny of the consensus FOMC SEP forecast of the economy by outside observers, therefore, would necessarily start with the detailed base forecast in the TB and then examine the plausibility of the FOMC’s modification.

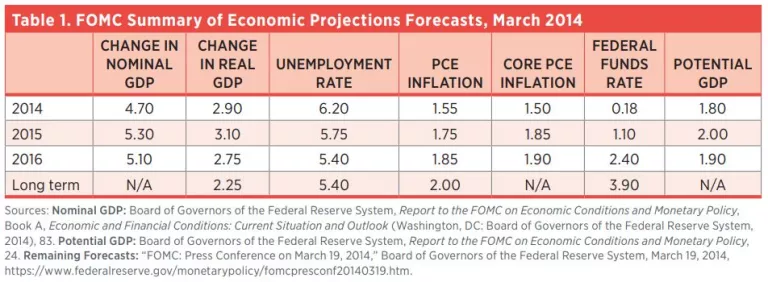

Table 1 presents SEP forecasts from the March 2014 FOMC meeting. It expands the forecasted variables by including nominal GDP and potential GDP. Values for those variables are taken from the March 12, 2014, TB Book A.k A with the staff forecasts would be publicly available. The FOMC forecast could be more optimistic or more pessimistic about the economy than the staff’s forecast. The chair would explain the reasons for any differences between the FOMC’s outlook on the economy and the TB’s outlook and the corresponding difference in the projected funds rate path. Because the consensus FOMC SEP forecast presented by the chair would not be constrained by the reaction function in formula (1), the FOMC then would not be strictly constrained to follow a rule but would possess considerable room for judgment.

However, the chair would discuss the funds rate decision using formula (1). The following illustrates a hypothetical discussion by the chair for the March 2014 press conference. Using formula (1) with forecasts provided by the March 2014 SEP forecasts yields the following: πt+3|t =1.6 and π* = 2; yt+3|t = 3.5 and y*t+3|t = 1.8; and ogt+3|t = -1.9. Putting those numbers into formula (1) yields a reduction of the funds rate of −0.65. At the March 2014 FOMC meeting, the funds rate was at the zero lower bound (ZLB). If the number released at the prior quarterly SEP meeting had been smaller in magnitude—say, −0.25—such a forecast would likely cause markets to extend their expected liftoff date for the funds rate. The combination of the ZLB and a recommended reduction in the funds rate could explain the contemporaneous quantitative easing (QE), while the declining unemployment rate shown in the SEP could explain the modest tapering undertaken at the March meeting.

An FOMC consensus SEP would enhance transparency. The current SEP is a jumble of 19 separate forecasts lacking in coherence in that there is no way to organize the individual forecasts as a coherent whole coming from a particular individual. The forecasts depend upon what the individual participant deems the appropriate funds rate path. That condition is a way of ensuring that each participant makes a forecast that in the long term achieves the dual mandate.

Moving to an Explicit Analytical Framework

The discussion here takes formula (1) as the reaction function that characterizes the Greenspan era and interprets it in the context of the New Keynesian model as exposited by Marvin Goodfriend and Robert King. I term this monetary regime lean-against-the-wind with credibility.

Consider the FOMC’s task of controlling inflation. The FOMC has an inflation target but has never explained how it controls inflation. It does not exercise direct control over the spending of households. There is no wartime rationing. The FOMC does not set the dollar prices of the products that corporations produce. There are no wartime price controls. How then does it achieve its inflation target, which requires that, collectively, firms set their dollar prices so that they average 2 percent annual growth? Somehow, manipulation of the funds rate, which is an overnight rate of interest, translates into achievement of a desirable level of nominal spending and inflation. But without communication in terms of an analytical framework and a reaction function, the conduct of monetary policy remains at the “trust me” level.

To provide for price stability, the FOMC must cause aggregate nominal expenditure to grow in line with the economy’s potential real output. It moved to such a policy in the Volcker-Greenspan era with the abandonment of attempts to exploit Phillips curve tradeoffs. The policy rested on establishing a credible rule that provided a stable nominal anchor by coordinating firms’ expectations of inflation on price stability. Firms in the sticky-price sector, that is, firms that set prices for multiple periods, take that common expectation as a baseline for setting prices. The determination of relative prices takes the form of deviations from this baseline. The FOMC can then separate the control of inflation (the price level) from the behavior of the real economy (relative prices). It turns the determination of real variables like output and unemployment over to the private economy by following a rule that causes the funds rate to track its natural counterpart (the real interest rate determined by the real business cycle core of the economy).

Because data arrive with a lag, policymakers must forecast the contemporaneous behavior of the economy and its near-term evolution. Consider first inflation, which is a combination of inflation in the sticky-price sector and in the flexible-price sector. Only the former is relevant for a rule that allows the price system to determine real variables. As an approximate measure of underlying inflation, the FOMC uses the core PCE deflator. However, to some extent, inflation from the flexible-price sector passes through to the sticky-price sector. In the COVID-19 crisis, the worldwide decline in commodity prices biased downward the measure of core PCE inflation. The March consumer price index report shows that the pandemic produced declines in apparel, hotel, and airfare prices. The inflation measure used by the FOMC should account for such downward bias, for example, by using the Dallas trimmed mean measure of PCE inflation.

Consider next real output. The FOMC assesses whether the economy is growing faster than its potential based on whether rates of resource utilization are increasing (unemployment falling). That is the heart of the FOMC’s LAW procedures. Sustained growth above potential indicates that the real rate of interest lies below the natural rate of interest. In response, the FOMC raises the funds rate somewhat above its prevailing value, always watching financial markets to assess whether the markets believe that increases will, in time, cumulate to whatever extent necessary to maintain price stability. The converse holds if the FOMC assesses that the economy is growing more slowly than its potential (that is, unemployment is rising). The FOMC then lowers the funds rate below its prevailing value.

The output gap, which is the difference between actual and potential output, is measured only with great imprecision. Nevertheless, the FOMC must operate with some estimate of it. Consider an economic recovery in which the output gap is clearly negative. Assuming no attempt to exploit a Phillips curve, the FOMC wants real GDP to grow faster than growth in its long-term potential but not to overshoot the path of potential real GDP. The problem is difficult because inflation is not a useful indicator in that it responds to an overshoot of output from potential (a positive output gap) only with a long lag. In the Greenspan era, in order to achieve a return to the path of potential output along a glide path, the FOMC began to raise the funds rate more aggressively when it saw signs of inflationary pressures (that is, signs of excess tightness) in labor markets. The FOMC knows that the output gap is zero when the economy grows at a rate that does not cause a sustained change in rates of resource utilization.

Using a Reaction Function to Clarify the FOMC’s Strategy

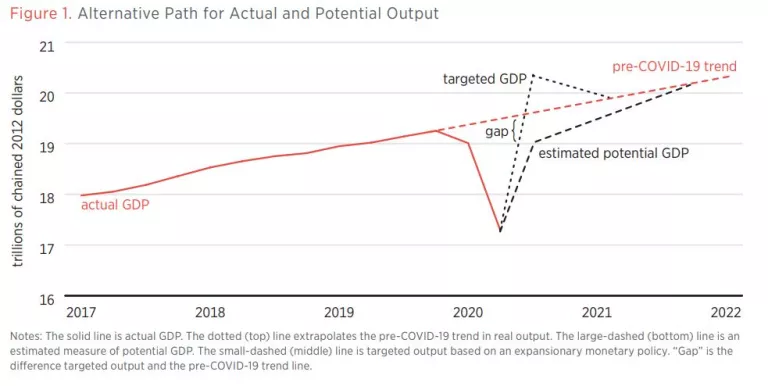

The reaction function illustrated in formula (1) does not restrict the FOMC to a particular strategy. Rather, it clarifies the strategy the FOMC is following. On August 27, 2020, with a speech by Chair Powell announcing the results of the Fed’s monetary policy review, the FOMC moved in the direction of an explicit reaction function. As illustrated in figure 1, it wants output to grow faster than its potential, (yt+3|t – y*t+3|t) > 0, so that the output gap, ogt+3|t , turns from negative to positive. The FOMC measures the output gap relative to the pre-COVID-19 trend line for potential output. Inflation should rise above 2 percent for a period of time π*t > 2.

Powell stressed that achievement of these results meant abandoning the earlier policy of raising the funds rate preemptively during economic recovery to avoid inflation:

In earlier decades when the Phillips curve was steeper, inflation tended to rise noticeably in response to a strengthening labor market. It was sometimes appropriate for the Fed to tighten monetary policy as employment rose toward its estimated maximum level in order to stave off an unwelcome rise in inflation. The change to “shortfalls” [as opposed to “deviations”] clarifies that, going forward, employment can run at or above real-time estimates of its maximum level without causing concern . . . . [F]ollowing periods when inflation has been running below 2 percent, appropriate monetary policy will likely aim to achieve inflation moderately above 2 percent for some time.

The analytical framework summarized in the second section highlights the pitfalls in Powell’s approach. First, underlying inflation is not well predicted by an output gap, especially the one used by the FOMC (shown in figure 1 as “gap”). As argued by Kosuke Aoki and Gregory Mankiw and Ricardo Reis, underlying inflation derives from the number that firms in the sticky-price sector (firms setting prices for multiple periods) coordinate on when setting nominal prices. Starting with the Volcker disinflation and continuing through the Great Recession, the FOMC has conditioned these firms to set prices based on the assumption of near price stability. The resulting inflation is, as of August 2020, close enough to the FOMC’s 2 percent target not to be of concern. Using the Dallas trimmed mean for PCE inflation, over the period February 2011 to February 2020, inflation remained fairly steady at 1.8 percent. In the COVID-19 crisis, the monthly figure for March 2020 fell to 1.1 percent but rose back to 1.7 percent in June 2020.

Second, the shock that initiated the COVID-19 recession was an exogenous reduction in productivity. Restaurants, cultural events, and sports events could no longer offer hygienically safe products. Liquidity-constrained households that suffered layoffs and could not borrow to smooth consumption received payments through the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Unlike past recessions, the shock was not a negative aggregate demand shock. For that reason, responding with expansionary monetary policy risks an uncontrolled rise in inflation. The FOMC should aim to maintain an amount of nominal expenditure sufficient to accommodate the recovery in potential output (the large-dashed line in figure 1 labeled “estimated potential GDP”) and maintain the current near price stability.

The FOMC should maintain aggregate nominal demand based on the path for “estimated potential GDP” in figure 1 rather than on the more aggressive path that lies above this line. The FOMC’s estimate of the output gap should be based on “estimated potential GDP” rather than on the “pre-COVID trend” line. The FOMC should normalize the size of its asset portfolio by letting securities held outright run off or be sold, depending on market conditions. Given the normal functioning of financial markets, it should terminate the 13(3) credit programs.

The FOMC should implement a reaction function with upward and downward flexibility in the funds rate target (including negative interest on reserves in the event of weakness in the economy). As the economy recovers, it should raise the funds rate target based on signs of overheating of the economy such as lengthening supplier deliveries and tightness in labor markets. As in the Greenspan era, the FOMC should forecast movement of the output gap from negative to positive based on indicators that rates of resource utilization are stretched. There should be no presumption that potential output is defined by its prepandemic state. There will likely be long-lasting effects from the COVID-19 crisis, such as increased labor mismatch, an augmented push to automation and robots, increased remote working, and others. As a benchmark, the FOMC should make certain that the spring bulge in money unwinds. The increased demand for liquidity represented by the bulge should dissipate as the economy recovers.

How Transparency from an Explicit Reaction Function Will Enhance Public Debate

The transmission of monetary policy occurs through the way in which the FOMC influences the level and slope of the yield curve. It can tie down the short end of the curve with its funds rate target, but the slope of the yield curve arises out of two interacting factors. The first is the market’s understanding of the FOMC’s reaction function; that is, how does the FOMC respond to incoming information about the economy? The second is the market’s forecast of the evolution of the economy. Transparency and open debate require clarity about each.

The debate in February 2015 makes these points. As determined by the market for Fed funds futures, the expected future path for the funds rate lies significantly below the path assumed by the FOMC consensus. As commonly assumed, the median value of the FOMC’s dot plot released with the quarterly SEP measures the latter, the FOMC consensus view. What is relevant for monetary policy are not the forecasts of FOMC members but rather the market’s judgment. Making monetary policy in real time is inherently difficult because of the difficulty in forecasting the evolution of the economy. Nevertheless, the formulation of policy can only be helped by an open debate structured around the reasons for this kind of divergence between FOMC and market views. Which view is right—the FOMC consensus or the market? And why? Perhaps the market believes either that the current funds rate is too high or that the probable increases by the FOMC shown in the FOMC’s dot plot are unwise, given weakness in the economic forecasts.

As explained in the first section of this brief, markets infer the consensus funds rate path in part from the way the FOMC changes between meetings the language in the first and second paragraphs of the postmeeting statement. The full FOMC reaches a consensus on that language. However, changes in the language translate only loosely into changes in the FOMC’s expected funds rate path. Consider the need for markets to interpret the directive language illustrated by the congressional testimony of Chair Yellen when discussing the significance of possibly dropping the word “patient.” According to Macroeconomic Advisers, “Dropping the ‘patient’ language . . . means that ‘it will soon be the case that a change in the target range could be warranted at any meeting . . . .’ She said that the FOMC will ‘at some point begin considering an increase in the target range for the federal funds rate on a meeting-by-meeting basis.’”

Chair Yellen’s statements in early 2015 came from the need to drop the word “patient” from the FOMC statement in preparation for liftoff; that is, raising the funds rate above the ZLB. In general, the FOMC dislikes surprising markets with a change in the funds rate for fear that an undesirably strong reaction of the yield curve will produce an undesirable change in the stance of monetary policy. In this case, the fear was of a sharp rise in the yield curve, as had occurred with the May 2013 “taper tantrum.” At the same time, the FOMC added to the uncertainty over its future actions. That uncertainty appeared in an exchange in fall 2015 between New York Fed president William Dudley and Stanford professor John Taylor: “I don’t really understand what is unclear right now,” said Dudley. “Are you kidding?” Taylor said. “No one knows what you’re doing.”

The market’s uncertainty over the liftoff date for the funds rate came from two sources: policy and forecasts. The economy appeared to be approaching full employment. Somewhat later, LH Meyer wrote, “The good news is that we are at full employment and near price stability. The question is what the rate path is that will, in effect, keep us there.” Policy uncertainty arose over whether the FOMC would follow the Greenspan policy of raising the funds rate to preempt inflation or whether it would depart and wait until inflation, which was somewhat below target, reached the FOMC’s 2 percent objective. Forecast uncertainty arose from weakness in the world economy and whether that weakness would weaken the domestic economy. The proposal here would eliminate policy uncertainty and focus debate on the forecast uncertainty.

Final Comment

The FOMC “Statement of Longer-Run Goals and Monetary Policy Strategy” includes the language: “The Committee seeks to explain its monetary policy decisions to the public as clearly as possible. Such clarity facilitates well-informed decision making by households and businesses, reduces economic and financial uncertainty, increases the effectiveness of monetary policy, and enhances transparency and accountability, which are essential in a democratic society.” The most important step the FOMC could take toward fulfillment of this statement of intent would be to move away from the language of discretion by formulating an explicit reaction function. Choice of a reaction function would also facilitate discussion of a model of the economy explaining how the reaction function allows the FOMC to achieve its objectives for inflation and employment.

The reaction function proposed here builds on existing practice. In that sense, it is not radical. It is radical only in that it moves the FOMC toward greatly increased transparency and accountability. However, the additional explicitness is important. The FOMC possesses an incentive to control the public narrative through the language of discretion: each period, policy actions are assumed optimal in light of the contemporaneous state of the economy. The implicit assumption then is that the concatenation of policy actions assures an optimal monetary policy over time. Adverse outcomes must then derive from external shocks. However, productive dialogue with the academic community would require communicating in terms of a strategy; that is, a consistency in policy (a rule) maintained over time. Such a dialogue is required for understanding the evolution of monetary policy and the resulting evolution of the monetary regime determined by the Fed. Monetary stability is the ultimate prize.

About the Author

Robert L. Hetzel was an economist at the Federal Reserve Bank of Richmond from October 1975 to January 2018. He is a visiting scholar at the Federal Reserve Bank of Chicago; a senior affiliated scholar at the Mercatus Center at George Mason University; and a fellow in the Institute for Applied Economics, Global Health, and the Study of Business Enterprise at Johns Hopkins University.