- | Monetary Policy Monetary Policy

- | Federal Testimonies Federal Testimonies

- |

Safeguarding the Federal Reserve's Independence

Testimony before the Subcommittee on National Security, International Development, and Monetary Policy of the House Committee on Financial Services

Chair Himes, Ranking Member Barr, and members of the subcommittee:

Thank you for inviting me to discuss the emergency lending powers of the Federal Reserve (Fed). My name is Christopher Russo. I am a postgraduate research fellow at the Mercatus Center at George Mason University, where my research focuses on central banking. Before joining the Mercatus Center, I held roles at the Federal Reserve Bank of Chicago and Federal Reserve Bank of New York, advising senior officials on a range of monetary policy decisions.

Today, I urge you to safeguard the Fed’s political independence, which is the backbone of good monetary policy. My arguments can be boiled down to three points.

- The Fed’s role as the lender of last resort (LOLR) is essential to achieving its dual mandate of maximum employment and price stability. As the LOLR, the Fed provides liquidity to the entire financial system in times of crisis.

- Ten of the Fed’s recent emergency lending programs crossed “red lines” from monetary policy into credit policy by directly or indirectly providing new credit to corporations, states, and municipalities.

- Credit policy is not the Fed’s proper role. The Fed’s independence is damaged when it is opened to intense lobbying by Congress and special interest groups alike, which occurs when the Fed is required to aid specific nonbank borrowers on Wall Street, K Street, or even Main Street.

In my comments, I do not wish to pass judgment on the actions that Chair Powell, the Federal Open Market Committee, or the Federal Reserve System took as they responded to the COVID-19 crisis. Rather, I hope to assist Congress as it considers and designs a future for the Fed that preserves and protects its role as the LOLR.

MAIN STREET REQUIRES AN EFFECTIVE LENDER OF LAST RESORT

As the LOLR, the Fed’s job is to support the private creation of money by banks. Without a LOLR, banks pulling back on lending can shrink the overall supply of money. The shrinking money supply can cause sound banks to fail in a dash for cash. Those failures further reduce the money supply, triggering a chain reaction that could result in a recession or, worse—as history has shown—a depression.

The LOLR prevents such a chain of events. To avert a crisis, the Fed, as the LOLR, lends to banks without limit, in a timely manner, based on good collateral, at a penalty rate. These loans are not meant to finance new investment.

SOME FED EMERGENCY LENDING HAS CROSSED RED LINES INTO CREDIT POLICY

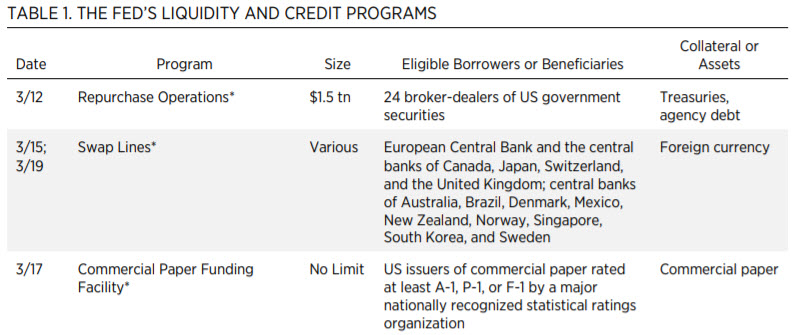

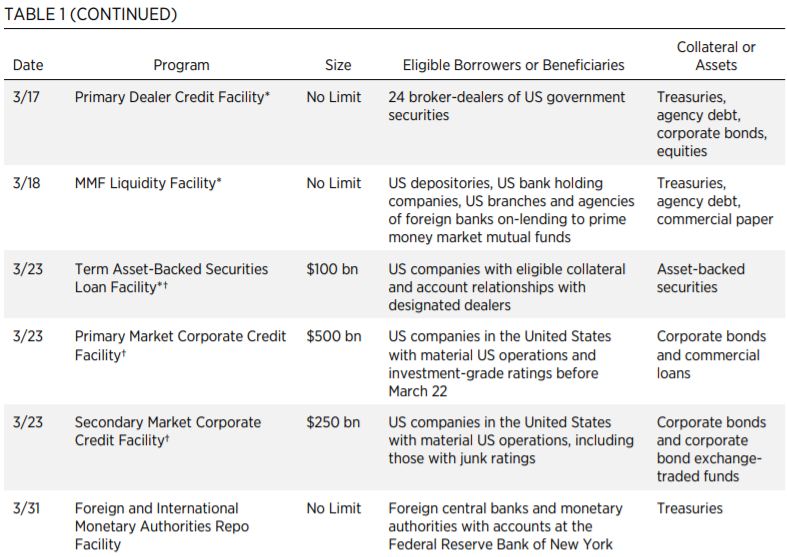

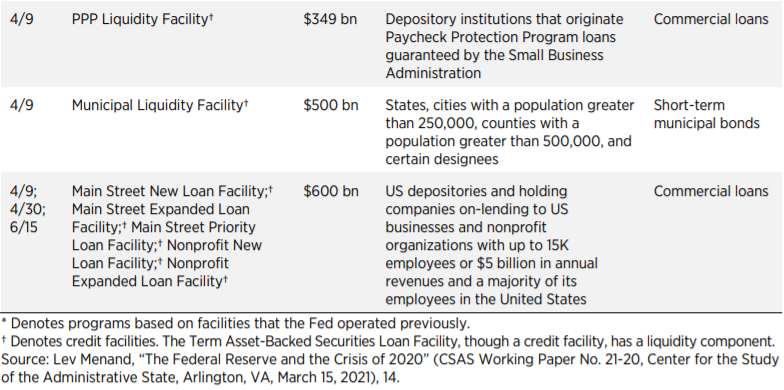

When the global economy was forced into a sharp contraction in March 2020 as the pandemic swept the world, the Fed unleashed a firehose of emergency lending. By one count, it set up about 16 programs (table 1). Six of these programs were designed to provide liquidity to the “shadow banking system,” which is not eligible for lending through the Fed’s traditional LOLR tools. These six programs extend the LOLR doctrine to meet recent institutional developments.

The other 10 programs were intended to assist Congress and the Treasury in allocating credit. These credit programs are beyond the traditional LOLR doctrine. For example, the Fed’s municipal loan facility made direct loans—and only to the State of Illinois and New York City Metropolitan Transit Authority. As Chair Powell has described it, the Fed’s response to the crisis “crossed a lot of red lines.” When I sought more information about the Fed’s risk management practices, my requests were denied.

CONGRESS SHOULD KEEP THE FED INDEPENDENT AND EFFECTIVE BY LIMITING ITS ROLE IN CREDIT POLICY

Congress last reformed the Fed’s emergency lending powers with the 2010 Dodd-Frank act. Congress specified that emergency lending is for “unusual and exigent circumstances.” It must be “broad-based” and only “for the purpose of providing liquidity to the financial system.” These restrictions insulate the Fed’s decisions from direct political pressure.

However, seeing the Fed’s success in the pandemic, some elected officials have argued for the Fed to take a permanent role in credit policy. Congress should resist this siren call of turning the Fed from a central bank into a piggy bank. Whether the Fed finances green energy or the construction of a border wall, the transformation of its role would subject the Fed to intense political pressure from policymakers and lobbyists. By damaging the Fed’s independence, such pressure would harm its capacity to be the LOLR during the next crisis.

CONCLUSION

Congress has charged the Fed with the goals of maintaining stable prices and maximum employment. The Fed’s independence is critical to achieving those goals. But that independence will be threatened by injecting the Fed into national credit policy. Thank you again for inviting me to speak. I look forward to answering your questions.