- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

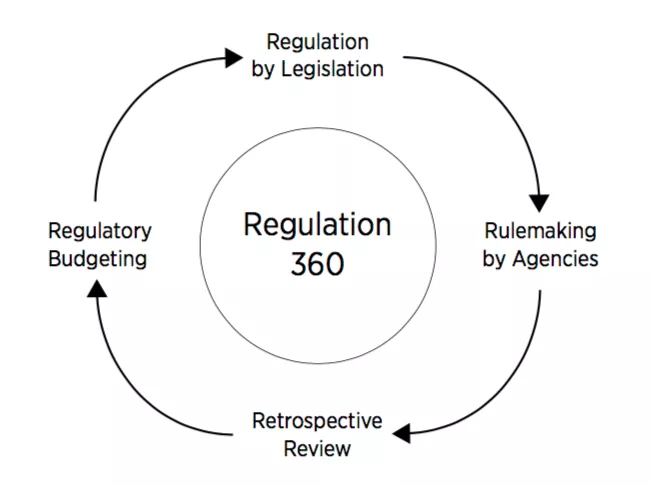

Regulation 360: Why We Must Reform Our Regulatory System (and How to Do It)

Like most things in life, federal regulations can come with costs as well as benefits. The process by which regulations are crafted should inform decisionmakers about these tradeoffs. Legislators and regulatory agencies must have the information necessary to assess the effects of mandates and rules to ensure that they are making optimal decisions.

This is something that decision makers have been ill equipped to do in our current regulatory system. As a result, there has been too much regulating in the dark.

Reasonable people can disagree about the tradeoffs they are willing to make to get a desired outcome. But surely they can agree that we should not adopt regulations unless we are reasonably sure that they will solve a real problem at an acceptable cost.

- Regulation by Legislation

- Rulemaking by Agencies

- Retrospective Review

- Regulatory Budgeting

Each of these four stages is important in and of itself. The stages’ interaction is vitally important too. That’s why this brief is called “Regulation 360.” The process envisioned here is a circle, with each stage building on the one before it.

Regulatory budgeting, however, is not the end of the line for the dynamic regulatory process. Instead, it in turn continues to inform regulation by legislation, starting the whole process off again in its clockwise circle: Regulation 360.

A Principles-Based Approach

Regulatory policy is the responsibility of Congress, regulators, and the regulated. Executive orders lay out the fundamental requirements of a well-functioning system. For example, Executive Order 13563 states the following:

“Our regulatory system must protect public health, welfare, safety, and our environment while promoting economic growth, innovation, competitiveness, and job creation. It must be based on the best available science. . . . It must take into account benefits and costs. . . . It must measure, and seek to improve, the actual results of regulatory requirements.”

In considering the outcomes of regulations, Congress and the various regulatory agencies should be guided by the following principles. These principles can help make the regulatory process more transparent and decision makers more accountable for tangible outcomes.

- A regulation should solve a real, widespread problem—the problem that it sets out to address.

- A regulatory agency should be able to prove a regulation is likely to make people’s lives better in significant ways. Regulatory proposals should specify the ultimate outcomes that benefit people, not just the inputs, activities, or processes. Regulation requires evidence, not just assertions—good intentions are not enough.

- Regulators should define how they will know when the problem is solved and no additional regulation is necessary. Simply put, for any regulation, what counts as success?

- Multiple alternative forms of regulation (and alternatives to regulation) should also be considered. These could include fees, bonds, insurance, changes in liability rules, definition or redefinition of property rights, and information provision or disclosure.

- Policymakers should aim to provide the most benefits to the public for the least cost—the “biggest bang for the buck.” In other words, they should make choices that maximize net benefits.

- Regulation should not unfairly benefit some groups or technologies at the expense of others. Picking winners and losers in this manner should be avoided.

- Regulation should be based on the best available evidence, not on wishful thinking.

These principles must be front and center throughout the regulatory process. They should guide the approach of Congress and the regulatory agencies as well as the manner in which those entities interact. They should also inform the conduct of regulatory review and the implementation of regulatory budgeting.

Regulation by Legislation

Congress is responsible for setting broad regulatory mandates through legislation. Indeed, between 2008 and 2013, some 49 percent of prescriptive, economically significant regulations were required as a result of statute.

However, Congress suffers from scarce information about the scope and consequences of its actions. This scarcity of information leads to poor regulatory decision-making.

Assessing the benefits and costs of proposed action can be challenging. But this is not an excuse for failing to conduct benefit-cost analysis—in fact, it is a reason to do it. As long as it is not intentionally biased, imperfect information is better than no information at all.

Mandates Poorly Made

The case of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 is illustrative. Congress passed the legislation in response to the financial markets meltdown that had begun three years earlier. As often happens with crisis legislation, much of Dodd-Frank was crafted in haste. This decreased its likelihood of delivering on its promises and increased the likelihood of producing unintended consequences.

- The legislation sought to solve the too-big-to-fail problem that led to the massive bailouts during the financial crisis. However, its implicit government guarantee to “systemically important” firms actually encourages large firms to take on more risk, because it is taxpayers who ultimately bear that risk, not the firms.

- Smaller financial institutions (“community banks”) may not have been the intended target of the legislation. But they are poorly equipped to deal with Dodd-Frank’s increased compliance costs. This gives big banks a competitive edge over their smaller rivals.

- Dodd-Frank does not reform the broken housing-finance system. It ignores Fannie Mae and Freddie Mac, the government-sponsored mortgage giants at the heart of the crisis.

- Measures intended to protect consumers ended up harming them. These harms may include threats to privacy, decreased consumer choice, and increased consumer costs.

The Dodd-Frank Act was passed without (1) the benefit of thorough economic analysis of its potential impact and (2) sufficient consideration of alternative paths for remaking the financial regulatory system. The bill’s size and complexity made it difficult for members of Congress to fully understand its provisions before voting on it. Congress often makes decisions based on political concerns with minimal consideration of foreseeable unintended consequences, and this case was no different.

In addition, Dodd-Frank created a number of powerful new regulatory agencies: the Consumer Financial Protection Bureau, the Financial Stability Oversight Council, and the Office of Financial Research. However, these agencies are shielded from accountability to Congress.

Key Questions to Stay on Track

Congress should have an organized process for obtaining critical information before it decides whether to write regulatory mandates into statutes. When considering a proposed bill, it should ask and answer the following key questions:

- What is the problem the legislation is intended to address?

- What is the desired outcome, and how can progress be measured?

- What are the alternative solutions to the problem?

- What are the benefits and costs associated with the various alternatives?

These questions will help Congress continually focus on outcomes.

When it comes to regulations, results are what count, not intentions. Only by continually seeking answers to the questions above can Congress properly assess the impact of its actions and properly perform its regulatory role. All new legislation should be accompanied by prospective economic analyses of the associated economic costs.

Rulemaking by Agencies

While federal regulations originate from acts of Congress, they are developed and enforced by the various regulatory agencies. Agencies take the broad policy mandates contained in statutes and create more detailed regulation through rulemaking.

Regulation and Tradeoffs

Americans expect regulations to accomplish a lot of important things. Regulations have the potential to protect us from financial fraudsters, prevent workplace injuries, preserve clean air, and deter terrorist attacks.

As mentioned earlier, however, regulation requires sacrifices and tradeoffs—there is no free lunch. Depending on the regulation, consumers may pay more, workers may earn less, our retirement saving may grow more slowly as a result of reduced corporate profits, and we may have less privacy or less personal freedom.

Just like lawmakers passing legislation, regulatory agencies should craft rules with knowledge of their likely results. A decision maker’s failure or refusal to acquire this knowledge before making a decision is a willful choice to act based on ignorance.

“Ready, Fire, Aim”

Agencies must conduct analysis early enough in the rulemaking process that the analysis can inform their decisions.

In practice, it is not uncommon for agencies to analyze just one alternative—the regulation being proposed or finalized. This suggests that no other alternatives were seriously considered. Worse, agencies often conduct analysis after a decision to regulate has already been made. This is sometimes referred to as the “ready, fire, aim” problem in rulemaking.

A clear danger of performing analysis too late is that it will be used as a tool to justify regulations, instead of informing how regulations are designed. This is especially relevant given the fact that the heads of regulatory agencies are political appointees. As a result, the chain of command ensures that regulatory decisions are influenced by political considerations.

Another challenge is that the current regulatory process often suffers from misaligned incentives. That’s because regulatory agencies often behave as if their job is to produce regulations rather than to produce outcomes. For an agency, success is issuing as many regulations in a year as staffing and resources permit—not examining whether those regulations are necessary or deciding not to issue regulations in situations where they are unwarranted.

For these reasons, Congress must continue to play an important role in the rulemaking stage of the regulatory process.

Legislators are charged with overseeing how well the implementation of regulations conforms with congressional intent. This oversight role includes efforts to limit mission drift or noncompliance by the agencies. It also can force the agencies to create and deliver better information about the consequences of their actions.

Congressional Oversight in Practice

Unfortunately, the scope and scale of congressional oversight is far from what it should be. The sheer volume of rules produced means that oversight of regulatory agencies is more limited than ever. This occurs even when Congress, in authorizing legislation, has specified a desired outcome. Agencies often develop rules without demonstrating (using evidence) that they are likely to accomplish the outcome.

In addition, regulation inevitably produces unintended consequences. Actual outcomes may turn out to be dramatically different from a statute’s intended purpose, and they can have indirect effects on third parties, either intended or unintended. For example, a regulation requiring gasoline to have higher levels of ethanol (which is made from corn) led to higher global food prices as well as higher prices for livestock feed. These higher prices hit lower-income American households especially hard.

The current legislative and regulatory processes do not adequately inform Congress about the costs and consequences of its regulatory mandates.

Key Questions to Stay on Track

- What are the benefits and costs of any proposed rules?

- Has the analysis been completed before a decision is made?

- Is regulation the best way to produce the desired outcome?

Retrospective Review

After Congress has passed its legislation and the regulatory agencies have completed their rulemaking, agencies must continue to review the benefits and costs of regulation.

“Outmoded, Ineffective, Insufficient, or Excessively Burdensome”?

Executive Order 13563 requires agencies to carry out a review of existing regulations to determine if the regulations are “outmoded, ineffective, insufficient, or excessively burdensome.” If any regulations are so found as a consequence of this review, agencies must modify, streamline, expand, or repeal the regulations.

Unfortunately, effectiveness and efficiency of rules are rarely evaluated in hindsight.

In our current system, an agency’s primary objective is to fulfill its mission via the promulgation of rules. Perhaps not surprisingly, agencies lack impartiality in reviewing their own regulations. They also lack incentives to produce information necessary to analyze rules. That’s because their budgets are tied to the amount of rules that they have to enforce.

In addition, agencies make little effort to engage in retrospective (i.e., backward-looking) analysis of existing regulations to improve the measurement of actual results. They are thus ill equipped to evaluate whether actual benefits exceed costs.

With the number of regulations on the rise, a reliable practice of review is critically important to judge how well or how poorly existing regulations actually work and then to revise the regulations accordingly.

Regulatory Accumulation

Every president since Jimmy Carter has vowed to reduce the amount of red tape built up in federal regulations. Yet every presidential term has produced a net increase in regulation. The consequences of this “regulatory accumulation” are significant. One recent study estimates that the regulations adopted between 1980 and 2012 slowed GDP growth by about 0.8 percentage points annually.

Previous efforts at regulatory cleanup have failed. We need a new process for the systematic retrospective analysis of regulations if we want to break this pattern.

After a regulation is implemented, Congress must continue to monitor progress toward the goal of the regulation by conducting oversight hearings. This requires a robust review of what the regulation has achieved. Doing so will address a significant failing of the current system—the lack of a follow-up necessary to determine the actual social and economic benefits and costs that have resulted from legislatively authorized regulation.

Key Questions to Stay on Track

- How close have the regulations come to delivering the intended results?

- What costs have been incurred in doing so?

Regulatory Budgeting

Federal regulations have been on the rise for the past five decades. And as indicated above, there are significant benefits and costs associated with these regulations (both new and accumulated). Costs are not just the paperwork burden or other compliance costs. They also include hidden costs such as the negative effects of regulation on innovation and on entrepreneurship, both of which are critical drivers of economic growth.

Congress has no analytical arm that annually estimates and tracks those benefits and costs in the same way that the Congressional Budget Office scores the budget.

Regulations have economic effects similar to taxes and spending, and they are a mechanism for transferring wealth. Consider, for example, a regulation that requires the installation of a new environmental protection technology at power plants. This requirement would have many of the same effects on energy prices as a tax on carbon. While the tax would appear in a government budget, the regulatory requirement would not.

What Can a Regulatory Budget Do?

A budget can provide a reliable baseline to which future changes can be compared. It can produce informative projections of future costs. And it can be used as a tool to simultaneously correct errors and control the growth of the regulatory burden.

To be most effective, a regulatory budget should consider economic costs, not just the budgetary outlays of proposed legislation. This will help Congress and agency staff better assess tradeoffs and prioritize accordingly. The budget should incorporate both forward-looking and retrospective review.

These elements will create a feedback loop to better communicate to Congress the impact of regulation.

New Incentives

A regulatory budget would incentivize different behavior by agencies when it comes to proposed and past regulations.

- First, agencies would seek to avoid new regulations that would not achieve high benefits relative to their budgetary costs.

- Second, they would seek to eliminate old regulations that have proven ineffective or inefficient.

In other words, a regulatory budget process would resemble an error-corrections process.

For Congress, a budget attaches a price tag to different regulatory options—costs are put “on the books.” Simultaneously, retrospective and forward-looking analysis communicate information about whether those options have been or are likely to be effective in delivering the legislation’s intended outcomes. Congress then must choose how much the delivery of those intended outcomes is worth.

This places the central question in the regulatory process—the valuation of benefits—squarely in Congress’s control.

Key Questions to Stay on Track

- Does the budget involve planning, setting priorities, and making decisions?

- Does it help in making tradeoffs between competing wants and limited resources?

- Does it force the spender to identify and prioritize the most valuable options?

The problems with the US government’s regulatory process have occurred under Congresses and administrations controlled by both political parties. The problems are institutional, not political, so they can be solved only through reforms to the regulatory process.

“Regulation 360” proposes fundamental reforms to that process.

It starts with regulation by legislation and moves through rulemaking by agencies, retrospective review, and regulatory budgeting. Then it loops back to regulation by legislation, beginning the process over again. As this 360-degree process continues, the quality and effectiveness of regulation will improve, government will increase its effectiveness in general, and people’s lives will be improved.

Go Deeper, Read More

Regulation by Legislation

- Jason J. Fichtner, Patrick A. McLaughlin, and Adam N. Michel, “Legislative Impact Accounting: Rethinking How to Account for Policies’ Economic Costs in the Federal Budget Process,” Public Budgeting & Finance (forthcoming), http://onlinelibrary.wiley.com/doi/10.1111/pbaf.12187/abstract.

- Hester Peirce and James W. Broughel, Dodd-Frank: What It Does and Why It’s Flawed (Arlington, VA: Mercatus Center at George Mason University, 2012).

Rulemaking by Agencies

- Patrick A. McLaughlin, Jerry Ellig, and Michael Wilt, “Comprehensive Regulatory Reform” (Mercatus Policy Primer, Mercatus Center at George Mason University, Arlington, VA, 2017).

- Jerry Ellig, “Ten Principles for Better Regulation” (Mercatus Research, Mercatus Center at George Mason University, Arlington, VA, 2013).

- John F. Morrall and James W. Broughel, “The Role of Regulatory Impact Analysis in Federal Rulemaking” (Mercatus Research, Mercatus Center at George Mason University, Arlington, VA, 2014).

- Jerry Ellig, “Evaluating the Quality and Use of Regulatory Impact Analysis: The Mercatus Center’s Regulatory Report Card, 2008–2013” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2016).

- Richard Williams and James W. Broughel, “Principles for Analyzing Distribution in Regulatory Impact Analysis” (Mercatus on Policy, Mercatus Center at George Mason University, Arlington, VA, 2015).

- Reeve Bull and Jerry Ellig, “Judicial Review of Regulatory Impact Analysis: Why Not the Best?” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2017).

- C. Boyden Gray, “The President’s Constitutional Power to Order Cost-Benefit Analysis and Centralized Review of Independent Agency Rulemaking” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2017).

- James W. Broughel and Patrick A. McLaughlin, “Principles for Constructing a State Economic Analysis Unit” (Mercatus Policy Primer, Mercatus Center at George Mason University, Arlington, VA, 2018).

Retrospective Review

- Patrick A. McLaughlin and Richard Williams, “The Consequences of Regulatory Accumulation and a Proposed Solution” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2014).

- Randall Lutter, “Regulatory Policy: What Role for Retrospective Analysis and Review?,” Journal of Benefit-Cost Analysis 4, no. 1 (2013): 17–38.

- Randall Lutter, “How Well Do Federal Regulations Actually Work? The Role of Retrospective Review” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2012).

- Jerry Ellig, “Why and How Independent Agencies Should Conduct Regulatory Impact Analyses” (Mercatus Working Paper, Mercatus Center at George Mason University, Arlington, VA, 2018).

Regulatory Budgeting

- Patrick A. McLaughlin, “Regulatory Budgeting as a Solution to the Accumulation of Regulatory Errors” (Testimony before the House Committee on Budget, Mercatus Center at George Mason University, Arlington, VA, 2016).

- Laura Jones, “Cutting Red Tape in Canada: A Regulatory Reform Model for the United States?” (Mercatus Research, Mercatus Center at George Mason University, Arlington, VA, 2015).

- Fichtner, McLaughlin, and Michel, “Legislative Impact Accounting.”