- | Regulation Regulation

- | Policy Briefs Policy Briefs

- |

The Social Discount Rate: A Primer for Policymakers

The social discount rate used in cost-benefit analysis (CBA) is an interest rate applied to benefits and costs that are expected to occur in the future in order to convert them into a present value. This conversion is done to ascertain what those benefits and costs are worth today. The social discount rate is widely considered to be one of the most important inputs in CBA in that small changes in this rate can result in large swings in present-value calculations, thereby having a major influence on whether a project passes or fails a cost-benefit test. However, the social discount rate is widely misunderstood for a variety of reasons. This primer explains the basic conceptual issues involved with the social discount rate and tries to clear up some common misunderstandings.

Basic Concepts

The two core discounting concepts in CBA are the “consumption rate of interest” and the “investment rate of interest.” The investment rate of interest accounts for the marginal social rate of return to capital in the economy. The intuition behind this rate is that investments earn positive, compounding rates of return. The consumption rate of interest, meanwhile, represents the rate at which a unit of consumption in the present is traded for a unit of consumption in the future. This interest rate reflects consumers’ time preferences and, in certain circumstances, may be represented by the risk-free market interest rate. The standard approaches to discounting in CBA all rely on these two interest rate concepts. For the sake of clarity, when this article refers to “the social discount rate” in CBA, it is the consumption rate of interest for all of society that is being referenced.

The investment rate of interest will generally be higher than observable market interest rates (and by extension the consumption rate) because the minimum required rate of return demanded by businesses will tend to exceed their costs of borrowing, owing to taxes. If the expected after-tax rate of return on a project falls below businesses’ cost of borrowing, they will not undertake certain investments that might still be profitable from a societal point of view. In this way, taxes create allocative distortions in the economy that limit the amount of overall investment.

The risk-free market interest rate can deviate from the natural rate that reflects consumer time preferences, owing to factors such as inflation or market inefficiencies (e.g., externalities). Small adjustments can be made in an analysis to account for such factors. However, discounting consumption in CBA also becomes much more complicated in an intergenerational context, because while all human beings exhibit some degree of time preference, they only exhibit positive time preference during the time they are alive. No one is impatiently waiting to be born. So while there is a potential case to be made on positive grounds for discounting consumption for policies that only have impacts within a lifetime or perhaps a within a generation, it does not follow that this rationale extends to policies with intergenerational consequences. Most often, how much value society should place on consumption in the future is an ethical question.

The Power of Compound Interest

The consumption and investment rates of interest are different from a discount rate used in financial analysis in that they are applied to real resources, which are distinct from financial resources. The consumption rate of interest is used to discount resources that are consumed, and the investment rate of interest applies to resources that are invested. Any interest rate, be it applied to money or anything else, is important owing to the power of compound interest.

Tables 1 and 2 demonstrate the influence small changes in the discount rate have on present-value calculations. As is evident from table 1, an investment paying $1 million in 100 years is worth just $72.45 in present-value terms at a 10 percent discount rate, $1,152.45 at a 7 percent rate, and $52,032.84 at a 3 percent rate.

On the one hand, there is the observable fact that people tend to exhibit positive time preference. That is, they prefer consumption sooner rather than later. However, as discussed earlier, this provides little justification for discounting benefits and costs to those not yet born. Common arguments for using a positive social discount rate in an intergenerational context are that people in the future will be richer than those in the present, so, owing to the phenomenon of diminishing marginal utility, a unit of consumption—including a life—can be expected to generate less utility to future citizens than to present citizens. Or sometimes it is simply stated that the well-being of people in future should be discounted at compounding exponential rates since future utility matters less than present utility.

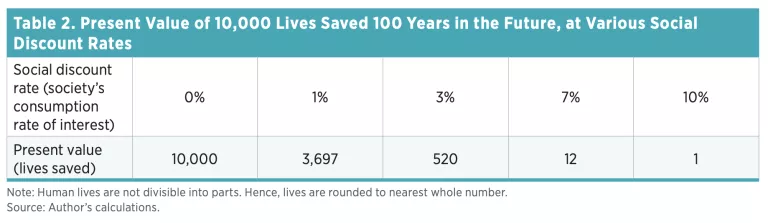

Table 2 highlights the importance of the discounting when comparing lives saved in the future to an equivalent number of lives saved in the present. For example, 10,000 lives saved in 100 years are worth 198 lives in the present at a 3 percent social discount rate and worth just 1 life using a 10 percent social discount rate.

When to Use Each Rate

When conducting a CBA, one must be careful to use appropriate rates in their appropriate contexts. Nonpecuniary aspects of life cannot be invested in an account, so they should never be treated as if they will compound in value at the marginal rate of return to capital. At the same time, returns to capital often can be reinvested, so it is entirely appropriate to treat capital investments as if their returns compound in value at the investment rate.

Guidelines from the federal government conflate these two discounting concepts by recommending that regulatory agencies apply a single social discount rate to all benefits and costs, irrespective of whether those benefits and costs are like capital investments or like consumption. This is a problem because it means analysts are essentially treating all benefits and costs as if they are either consumption or investment, when rarely is this the case. Treating consumption and investment equally gives too much weight to consumption relative to a comparable amount of investment because, in general, one dollar of investment is more valuable to society than one dollar of consumption.

The way to resolve this issue is to use the two different rates in their different contexts, which means separating consumption and investment in the analysis. Positive and negative incremental investment can be kept on one side of the ledger (out of convention this is often the cost side), and consumption can be kept on the other side of the ledger (the benefits side). Then the two different interest rates can be applied distinctly to their respective benefits or costs.

Some Misconceptions about Social Discounting

Misconception #1: Analysts Are Discounting Money Rather Than Lives

Some commenters argue what is being discounting in CBA is money rather than lives saved. This confusion arises because benefits and costs are valued in monetary terms in order to compare them to one another. The undiscounted dollar values in CBA refer to monetary equivalents; i.e., the value individuals place on certain resources in terms of what they are willing to spend for them. Using such a valuation technique does not convert those resources into something that can be invested, like money. Dollars are simply a convenient measuring stick to make comparisons in value.

Consider, for example, the similar practice of adjusting the value of resources for inflation when they occur in different years (which also occurs in CBA). After an inflation adjustment, resources have a dollar value assigned to them, but those dollars actually represent bundles of real resources, hence the use of the term “real” when referring to inflation-adjusted values. Lives are not literally being converted into money when they are expressed as monetary equivalents in CBA. Real resources are ultimately what is being valued.

Misconception #2: The Opportunity Cost of Capital Is the Basis for Social Discounting

Other observers assert that a social discount rate is necessary in CBA because of the opportunity cost of capital; i.e., because capital earns a rate of return in the future. For example, government guidelines recommend regulatory agencies use a 7 percent social discount rate that “approximates the opportunity cost of capital.”

Capital’s rate of return cannot be the basis for social discounting, however, because the rate at which individuals discount future consumption shapes household savings patterns and by extension determines capital’s rate of return. Basing the social discount rate on the opportunity cost of capital rate involves circular reasoning. Moreover, an optimum is achieved when capital investment is increased to such an extent that the investment rate of interest falls to meet the social discount rate. At this point, the additional utility generated from an incremental unit of capital investment is zero, which, again, provides no particular basis for social discounting.

Misconception #3: Only Regulatory Benefits Have Intergenerational Consequences

Social discounting often comes up in the context of climate change policy or other environmental contexts such as nuclear waste disposal, where society has to wait a long time for the benefits of a government regulation to pay off. This can create an impression that the social discount rate matters most for environmental projects or only for projects with nonpecuniary benefits far in the future. In fact, costs often have intergenerational consequences as well, though these costs often go unaccounted for in analysis. Even small amounts of investment displaced by government projects today can have significant long-acting consequences, owing to the power of compound interest.

Moreover, people are continually being born and dying, so what constitutes a “generation” may in fact be a relatively short period of time. While deciding how much weight to give to the consumption of future generations is based on a value judgment, a commitment to assessing the benefits and costs of policy as they actually occur requires acknowledgment of the impacts of policies through this investment channel.

A Note about Declining Discount Rates

Some economists have suggested that, owing to uncertainty, the government should consider using a social discount rate that declines over time. There are two rationales for declining discount rates that do not involve any suboptimal, or irrational, decision-making. One rationale takes the perspective of a social planner that centrally plans the economy. The discount rate of the social planner may decline over the investment horizon owing to the combination of the social planner being risk averse and there being fluctuations in and uncertainty about the rate of economic growth in the future.

A second rationale for declining discount rates is called the Expected Net Present Value approach, and it asserts that in the presence of uncertainty, a declining discount rate is equivalent to a constant rate under certainty. Consider the possibility that there is a 50 percent chance that the social discount rate is 3 percent and a 50 percent chance that it is 7 percent. To account for this uncertainty, one could calculate the present value of the project at 3 percent, then at 7 percent, and then obtain the expected value; i.e., the average of these present values. It turns out that the implied certainty-equivalent discount rate consistent with this average present value is lower than 5 percent, the average of the two social discount rates. Furthermore, as the time horizon extends into the future, this implied discount rate gets closer and closer to 3 percent, the low end of possible discount rates. Therefore, accounting for uncertainty can entail use of a declining discount rate that is equivalent to a constant rate under certainty.

The first argument for declining discount rates, based on the preferences of a social planner, is explicitly normative. Whether to adopt this method or not is a value judgment because this rationale depends on ethical choices about the social planner’s welfare function. The second argument is more compelling because it is simply a mathematical property that follows from taking the expected value of a function, although aspects of this argument are normative as well.

In either case, however, if an analyst uses a declining social discount rate owing to uncertainty, he or she must also adjust the estimation of the opportunity cost of capital over time in the analysis, since it will vary with the social discount rate. In general, a lower social discount rate means a higher estimated opportunity cost of capital and vice versa, which is why low and declining discount rates need not encourage more regulation. If the opportunity cost of capital is accounted for in analysis, regulatory costs can be very large when the social discount rate is low or declining. However, these costs often go overlooked, leading to the common view that a low social discount rate encourages more regulation.

Conclusion

This primer has sought to provide some clarity on the topic of the social discount rate and to clear up common misconceptions about this rate. Misunderstandings often stem from conflating the two main discounting concepts: the consumption and investment rates of interest. Indeed, even government guidelines on regulatory analysis seem to make, or at least encourage, such mistakes.

Moreover, some aspects of discounting are inherently normative; that is, they involve value judgments. Analysts should always be clear about what aspects of their analysis involve value judgments. For example, if the preferences of a hypothetical social planner are important determinants of present-value calculations, this fact should be made transparent in the analysis. Furthermore, the opportunity cost of capital should always be accounted for in any analysis, and analysts should understand that estimates of the opportunity cost of capital will tend to vary with the social discount rate used, rather than the other way around.

Adhering to these basic principles could potentially resolve many common problems found in modern CBA.