- | Policy Briefs Policy Briefs

- |

On Borrowed Time: How Occupational Licensing Affects Student Loan Debt

Rapidly increasing student loan debt has become a major policy issue in many countries over the past several decades. In the United States, student loan debt expanded from $0.2 trillion in 2003 to $1.5 trillion in 2020. Student loan debt is the second-largest category of household debt, following mortgage debt, and is the largest category of delinquent household debt in the United States. At the micro level, about two-thirds of recent college graduates finance their college education with student loans. Although a significant amount of time and attention has been devoted to the issue, the possible connection between occupational licensing and rising student loan debt remains largely unexplored.

Occupational licensing has significantly expanded over the past several decades. Also, licensing requirements for many occupations include requirements of undergraduate or graduate education. Licensing creates an entry barrier and allows professionals an opportunity to generate monopoly rents, the so-called licensing premium. These rents are not confined to occupations requiring a college degree; studies have found evidence that occupational licensing is associated with higher earnings in several occupations for which licensing does not require a college degree. Over time, education requirements for licensed occupations have gradually increased. It is worth considering the association between occupational licensing, borrowing, and student loan debt.

Our analysis uses the 2017 National Survey of College Graduates (NSCG), which provides individual-level microdata on licensing status and college financing.

Our primary findings are the following:

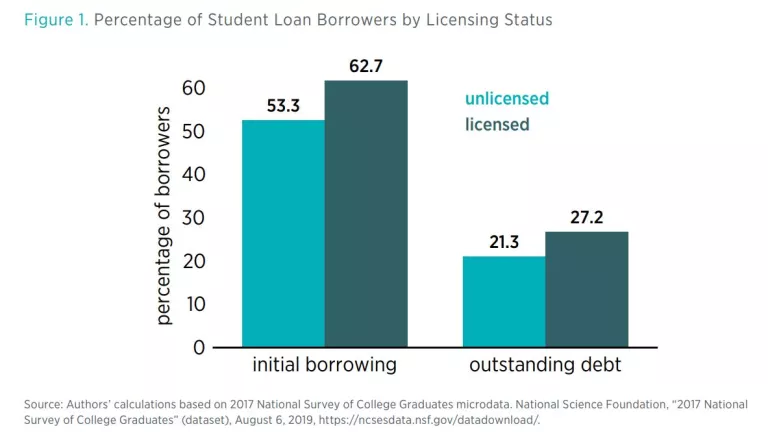

- Licensed workers are almost 10 percentage points more likely to have borrowed for their college education and almost 6 percentage points more likely to have outstanding student loan debt than unlicensed workers.

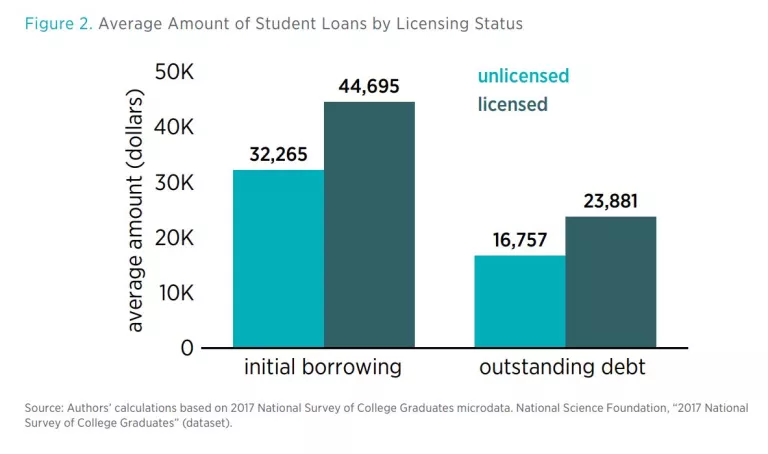

- Among student loan borrowers, licensed graduates borrow about $12,000 (or 38.5 percent) more and have student loan debt balances about $7,000 (or 42.5 percent) more than unlicensed graduates.

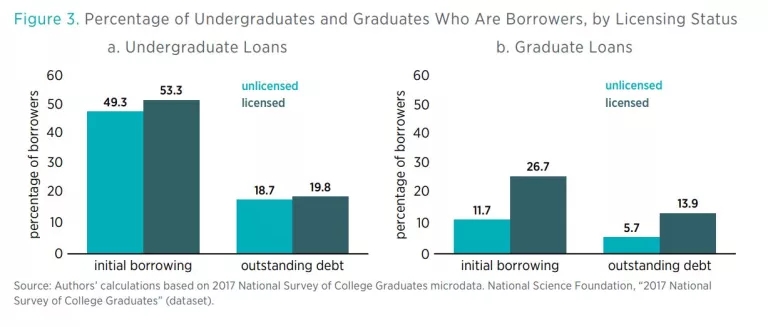

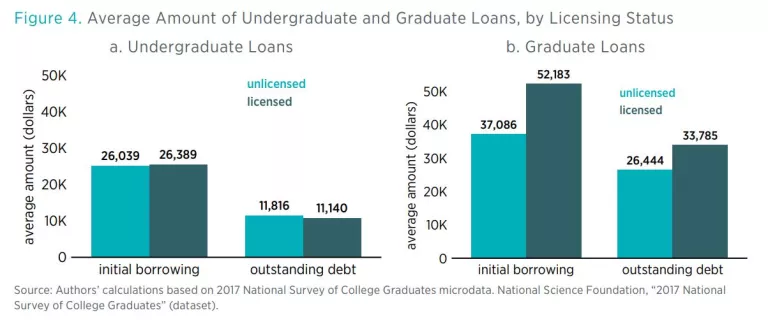

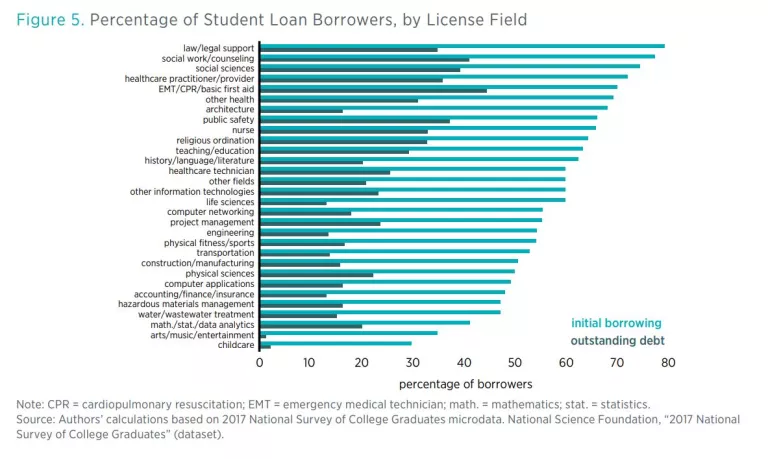

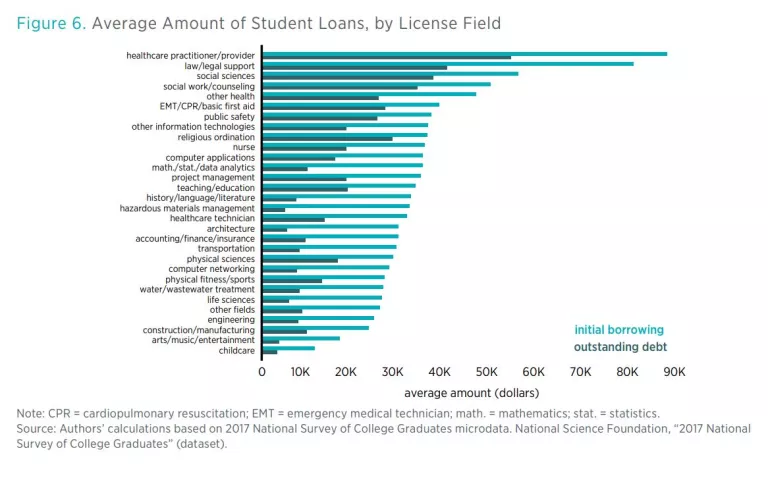

- The differences in student loan borrowing and outstanding debt between licensed and unlicensed graduates are mostly attributable to licensed individuals who have obtained postgraduate education, such as healthcare practitioners and lawyers.

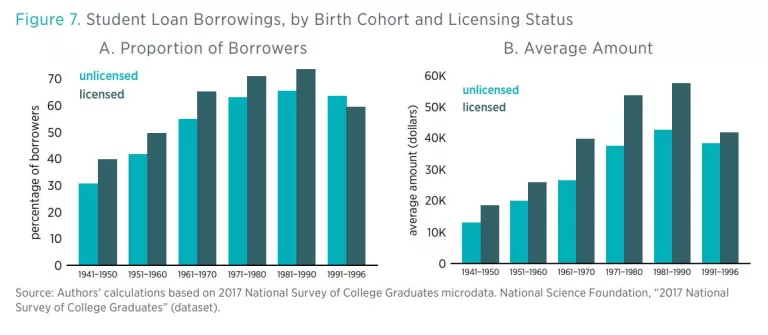

- There is some evidence that the gap in student loan borrowing between licensed and unlicensed individuals has gradually expanded over time.

Our comparison suggests that licensed workers may bear more up-front financing costs than unlicensed workers in the era of fast-growing student loans across the country. Specifically, licensed workers in low-paying jobs may suffer most among all licensed workers. Furthermore, monopoly rents created by licensing regulation may benefit higher education institutions as well as licensees. In this case, licensing reform may help mitigate soaring student loan borrowing and debt and remove additional financial burdens on licensed individuals.

Data and Methodology

We use the NSCG microdata found in public use data files for the analysis. The NSCG is a nationally representative survey of four-year college graduates in the United States. It is a unique survey that provides rich information on both individual licensing status and college financing. The survey data also include detailed information on degrees, licenses, and demographics. Our study sample comprises all individuals who responded to the 2017 NSCG. All descriptive statistics are weighted by survey weights.

We define a licensed individual as a person who had a currently active professional license or certificate as of the survey reference date. In the 2017 NSCG, the question used to identify these individuals is A39: “As of February 1, 2017, did you have a currently active professional certification or a state or industry license?” Any respondent who answers, “Yes,” is considered a licensed individual in our study. As a result, our analysis is unable to fully distinguish licensing from certification. To work around this limitation, our analysis also examines borrowing and outstanding debt for those in licensed occupational fields.

We measure the amount of initial student loan borrowings and outstanding debt using self-reported data. The 2017 NSCG includes question D13: “The next question asks about the TOTAL amount you have borrowed to finance undergraduate and graduate degrees you completed before February 1, 2017, and how much you still owed as of February 1, 2017.” Respondents are asked to sort themselves into 1 of 11 bins: $0, $1–$10,000, $10,001–$20,000, and so on through $80,001–$90,000, or $90,001 or more. We approximate each bin to the midpoint value. Then we calculate the total amount borrowed for undergraduate and graduate degrees, and we calculate the total outstanding debt for both undergraduate and graduate degrees.

Results

Individual licensing status is positively associated with initial student loan borrowing and outstanding debt. Figure 1 compares the percentage of student loan borrowers with occupational licenses with those without occupational licenses. Licensed individuals are more likely than unlicensed individuals to have borrowed to finance higher education. Of licensed individuals, 62.7 percent have student loans, whereas 53.3 percent of unlicensed individuals do. This disparity also occurs with outstanding debt: 27.2 percent of licensed individuals have student loan debt, whereas 21.3 percent of unlicensed individuals do. The gap in student loan debt between licensed and unlicensed individuals is smaller than the gap in initial borrowing. This difference may be attributed to licensed individuals having a higher ability to repay their student loans (because of, for example, higher wages) after graduation than unlicensed individuals.

Conclusion

Our analysis suggests that occupational licensing is positively associated with student loan borrowing and debt. The difference is mainly attributable to occupational licenses that require graduate education. There are also large variations in student loan borrowing and the ability to repay student loans across different licensed fields. The positive relationship between licensing status and student loans has existed for a long time and also appears to have grown.

Our findings have several policy implications. Researchers and policymakers need to further consider the long-term consequences of student loan debt that occupational licensing imposes on aspiring workers. Previous literature has focused on the licensing wage premium and other labor market consequences but has not examined education expenses. Effectively, licensing may result in a transfer of some of the licensing wage premium from licensed workers to colleges and universities. If increases in educational expenses for licensing merely limit entry to the licensed occupation without a sufficient increase in productivity, they may add financial burdens to licensed individuals. In fact, recent research suggests that scaling back occupational licensing will lead to productivity gains of as much as 2.5 percent. Rather than addressing the problem with temporary solutions such as student loan forgiveness, which may create a moral hazard of individuals taking on more debt—a vicious cycle—policymakers should consider shifting their focus to the root cause. Licensing reform may help mitigate an increase in educational expenses and student loans as well as relax extra burdens to licensed individuals.