- | Financial Markets Financial Markets

- | Public Interest Comments Public Interest Comments

- |

Ending Too-Big-to-Fail May Require More Than the Minneapolis Fed Too-Big-to-Fail Plan

The too-big-to-fail problem has been a long time in the making, and regulator discretion to date has not been successful at eliminating the problem.

Thank you for the opportunity to comment on the Minneapolis Plan to End Too Big to Fail. A key aim at the Mercatus Center at George Mason University is to bridge the gap between academic ideas and real-world problems and to advance knowledge about the effects of regulation on the economy. My comments are my own and do not reflect those of any affected party or special interest group, but rather reflect my general concerns about some of the policy prescriptions, as well as the methodology used to justify the results.

General Comments

Broadly speaking, the push for higher capital found in the Minneapolis Plan to End Too Big to Fail (Minneapolis Fed Plan) makes sense. However, before addressing some of the questions posed in the request for comment, I would like to share several concerns I have about the proposal.

First, the too-big-to-fail problem has been a long time in the making, and regulator discretion to date has not been successful at eliminating the problem. A recent historical study compares costs of US banking crises since the National Bank Act of 1864. From 1865 until the Federal Reserve Act of 1913, the total cost of all bank insolvencies was only about $1 billion in 2009 dollars, which was comparable to the costs calculated for the “free banking” period from 1838 to 1860. During that period, most banks were liquidated before they could fail, because shareholders were subject to contingent liability, such as double, triple, or even unlimited liability. After the Federal Reserve Act of 1913, discount window lending offset shareholder incentives to liquidate a troubled bank early, which had the effect of raising the costs of crises. According to one estimate cited in the study, the cost of the Great Depression from 1929 to 1933 escalated to about $39 billion in 2009 dollars. With the introduction of federal deposit insurance in 1934, contingent liability was thought to be unnecessary, and while crises have been less frequent, the costs have continued to escalate. The Savings and Loan Crisis, which occurred from 1986 to 1995, cost about $200 billion in 2009 dollars. For comparison, the study estimates that the most recent crisis may have cost no less than $1.7 trillion in 2009 dollars, which may be a low estimate. Therefore, eliminating too-big-to-fail may require replacing regulator discretion with market discipline. The Minneapolis Fed Plan, however, makes no explicit mention of market discipline.

Second, steps 1 and 2 of the Minneapolis Fed Plan focus on bank holding company size rather than banking activity. A recent study, however, suggests that securitization-active bank holding companies held the most AAA-, AA-, and A-rated private label securitization tranches, including structured finance collateralized debt obligation (CDO) tranches, which experienced the greatest distress during the crisis. In a forthcoming working paper, I show that the largest securitizing banks on average had the greatest exposure to private label securitization tranches that experienced distress during the crisis. This means a key issue that arose during the most recent crisis was why financial holding companies created (and held) so many of the products that ultimately went bust.

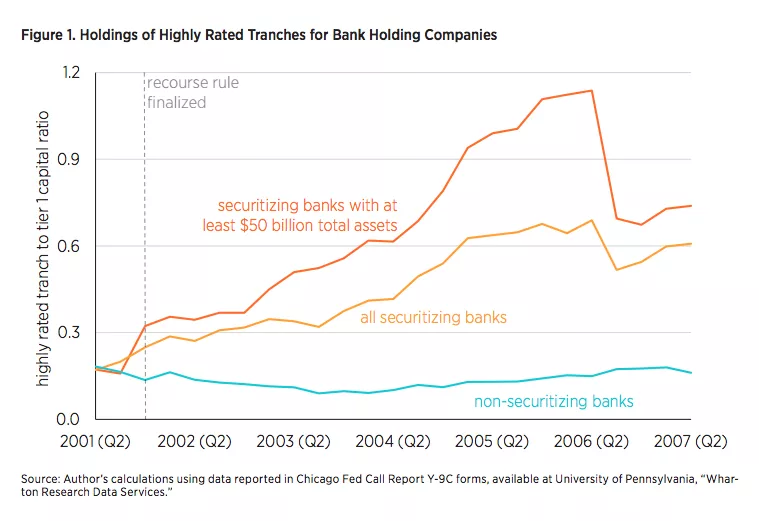

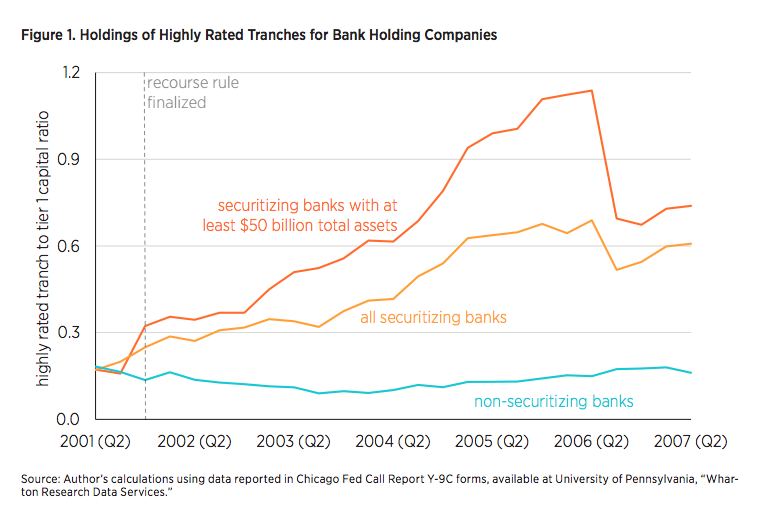

Related to this point, figure 1 shows why bank activity is important. The red line in the figure depicts estimates of average holdings of highly rated tranches relative to tier 1 capital for securitizing bank holding companies with at least $50 billion in total assets, a cutoff identified by the Dodd-Frank Wall Street Reform and Consumer Protection Act (Pub. L. No. 111-203; 124 Stat. 1376) as signifying systemic importance. The orange line depicts estimates for all securitizing bank holding companies. Finally, the blue line depicts estimates for non-securitizing bank holding companies. The figure shows that securitizing holding companies increased their highly rated tranche holdings relative to tier 1 capital throughout the sample until Q3 2006. For holding companies with at least $50 billion in total assets, average holdings of highly rated tranches exceeded tier 1 capital by Q4 2005, as the ratio exceeds one. The size of the highly rated tranche holdings relative to tier 1 capital can help explain why, once the highly rated tranche values began to decline, these holding companies faced insolvency risk.

Related to this, steps 1 and 2 of the Minneapolis Fed Plan still make use of risk weighting, which may distort bank portfolio allocations. For instance, the vertical line highlighting Q4 2001 in figure 1 shows how securitizing bank holding companies on average tended to increase their purchases of the highly rated tranches, after the Federal Reserve, Federal Deposit Insurance Corporation (FDIC) and Office of the Comptroller of the Currency finalized the Recourse, Direct Credit Substitutes and Residual Interests Final Rule, or Recourse Rule in late 2001. The Recourse Rule could have distorted bank portfolio allocations by lowering risk-weights for the highest-rated tranches and increased the risk-weights for the below-investment-grade tranches. The Recourse Rule, accordingly, was intended to encourage securitization without encouraging ex ante risk-taking. Yet, an unintended outcome may have been that it encouraged both securitization and ex post risk-taking, as securitizing holding companies increased their holdings of the highest-rated products they created, which subsequently experienced significant writedowns.

Third, steps 1 and 2 of the Minneapolis Fed Plan aim to have well-capitalized holding companies rather than banking subsidiaries. However, capital requirements may be more effective at the banking subsidiary level; therefore, it may be good to acknowledge this facet of capital adequacy.

Fourth, using capital to back assets may not be the most effective way to establish capital adequacy. In a Modigliani–Miller world, bank assets and liabilities should be decoupled. While Modigliani and Miller may describe a hypothetical world, to the extent that DeYoung and Yom have shown that assets and liabilities may be statistically speaking independent, although less so for large banks, that suggests we may not be far from that ideal world. In that case, it would seem to make more sense to use capital to back liabilities, such as deposits, rather than assets. This was initially the case when the Federal Deposit Insurance Corporation first came into being as it called for banks to have at least 10 percent capital to back deposits. With these preliminary concerns in mind, I will now address a few of the questions posed in the request for comment.

Comments on the Benefit and Cost Analysis of The Higher Minimum Equity Requirement

The approach used to calculate costs of a higher minimum equity requirement seems reasonable. My primary criticism with step 1 of the Minneapolis Fed Plan concerns the use of cross-country data from the International Monetary Fund’s (IMF) database from 1970 to 2011 to estimate benefits. This may make sense for international organizations, like the IMF or the Bank of International Settlements, which have a dialogue with a wide variety of clients, but it does not make sense for US policymakers to apply this approach to the United States.

The Minneapolis Fed Plan uses a discount rate of 5 percent, assumes that the United States experiences the median cost of a crisis relative to precrisis GDP reported in the Basel Committee on Banking Supervision (BCBS) 2010 study equal to 7.5 percent, and assumes that crises have only permanent effects. These assumptions translate into a present-value cumulative cost of a crisis equal to 158 percent of GDP. A forthcoming working paper finds that over the 1892–2014 period, the cost of a crisis relative to precrisis GDP in the United States equals only 4.5 percent of GDP, which in present-value terms would significantly reduce the cumulative cost of a crisis to only 94 percent of GDP. In sum, simply assuming that crises have only permanent effects may be reasonable, but relying on data from other countries to determine the present-value effects of a crisis in the United States does not makes sense. The benefits of higher capital should at least reflect alternative assumptions about the costs of a crisis, based on US historical data.

Lastly, based on my earlier comments, a minimum equity capital requirement may be improved if it is (1) defined simply as a leverage ratio instead of a risk-based standard, (2) based on liabilities rather than assets, and (3) applied to the banking subsidiary rather than the holding company. In addition, given that book values do not respond well to changes in market conditions, the use of market value may be preferred.

Comments on Benefit and Cost Analysis of a “Systemic Risk Capital Charge”

Given my reservations, expressed earlier, about defining systemically important financial institutions merely based on holding company size, simple size-based capital charges will serve at best as a blunt instrument in attempting to end too-big-to-fail. This approach may be especially problematic if the Minneapolis Fed Plan does not explicitly address the lack of market discipline that has characterized the practice of bank supervision since the establishment of the Fed.

Comments on Right Sizing Community Bank Supervision and Regulation

More complicated regulatory regimes are likely to generate regulatory arbitrage opportunities, from which larger banks are in a better position to benefit. Therefore, a better way to address the “right sizing” issue is to have a simpler, higher-leverage ratio, applied to most if not all banks. For instance, the recent study mentioned above finds that the benefits of increasing the leverage ratio to 15 percent for banks with at least $1 billion in assets tend to exceed the costs.

Overall, the Minneapolis Fed Plan to End Too Big to Fail is a step in the right direction. Still, a simpler plan that focuses on the US experience only, rather than results from cross-country studies, and that addresses the lack of market discipline in bank regulation, may be more effective.

Additional details

Proposed Plan on Ending Too Big to Fail

Agency: Federal Reserve Bank of Minneapolis

Proposed: November 16, 2016

Comment period closes: January 17, 2017

Submitted: January 17, 2017

{kind=link}