- | Housing Housing

- | Policy Briefs Policy Briefs

- |

Analyzing the Unfunded Pension Risk of Local Governments

As local governments have entered the COVD-19 crisis, they have faced varying cost burdens from previously promised employee retirement obligations. During the Great Recession, pension obligations played a role in the bankruptcy filings by Central Falls, Rhode Island, and by Prichard, Alabama. In this policy brief, I seek to determine whether pension costs might force more communities into insolvency during the COVID-19 recession.

I obtained fiscal year (FY) 2019 audited financial statements filed by 5,698 local governments, of which about 1,005 have single-employer pension systems. From each statement I collected net pension liability and government-wide revenue data.

Some governments report net pension assets, while others report both net pension assets and net pension liabilities. A net pension asset arises when the government’s fiduciary net position (FNP) exceeds its total pension liability (TPL) for one or more plans. The same government may also have plans in which TPL exceeds FNP, creating a net pension liability as well. For this analysis I treat net pension assets as a negative net pension liability, netting assets against liabilities when both are reported.

The absolute size of a government’s net pension liability is not a good indicator of pension cost pressures because local governments vary greatly in size. The liability should be adjusted to reflect the size of the governmental unit. One possibility is to divide the liability by the jurisdiction’s population to derive a per capita debt level.

I use a different method: dividing the liability by total revenue. This procedure is somewhat more precise because it considers the varying abilities of local governments to raise revenue from a given population.

That said, a pension liability-to-revenue ratio is also an imperfect measure of pension cost burdens. As I will show later, net pension liabilities are calculated using different discount rates across systems. But the ratio is relatively simple to compute and allows a rough comparison across a large number of governments.

The net pension liability-to-revenue ratios calculated from FY 2019 financial statements ranged from a maximum of +336 percent to a minimum of −269 percent (reflecting a relatively large net pension asset position). The median ratio was 10 percent. Included in the sample are 1,692 local governments that had zero reported net pension liabilities, most likely owing to the absence of a defined benefit pension plan.

All local governments in my sample with net pension liability-to-revenue ratios greater than 200 percent are in Illinois, Michigan, West Virginia, and Puerto Rico. High-pension-burden municipalities (there were no counties with these high ratios) in the three states have single-employer plans; Puerto Rico municipios (municipalities) participate in the commonwealth’s Employee Retirement System, which has exhausted its assets.

In the rest of the brief I will consider local governments with extreme pension liability-to-revenue ratios in Illinois, Michigan, and West Virginia.

Riverdale, Illinois, and Other Chicago Suburbs

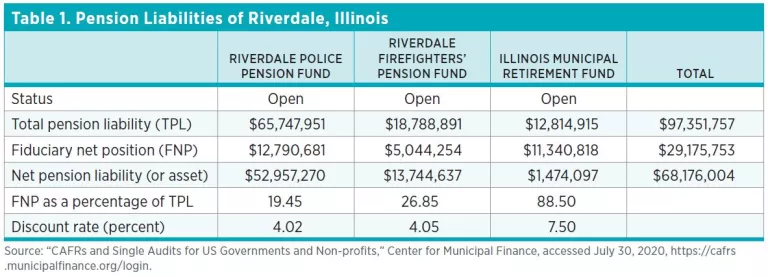

The local government reporting the highest net pension liability as a percentage of revenue in the sample is Riverdale, a southern suburb of Chicago. Aggregate net pension liabilities across the village’s three pension funds amount to 336 percent of government-wide revenues. Table 1 shows the breakdown of these liabilities (totals vary slightly from the aggregate net pension liabilities reported elsewhere in Riverdale’s financial statements).

Funded ratios calculated by actuaries often differ from the plan fiduciary net position as a percentage of total pension liability shown in table 1 and in similar tables later in this brief. Although both percentages address the same objective—that is, comparing a fund’s assets to the present value of its payment obligations—they may be computed from different assumptions. The ratios reported on local government comprehensive annual financial reports (CAFRs) must be calculated according to rules set by the Governmental Accounting Standards Board (GASB), while funded ratios reported by actuaries and data collectors such as IDOI do not face this same requirement.

In the case of Riverdale, IDOI reports funded ratios of 31 percent and 44 percent for the police and firefighters’ plans, respectively—much higher than the percentages given earlier. The main source of the difference is the discount rate applied to future benefit payments. To calculate its funded ratios, IDOI discounts plan liabilities by the assumed rate of return on plan assets, which was 6.25 percent for the police fund and 5.75 percent for the firefighters’ fund. The CAFR used “blended” discount rates of 4.02 percent and 4.05 percent, respectively, for the two plans (blended discount rates are explained in the next section). GASB rules also call for the fund’s assets (or FNP) to be reported at market value, whereas the IDOI funded ratios use an actuarially smoothed value under which recent gains and losses are only gradually incorporated.

One reason for Riverdale’s public safety plans’ low levels of funding is the village’s failure to make actuarially determined pension contributions each year. In FY 2019, Riverdale contributed $738,794 to the police plan, far less than the $2,015,052 determined by system actuaries. For the firefighters’ plan, actual contributions of $165,117 were a small fraction of the actuarially determined amount of $743,750.

Riverdale has been and will continue to be challenged to make full pension contributions because of weak revenues. Government-wide revenue in 2019 was virtually identical to 2013 and 2014 levels. High rates of property tax delinquencies are limiting village revenues. Riverdale’s mayor, Lawrence Jackson, recently told the Chicago Tribune that only 68 percent of Riverdale’s property tax levy was being collected. Delinquencies may increase further during the COVID-19 pandemic because Cook County has indefinitely postponed auctions of properties with unpaid taxes.

Several other Chicago suburbs have net pension liability-to-revenue ratios greater than 200 percent. These include Calumet City, Forest Park, Forest View, North Chicago, Stone Park, Waukegan, and Worth.

Charleston and Other West Virginia Cities

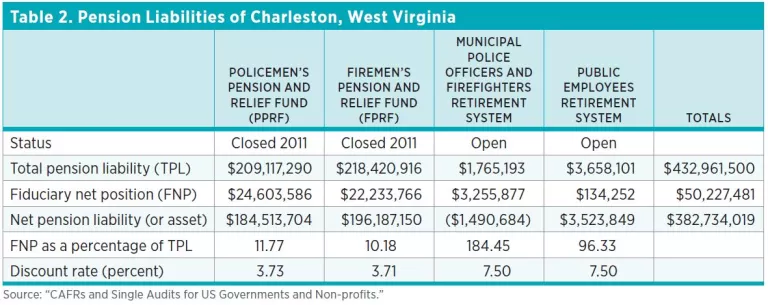

Charleston, West Virginia, reported the second-highest net pension liability as a percentage of government-wide revenues in the sample. The city’s 2019 net pension liability of $382,734,019 was 315 percent of total revenues, which amounted to $121,444,386.

Most of Charleston’s pension debt belongs to a pair of single-employer public safety plans that were closed to new employees in 2011. Table 2 shows key metrics for these two legacy plans, as well as the state plans in which Charleston participates.

During the Great Recession, multiple West Virginia cities encountered difficulties funding their police and firefighters’ pension systems, and they asked for state intervention. In response, the state legislature passed and then-governor Joe Manchin signed Senate Bill 4007 in late 2009. The bill created the West Virginia Municipal Pensions Oversight Board to oversee 53 municipal police and firefighters’ retirement systems. The board educates local plan trustees, prepares actuarial valuation reports, and reviews medical examinations of police and firefighters seeking disability pensions.

Senate Bill 4007 also increased West Virginia’s insurance premium tax by 1 percent, earmarking the proceeds for additional contributions to various pension funds in West Virginia, including the local police and firefighters’ systems. In the 2019 fiscal year, Charleston’s two public safety plans received $3,530,843 from the insurance surtax.

Finally, the bill gave cities the option to close their single-employer plans and enroll new hires in a statewide plan—the Municipal Police Officers and Firefighters Retirement System (MPFRS). Charleston was among the cities that took this option. Because MPFRS is over 100 percent funded, Charleston’s exposure to the system is a net pension asset that slightly offsets the city’s large liabilities.

The law requires closed plans to adopt a conservation funding method under which contributions and assets are divided into two accounts. The Benefit Payment Account uses all employer contributions as well as a portion of employee contributions and state insurance premium tax proceeds to make pay-as-you-go payments to beneficiaries. Remaining employee contributions, insurance surtax revenues, and investment income are added to the Accumulation Account, which will only be used to pay benefits when it achieves full funding.

With the injection of state tax proceeds, actuaries project that full funding will be achieved in 2045. This projection is likely to be achieved because it relies on a relatively conservative assumed rate of return. As mentioned above, plan assets are projected to grow at a rate of 4.5 percent. This is well below the 7.11 percent average used by large, state-sponsored pension plans. Relative to state pension systems, Charleston’s conservation retirement plans have conservative investment portfolios: about 60 percent of funds are invested in US equities, with smaller amounts allocated to US corporate bonds, Treasury securities, and short-term investments. No funds are deployed to foreign securities or alternative investments such as private equity.

Other West Virginia cities that have single-employer public safety retirement systems have heavy pension debt burdens. Aside from Charleston, West Virginia municipalities with net pension liability-to-revenue ratios exceeding 100 percent include Beckley, Bluefield, Clarksburg, Fairmont, Huntington, Martinsburg, Morgantown, Parkersburg, and Weirton.

Some of these cities have kept their single-employer systems open. One West Virginia municipality that continues to accept new members into its public safety pension plans is Martinsburg, whose net pension liabilities are 192 percent of total revenues. As of 2019, Martinsburg’s police and firefighters’ plans had funded ratios of 19.47 percent and 7.68 percent, respectively. The latest actuarial analysis projected that the police plan’s assets would be exhausted in 2037 and that the firefighters’ plan would run out of funds in 2032. At that point, benefits would be financed on a pay-as-you-go basis, but, like Charleston, Martinsburg’s pension contributions are being supplemented by state insurance premium tax proceeds.

If Martinsburg can maintain its revenue base, it should be able to shoulder pay-as-you-go payments. In 2019, the two public safety benefit systems made $2,701,753 in benefit payments. If these pension expenses are added to the $492,373 payment Martinsburg made to the multiemployer West Virginia Public Employees Retirement System, these pension expenses amount to only 8 percent of total revenue, a proportion well below that experienced by cities with the highest pension cost burdens. If state premium proceeds of $794,160 are netted out, the theoretical city contribution falls to 6 percent.

By contrast, Charleston’s pension contributions totaled 11 percent of government-wide revenue in 2019, although that total would have been 14 percent if the city had been obligated to cover the $3,530,843 contributed by the state from insurance premium tax proceeds. The city also contributed $7,284,299 to its pay-as-you-go other postemployment benefit (OPEB) plan, so its overall retirement cost burden totals over one-sixth of total revenue.

Alton, Illinois, and Other St. Louis Suburbs

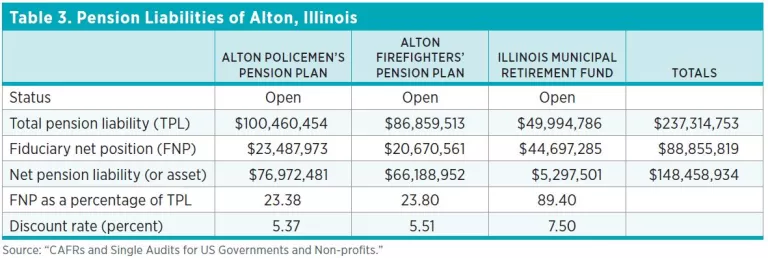

The third-highest net pension liability-to-revenue ratio belongs to Alton, Illinois, a suburb of St. Louis. Net pension liabilities in Alton totaled 298 percent of government-wide revenues at the end of FY 2019. Their breakdown is shown in table 3.

While the two public safety plans have very low funded ratios (when calculated according to GASB methods), the ratios have stabilized in recent years. The policemen’s FNP was 20.96 percent in 2016, the first year the GASB required plans to calculate this measure. It improved slightly, to 23.38 percent, in 2019. Similarly, the firefighters’ funded ratio grew from 19.08 percent in 2016 to 23.80 percent in 2019. These funded ratio improvements were partially attributable to a slight uptick in the blended discount rates used for each system.

Unlike Riverdale, Alton has been making pension contributions close to those actuarially determined. Over the four fiscal years ending March 31, 2019, the city contributed a total of $25,716,703, which is $309,312 more than the actuarially determined amount.

To further reduce its pension debt, Alton sold its municipal sewer and wastewater processing system to Illinois American Water in June 2019 for $53.8 million. Since Alton’s most recently available audited financial statements are for the fiscal year ending March 31, 2019, I do not have documentation that shows how much of the sales proceeds were applied to the two public safety pension plans.

Two other St. Louis suburbs had net pension liability-to-revenue ratios exceeding 200 percent: East Alton and Granite City.

Lincoln Park, Michigan

Of the Michigan cities in the sample, Lincoln Park had the highest net pension liability-to-revenue ratio. The city’s $91,840,059 pension debt was 233 percent of government-wide revenue in 2019. The debt breaks down as shown in table 4.

The MERS unfunded pension liability has continued to grow despite a reform implemented in 2004. At that time, new hires began participating in a defined contribution plan while being eligible for a more modest defined benefit pension. Earlier hires were eligible for 2.5 percent of final average salary multiplied by their number of years of service. Post-2004 hires are eligible for 1.0 percent of final average salary multiplied by their number of years of service, but the city also contributes 7 percent of their salary to a defined contribution plan.

The benefits of the 2004 reform were offset by poor investment performance. According to historical city CAFRs, the plan’s assets declined from $17,047,068 in 2007 to $10,915,398 in 2009 and have not recovered since.

Lincoln Park’s Police Officers and Firefighters Retirement System also suffered large investment losses between 2007 and 2009. Unlike general employees, safety employees continue to accrue all their benefits through the defined benefit plan. However, accrual rates were lowered for both new and existing employees. Before 2013, police and firefighters received 2.8 percent per year of final compensation per year of service. By 2015, this rate had been lowered to 2.0 percent for both new and existing employees, although certain older sworn employees could still accrue benefits at a 2.5 percent rate.

One unusual aspect of the city’s pension system is its unfunded supplemental benefit plan. This plan was created as part of a reform of Lincoln Park’s OPEB plan. In 2014, Governor Rick Snyder declared a fiscal emergency in Lincoln Park, placing its finances under the control of an appointed emergency manager.

The city was paying full health benefits for all police and firefighter retirees as well as for general employees who retired before 2005. In FY 2015, Lincoln Park had unfunded OPEB liabilities of over $110 million and paid $4.4 million in retiree healthcare benefits, more than 11 percent of government-wide revenue.

The emergency financial manager terminated the city’s OPEB plan in 2015, replacing it with a monthly stipend ranging from $150 to $425 for current retirees—and nothing for future retirees. The state treasurer approved this measure, and, under Michigan law, emergency financial managers are accountable to the treasurer rather than to local elected officials. Retirees sued the emergency manager, the state treasurer, and various others, claiming that the action violated the US Constitution’s Contracts Clause, Due Process Clause, and Takings Clause. In 2017 the US Court of Appeals ruled in favor of the defendants, allowing the OPEB plan termination to stand. The court ruled that the plaintiffs should have sued the city, rather than the third parties against which they filed suit.

After further litigation, retirees reached a settlement with the city. Lincoln Park now offers retirees an enhanced OPEB benefit of between $400 and $800 monthly. Retired employees can either apply the benefit amount as a credit against their monthly insurance premiums in the city’s health plan or take it as a cash payment. In the latter case, the payment is considered a supplemental pension benefit, even though it is intended as a retiree healthcare subsidy. Although this change has added $6.4 million to the city’s net pension liability, Lincoln Park’s net OPEB liability is only $10.6 million, a small fraction of its level in 2015. Further, because the retiree health benefit is no longer available to new retirees, these liabilities should diminish over time.

The city’s sizable retirement liabilities are a source of budgetary pressure. According to Lincoln Park’s 2020–2021 budget, pension and OPEB costs are expected to account for 37 percent of general fund expenditures. Owing to the OPEB reform discussed earlier, the great majority of these retirement expenditures are pension related.

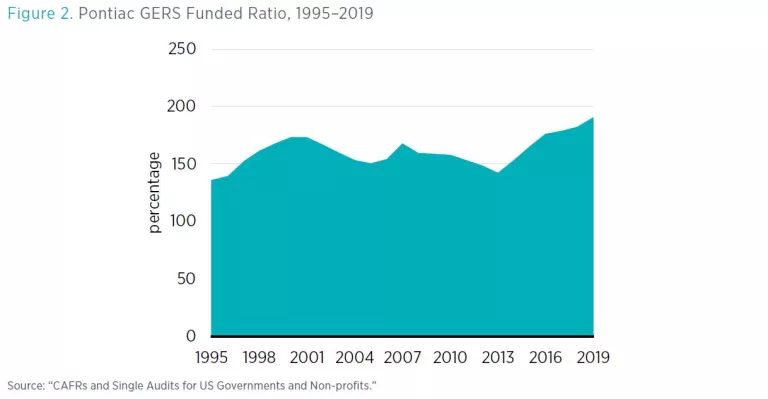

Pontiac, Michigan

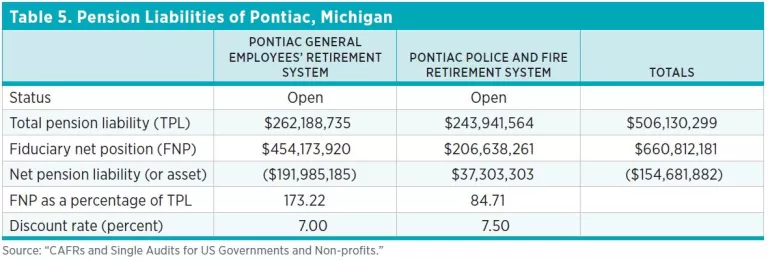

Of the cities I have reviewed, Pontiac had the strongest pension financial position in FY 2019. Its net pension asset position of $154,681,882 was 269 percent of annual revenue. The city has two pension systems, as detailed in table 5.

Pontiac was fortunate to have a strong general employee pension plan, because other aspects of the city’s finances have been troubled. In 2008, a review team recommended that Governor Jennifer Granholm declare a financial emergency in Pontiac owing to general fund deficits, cash management issues, and poor budgeting practices, an action she took the following year. The emergency was not lifted until 2017. As the city now struggles with COVD-19-related revenue losses, it will at least not have to worry about pension funding.

Conclusion

Riverdale and Lincoln Park are examples of municipalities that are struggling with deeply underfunded pension systems. Alton and Charleston were also facing high levels of pension debt in 2019 but appear to have solutions: an asset sale for Alton and state intervention for Charleston. Pontiac illustrates how a well-funded pension system eases fiscal distress but does not guarantee solvency.

Pension debt is only one dimension of a local government’s overall fiscal well-being and is rarely the sole driver of financial health. Unfunded retiree health obligations, bonded indebtedness, cash reserves (especially in a government’s general fund), and revenue trends are also key factors. If a government realizes rapidly increasing revenue, it can resolve large debt burdens without taking extreme actions: it can simply grow its way out of the problem.

On the other hand, governments with stagnant or declining revenue are most at risk. Today, the COVID-19 pandemic is forcing down revenues for governments across the country, but it is doing so unevenly. Counties and municipalities with high dependence on sales taxes and tourism-related revenues face more revenue pressure than those that rely primarily on property taxes—unless, of course, property tax delinquencies are a concern, as was the case in Riverdale.

It is also worth recognizing that pension debt and revenue declines do not immediately spell bankruptcy. Some governments may choose to further deplete their pension assets to make payments during this period of economic distress. By doing so, they may avoid bankruptcy this time around but leave themselves more vulnerable during the next downturn.

Like any single indicator, the net pension liability-to-revenue ratio cannot show which communities are facing a trip to bankruptcy court in the near term. But those near the top of the distribution (e.g., cities and counties with ratios greater than 100 percent) are at increased risk and should urgently consider their options.