- | Housing Housing

- | Policy Briefs Policy Briefs

- |

GASB 67 and GASB 68: What the New Accounting Standards Mean for Public Pension Reporting

The Government Accounting Standards Board (GASB) is a private, nongovernmental body that is charged with setting accounting guidance for state and local governments. Since its establishment in 1984, GASB has issued 86 statements to enhance the transparency, accountability, and clarity of state and local financial reporting. GASB’s goal is to ensure that financial information regarding the status and use of public funds is useful to decision makers and the general public. Changes in government financial practices, the emergence of new financial instruments, and choices of programs or policies often require GASB to update previous statements to reflect new accounting and financial realities.

In 2012 GASB updated its guidance for the reporting and measurement of public pension plan data, and in fiscal year (FY) 2015, state and local governments began to adopt the new standards, known as GASB 67 and GASB 68, in their comprehensive annual financial reports (CAFRs). The new standards were released in response to criticism that the previous standards, GASB 25 and GASB 27, did not fully measure or report plan liabilities and generated misleading information.

In particular, three major critiques had emerged. First, governments were permitted to engage in “asset smoothing,” or averaging the performance of pension investments over a five-year period to smooth out swings in market performance and thus smooth out annual contributions to the plan. Second, pension liabilities were measured with reference to the expected performance of investment portfolios, rather than based on their nearest equivalent in value—government bonds—thus understating the full value of pension liabilities. Last, governments did not report unfunded pension liabilities on the CAFR balance sheet, but instead reported the deficiency in funding since 1997, thus providing an inaccurate picture of governments’ true financial position.

The new guidance produced its desired effect, in part: state and local governments are now required to report unfunded pension liabilities on their balance sheets, producing a more complete picture of the state and local governments’ financial health. But the new guidance is not without problems. To begin with, discount rate selection is guided by subjective criteria resulting in inconsistent measurement. While asset smoothing—which was permitted in the previous standards—has been replaced with the more accurate market value of assets, the new standards permit states to incorporate asset smoothing in reporting pension expenses and net positions. So, while GASB 67 and 68 improve financial transparency by requiring fuller pension reporting in government financials, what is being reported still falls short of accuracy in measurement. GASB should improve the current guidance to reflect economic measurement of risk and eliminate the use of deferrals and delayed reporting.

Unfunded pension liabilities are now reported on the government balance sheets, producing a more accurate picture of government finances and increasing the visibility and the total amount of liabilities on the books. However, the new guidance allows for a subjective application of key measurement assumptions regarding pension liabilities and for the continuance of a form of asset smoothing. The net effect of these guidelines on asset and liability measurement is to dampen the full value of unfunded pension liabilities. These changes are, in effect, at cross-purposes with the effort to make financial reporting more transparent. A review of 144 public pension plans contained in 34 state CAFRs for FY 2014 reveals considerable variation in how the new guidance is applied by governments. In this paper we review each of the standards and consider their effects on state and local financial reporting.

GASB 67

GASB 67 concerns how state and local governments measure pension assets and liabilities. One important change to the previous standards relates to “asset smoothing.” Previously, GASB 25 permitted actuaries to smooth market fluctuations in asset returns, producing an “actuarial value of assets” based on a multiyear average of market values. Asset smoothing helps even out investment swings and give plan sponsors predictability in annual contributions, though it also has the effect of masking the volatility of pension asset portfolios. GASB 67 requires plans to report the actual value, or market value, of assets.

We observed in our review of 144 plans for FY 2014 that using market values rather than smoothed asset values presented a more accurate reporting of the true value of pension assets. Total asset values for the 144 plans were 7 percent higher on a market basis than if reported under asset smoothing. GASB 25, which permits asset smoothing and the calculation of an actuarial value of assets, reported total asset values as $1.46 trillion, and GASB 67, which eliminates asset smoothing and reports the market value of assets, reported total asset values as $1.56 trillion.

GASB 67 also provides new guidance on how plans should select a discount rate to value pension liabilities. Previously, GASB 25 permitted governments to value plan liabilities using a discount rate based on the expected return on plan assets. On average, states expect plan assets will return 7.52 percent annually. This rate of return reflects the return on a higher-risk portfolio consisting of a mix of equities, fixed incomes, and alternatives. Some economists believe this approach runs counter to economic theory, which suggests that a guaranteed liability, such as a legally guaranteed pension benefit, should be valued with reference to its closest equivalent in value—such as the low-risk return on bonds.

GASB 67 attempts to incorporate this concept of valuing pension liabilities with reference to low-risk bonds by suggesting that plans “split the difference.” GASB 67 advises plans to value the funded portion of the liability based on the higher-risk discount rate and value any unfunded portion of the liability based on the low-risk return on tax-exempt municipal bonds. This new “blended rate” approach was expected to lead deeply underfunded plans to report higher unfunded liabilities and lower funding ratios since they would be required to apply a lower discount rate to a much larger portion of the plan’s liabilities.

Early analysis of the effects of the new guidance expected that plan liabilities would increase and funding ratios would decrease. Economist Alicia Munnell and her coauthors modeled 126 plans using FY 2010 data. They projected that GASB 67 and 68 would likely cause plan funding ratios to drop from 77 percent to 63 percent. Professors of accounting John Mortimer and Lisa Henderson projected funding and liabilities for 48 plans using FY 2010 data and estimated that, under the new GASB standards, plans with lower funding ratios under the old guidance would run out of assets more quickly, forcing them to apply the lower blended rate to a greater portion of the liability. Overall, they found that the implementation of GASB 67 and 68 should have increased reported net pension liabilities by $9.2 billion and decreased funding ratios by 17.2 percent.

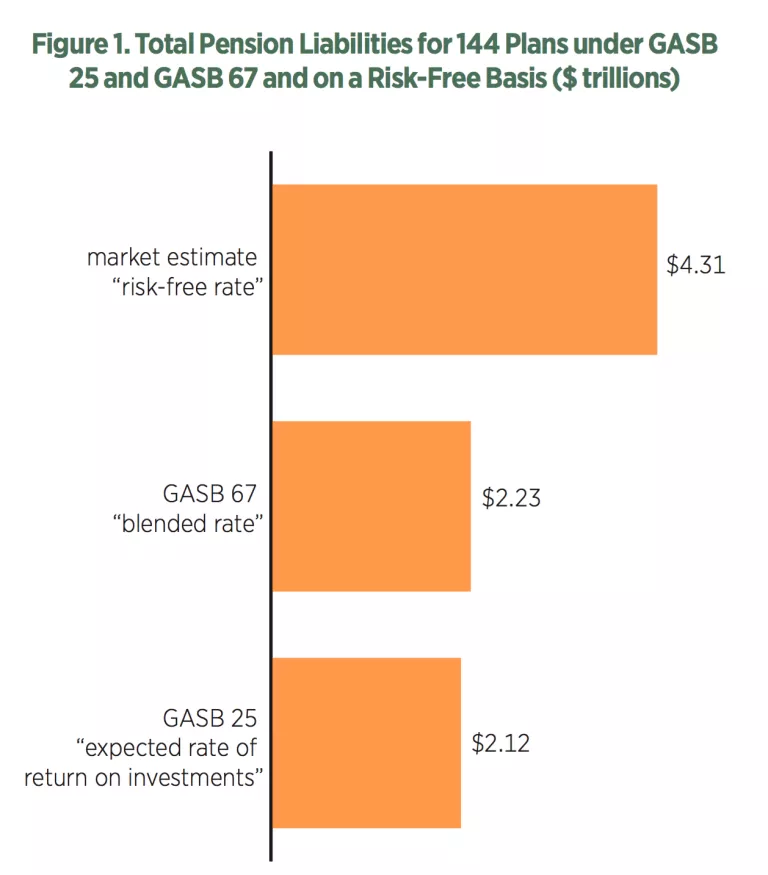

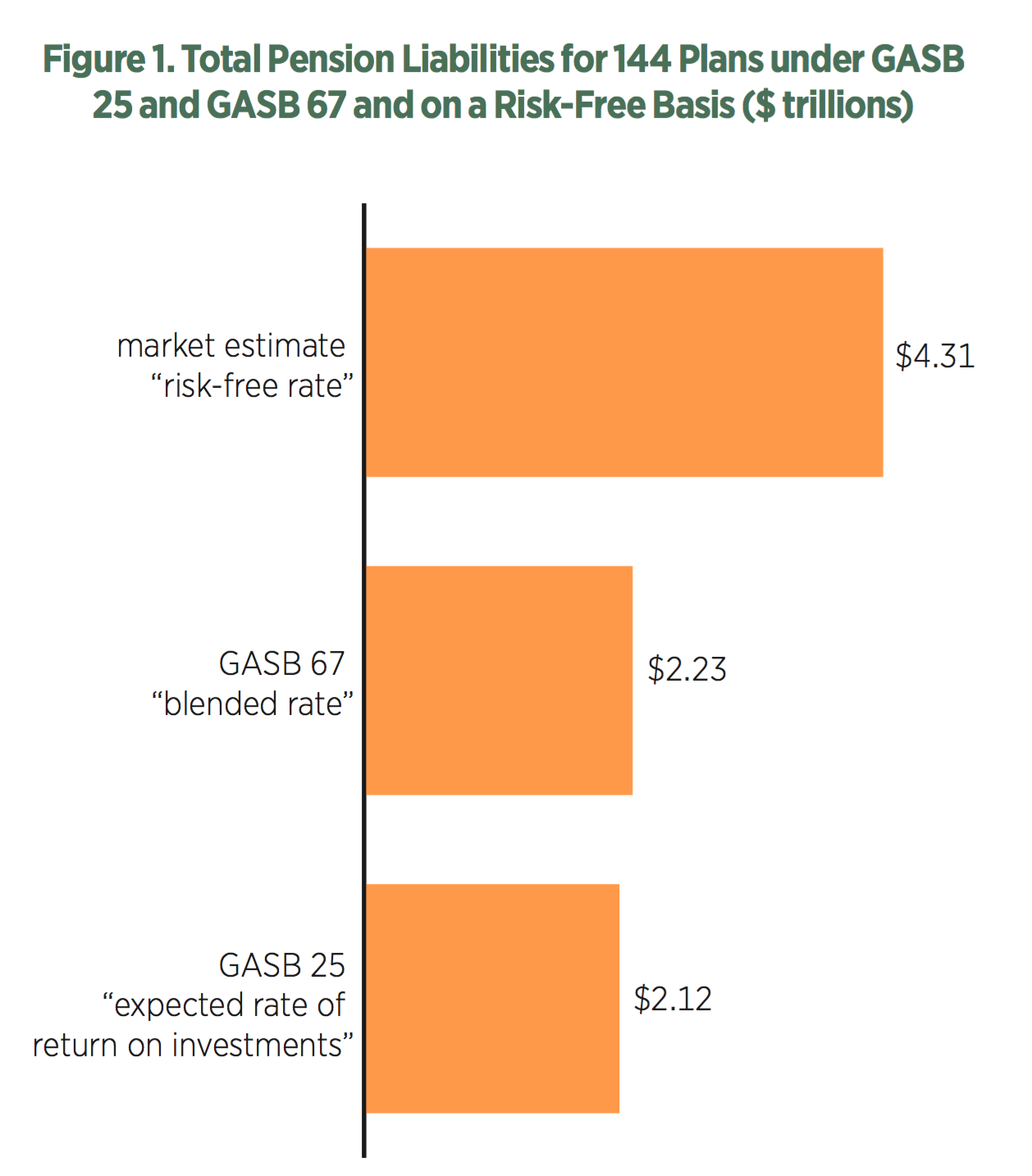

To assess whether the anticipated effects of GASB 67 were realized during its implementation, we reviewed 144 plans for FY 2014. We found that, contrary to expectations, the total pension liability was only 5 percent higher than previously reported liabilities, far less than projections estimated.

Under GASB 25, the total pension liability for these plans is $2.12 trillion. When applying the blended rate under GASB 67, the total liability rises slightly, to $2.23 trillion. The reason for this is that the vast majority of plan actuaries projected no portion of the liability would be unfunded, because the plans would not run out of assets. Therefore, the calculation of plan liabilities is based on the higher discount rate. Only 13 of the 144 plans applied the blended rate. These include all of New Jersey’s pension plans, the Kentucky Teachers’ Retirement System, Illinois State Employees’ Retirement System, Illinois State Universities Retirement System, and several smaller plans for Arizona elected officials, Colorado judges, and Rhode Island judges.

There was considerable variance in how the states applied the new standards:

- In New Jersey, actuaries projected an earlier run-out date for plan assets, resulting in the fullest use of the blended rate out of all state plans. As a result, New Jersey’s pension liability increased by 107 percent owing to the application of the new standard. By contrast, other state plans with significant unfunded liabilities did not apply the more conservative blended rate, but continued to use more generous assumptions.

- In Kentucky, Employees Retirement System actuaries projected that the system would not run out of assets, based on the state legislature’s commitment to fund the plan in full beginning in 2015. Thus, actuaries applied the higher discount rate assumption of 7.75 percent to measure its pension liabilities, thereby understating the true unfunded liability.

- Similarly, in California, upon the enactment of AB 1469—in which the state planned to provide additional funding to the State Teachers’ Retirement System—actuaries changed their projections to indicate that assets would not run out, thereby eliminating the need for the plan to apply a blended rate.

- In Illinois, despite the state’s poor history of funding its plans and its significant funding shortfalls, actuaries did not apply the blended rate to the Teachers’ Retirement System. Actuaries did not apply the low-risk rate to the State Employees’ Retirement System and the State Universities Retirement System until 2065, based on the assumption that the plans would not run out of assets until that date.

This early analysis of the application of GASB 67 indicates that plans have significant discretion in how and when to apply the blended discount rate, leading to subjective and inconsistent outcomes. Mortimer and Henderson noted the possibility that, because of the design of GASB 67 and 68, plans would produce optimistic estimates of plan funding. Our analysis confirms this supposition. As long as interest rates remain low, plans in the worst condition have the incentive to inflate the discount rate assumption to make plan liabilities appear small.

Figure 1 shows the difference in the three approaches to measuring pension liabilities, which are calculated based on GASB 25 and GASB 67 and on a guaranteed or risk-free basis as economic theory suggests. When using the risk-free rate—that is, the yield on notional 15-year Treasury bonds of 2.59 percent—the total liability for these 144 plans is $4.31 trillion.

GASB 68

GASB 68 pertains to how governments that sponsor pension plans report pension data in their CAFRs. Until 2014, state and local governments followed GASB 27 in disclosing pension information in the statement of net position. Under this guidance, governments reported the annual required contribution (ARC) to the pension plan or plans as the “net pension expense” and the difference between the ARC and the actual contribution as the “net pension obligation.” The ARC consists of two pieces: (1) the normal cost for pension benefits earned in the current year and (2) the amortization payment, which is a catch-up payment for costs associated with any unfunded liability over the past 30 years.

In effect, this information provided a measure of how much a government contributed to fund the plan annually. If the government fell short of its annual required payment, it would recognize a “net pension obligation.” These accounting terms did not reveal the full liability, only the cumulative deficiency in annual payments since 1997. The result is that states with large unfunded pension liabilities could report a zero net pension obligation if the annual payments to the plan were made in full that year.

In FY 2015, state governments implemented GASB 68 and reported the unfunded pension liability on the balance sheet of the CAFR. State-reported pension debt increased from $80 billion to $537 billion. The increase in total liabilities had the effect of lowering states’ overall net positions by 29 percent, from $1.3 trillion to $956 billion. The effect of GASB 68 is that governments now recognize unfunded pension obligations when measuring their overall fiscal position. This is a marked improvement for financial transparency and accuracy.

Despite this big improvement, the standard also permits practices that produce other types of distortions. GASB 68 permits plans to report pension liability data from the end of the previous fiscal year in order to allow governments to complete their CAFRs without a delay. This time lag, while it may appear benign, can produce distortions over time, especially considering that pension liabilities often constitute the largest single liability for many governments.

While GASB 67 eliminated the practice of asset smoothing in the reporting of pension assets, GASB 68 permits governments to continue a form of it. Governments are permitted to defer the recognition of the difference between the return expected on plan assets and the actual return. This “deferred inflow of resources” occurs over a five-year period. In effect, the deferred inflow of resources is the equivalent of asset smoothing which permits the sponsor to gradually incorporate any changes to the market value of assets that differ from the expected value of assets over time. The consequences of the practice remain the same. Market declines and gains are only gradually recognized, likely increasing the riskiness of sponsor behavior.

Policy Recommendations

GASB 67 and 68 are an attempt to improve the previous guidance governing state and local government pension reporting. While the updated standards sought to increase transparency, some problems with measurement remain. Further changes would go a long way in making government reporting more transparent and accurate. Among the most apparent changes prompted by our empirical findings are that GASB should

- reassess the application of the blended rate in light of economic theory and the intent of the new rule;

- require governments to wait until current pension numbers are available so that they will produce accurate balance sheets; and

- eliminate the use of measurement deferrals, which are a form of asset smoothing.

Conclusion

The implementation of GASB 67 and 68 was intended to improve the accuracy and transparency of pension reporting for US public sector plans. To date, the standards have had a mixed effect. State and local governments are now required to report the unfunded pension liability as part of their overall fiscal position, providing a more accurate assessment of fiscal health. The underlying assumptions used to measure pension obligations continue to need improvement. When measuring the government’s unfunded pension liability, asset smoothing has been replaced with the more accurate use of market values. However, the use of confusing deferrals allows governments to continue to conceal the total effect of market fluctuations from their net positions. The application of a blended discount rate to plan liabilities hinges on projections of when plans are likely to run out of assets, which is very subjective.

The first year of implementation suggests that actuaries are making optimistic assumptions. Plans that are currently distressed project solvency far into the future. In the cases of California and Kentucky, actuaries may assume that plans will be well funded on the basis of legislative intent to fund rather than actual assets and past funding behavior. These findings indicate that a reform of the new guidance is needed to ensure the proper measurement and funding of public sector pension plans.

{kind=link}