- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

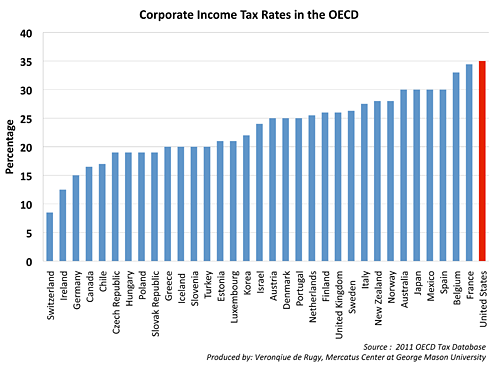

Corporate Income Tax Rates in the OECD

In this chart, Veronique de Rugy shows that in the United States, the corporate income tax raises little revenue compared with other federal taxes - roughly 11.6% of total federal tax revenues.

This week, Mercatus Center Senior Research Fellow Veronique de Rugy charts corporate income tax rates – the United States has the highest national statutory corporate tax rate in the OECD.

In 2011, national statutory corporate tax rates among the thirty-four members of the OECD will range from 8.5 percent in Switzerland to 35 percent in the United States. When sub-national taxes are added, the United States has the second-highest statutory combined corporate tax rate – 39.2 percent – after Japan’s rate of 39.5 percent.

Despite having the highest national statutory rate, the United States raises less revenue from its corporate tax than do the other members of the OECD on average. In fact, federal corporate income taxes raise little revenue compared with other federal taxes; roughly comprising 11.6% of total federal tax revenues.

Corporations, like individuals, can and do use tax breaks to lower their tax burdens and, as a result, the effective tax rate is lower than the top rate.

However, these breaks shouldn’t be looked at independently of the corporate tax system. The United States not only imposes high rates, but it also taxes corporations on a worldwide basis: profits made by an American-owned computer plant are subject to American taxes whether the plant is located in Texas or Ireland. In contrast, most major countries do not tax foreign business income. In fact, about half of OECD nations have “territorial” systems that tax firms only on their domestic income.

The combination of high rates, worldwide taxation and a competitive global marketplace makes our corporate tax system extremely punishing.

Veronique de Rugy explains why our corporate tax system is particularly inefficient at The Corner.