- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

Falling Deficits Don’t Mean It’s Time to Increase Spending

If current laws stay in place, spending for Social Security and the major health-care programs, including Medicare, Medicaid, and the Affordable Care Act, will grow faster than the economy. As a rule of thumb, a government’s spending should never grow faster than the economy that’s supposed to pay for it. (It’s worth noting that the CBO lowered its projection of economic growth going forward.) All of this suggests that, rather than celebrating a short-term respite from $1 trillion deficits, we should be even more concerned about reining in the size and scope of the federal government.

The Congressional Budget Office’s latest budget projections and economic outlook for the next 10 years puts the budget deficit for the current fiscal year (2015) at $468 billion, down from $483 billion in fiscal year 2014. These figures are considerably smaller than the $1 trillion deficits that the federal government ran from fiscal years 2009 to 2012. Advocates for higher federal spending cite the CBO’s relatively lighter deficit as warrant for opening up Washington’s spending spigot. In fact, the CBO outlook makes the opposite case—because these lower deficits won’t last.

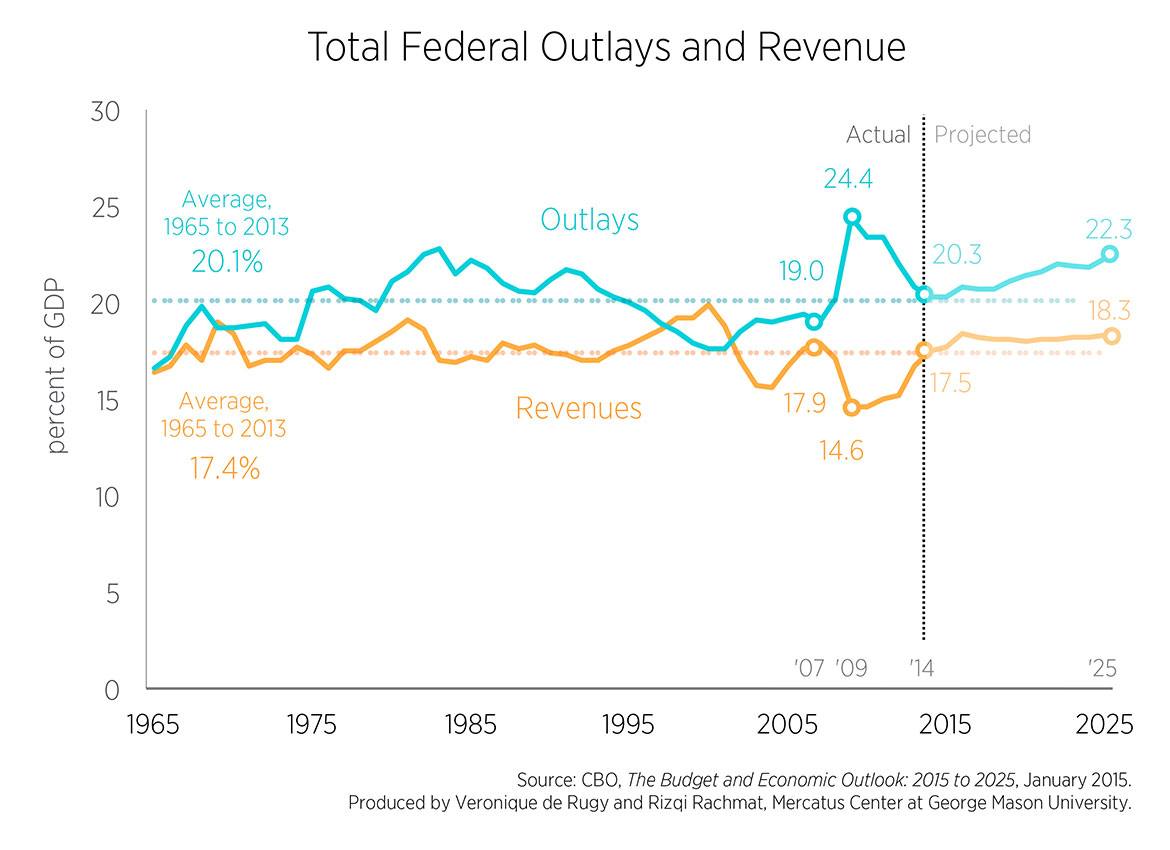

The CBO projects the deficit to begin rising again in fiscal year 2017 and to surpass $1 trillion in fiscal year 2025. This growth in future deficits is the result of a jump in entitlement spending rather than a one-time increase in spending (as it was in fiscal years 2008 and 2009). Deficits will keep growing unless the underlying causes are addressed. As the following chart illustrates, addressing the underlying causes does not mean increasing taxes to offset increased spending.

The dotted lines show the historical averages since 1965 for federal spending and revenues as a share of the economy (as measured by the gross domestic product, GDP). Currently, federal spending and revenues as a share of GDP are at those averages. The CBO projections show that both spending and revenues would rise significantly above the averages. Of particular concern, spending as a share of GDP would rise from 20.3 percent today to 22.3 percent in fiscal year 2025.

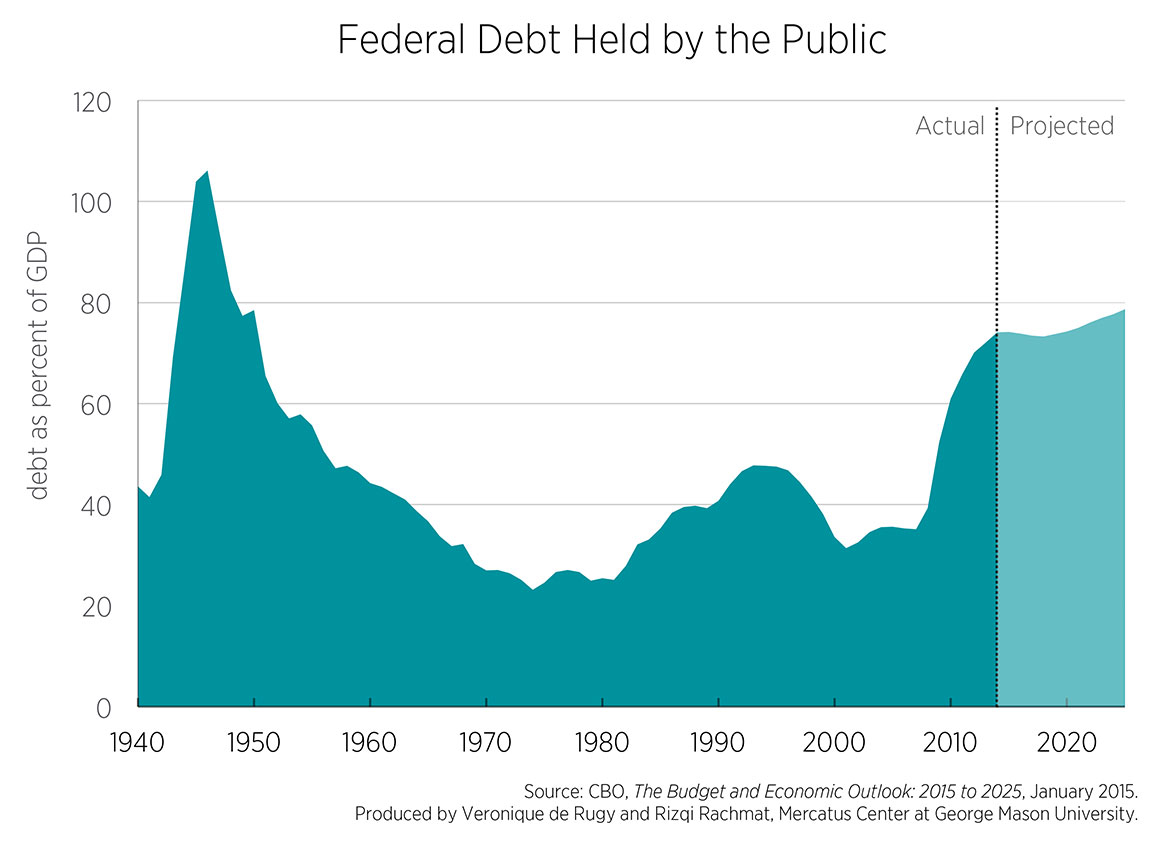

We should also be concerned that, while federal deficits have temporarily receded, federal debt levels are still rising. In fiscal year 2014, debt held by the public was 74.1 percent of GDP; it was 35.1 percent of GDP in fiscal year 2007. As the following chart shows, the CBO projects that debt will go from that 74.1 percent today to 78.7 percent of GDP in fiscal year 2025. The country has not experienced such large, sustained debt levels since the one-time explosion in federal spending to pay for World War II.

Last year, my colleague Jason J. Fichtner and I wrote a short paper entitled “The US Debt Crisis: Far From Solved.” Its findings remain relevant today:

As economists, we’re concerned about the negative consequences of excessive debt. But neither we nor any other economist can identify at what point high debt levels become unacceptable to global credit markets. Nor can we reliably predict what form the resulting fiscal crisis will take. It could mean an inexorable deterioration of the US economy. Or it could be more abrupt, with creditors losing faith and pulling their funds from the United States overnight, throwing the country into a vicious debt spiral, another deep recession, and ultimately a lower standard of living here and around the world.

This outcome is not inevitable, but it grows dangerously more likely as policymakers delay taking action. Continued failure to reform the main drivers of current and future spending and debt—principally Medicare, Medicaid, Social Security, and the Affordable Care Act—will eventually force deep and highly destabilizing policy changes. Only by acting soon and maintaining a long-term commitment to controlling spending can policymakers avoid a potentially irreversible decline in Americans’ standard of living.

If current laws stay in place, spending for Social Security and the major health-care programs, including Medicare, Medicaid, and the Affordable Care Act, will grow faster than the economy. As a rule of thumb, a government’s spending should never grow faster than the economy that’s supposed to pay for it. (It’s worth noting that the CBO lowered its projection of economic growth going forward.) All of this suggests that, rather than celebrating a short-term respite from $1 trillion deficits, we should be even more concerned about reining in the size and scope of the federal government.