- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

Social Security Disability Insurance Program Is Financially Unsustainable

It will be tempting for policymakers to avoid the politically difficult decision to rein in benefits by a temporary fix, like raising payroll taxes or shifting “assets” from the regular Social Security trust fund to the DI component. These short-term fixes would worsen the Social Security system’s long-term structural imbalance, while inflicting damage on the US economy.

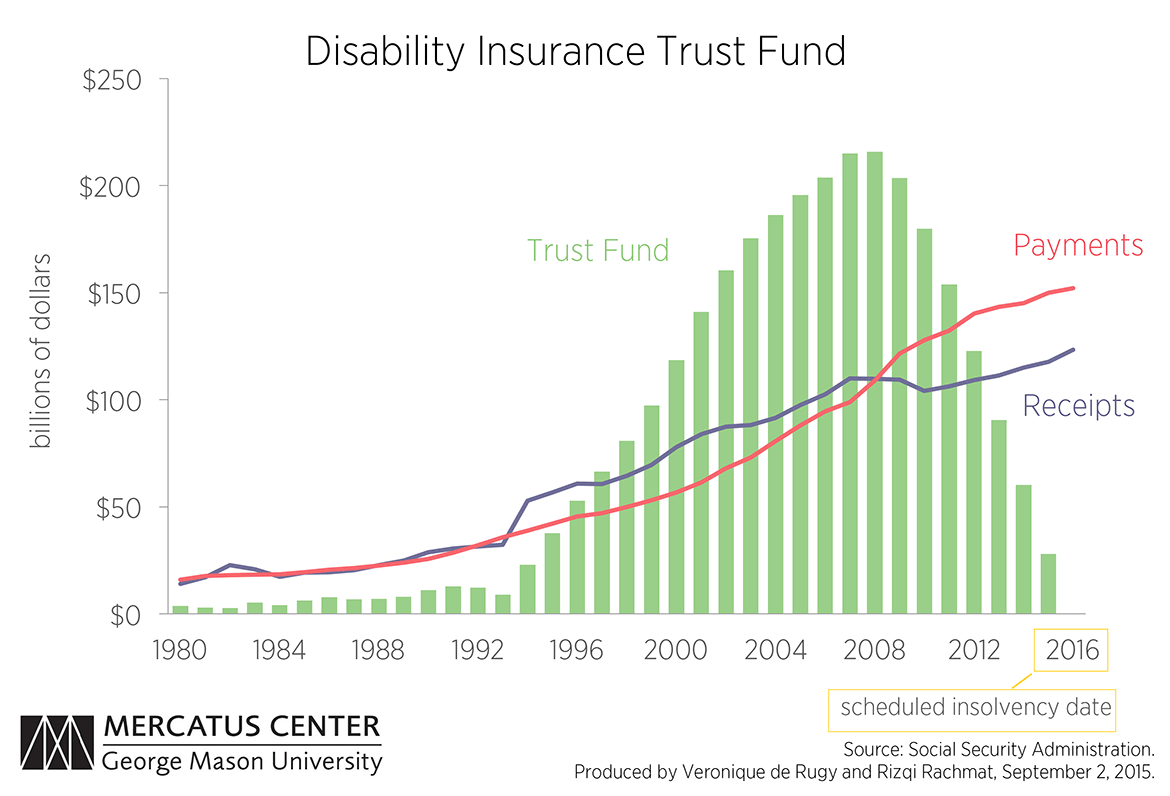

The 2015 annual report from the Social Security Board of Trustees shows that the program’s disability component is in immediate trouble. Data from the latest report show that the disability fund will be depleted as soon as next year and unable to pay full benefits to beneficiaries.

This week’s first chart uses that data to show total income, expenditures, and assets in the Social Security Disability Insurance (DI) trust fund going back to 1980. The chart shows that the trust fund has been operating under deficits since 2009, as shown by the decline in the trust fund (green bars) and ever-growing gap between the payments (red line) and receipts (blue line).

Those deficits have been financed by redeeming nonmarketable government securities that were accumulated over the years when the program was bringing in more revenue than was being paid out. The government spent the surpluses on other government programs and credited the fund with the securities. But because the securities are nonmarketable, the government had to use general federal revenues to “redeem” them once the DI fund started to run deficits in order to cover the difference. With the illusion of the DI trust fund about to disappear, policymakers have no choice but to finally confront the financial imbalance that actually began years ago.

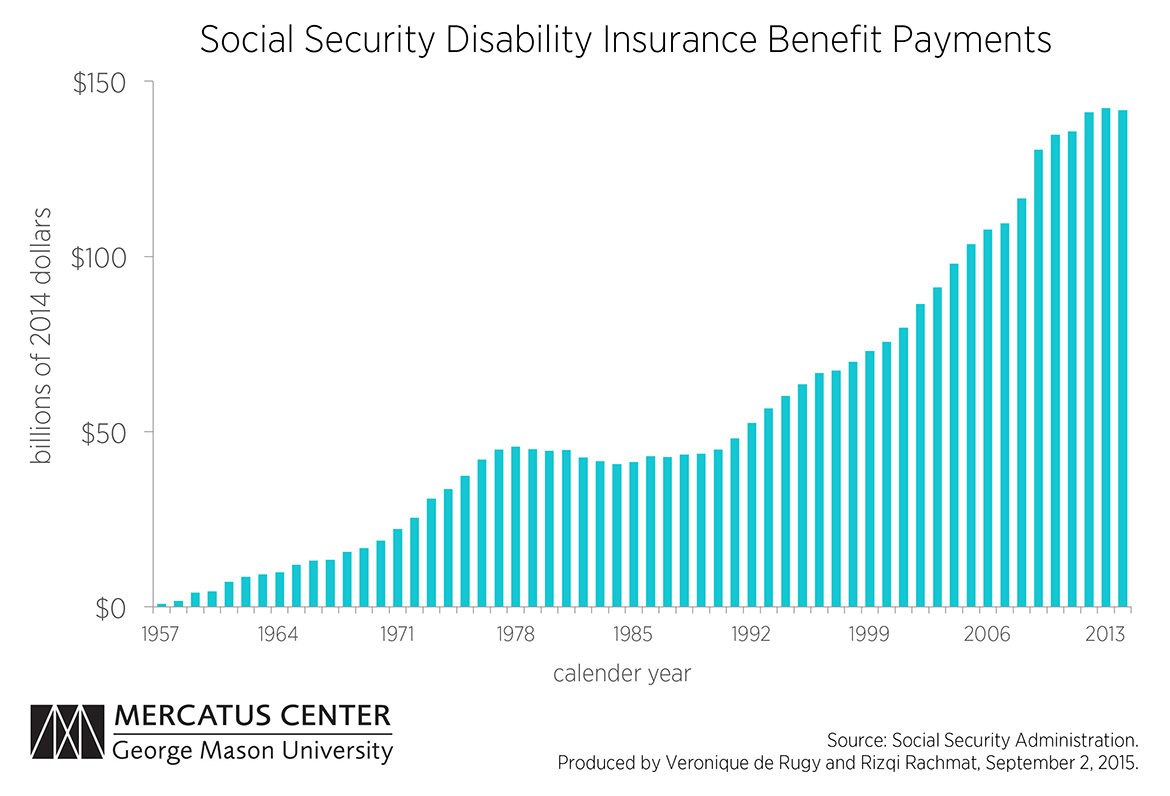

That means confronting the growth in disability benefits, which have exploded over the past decade. The second chart shows the dramatic inflation-adjusted rise in benefits since the program’s inception, which have doubled in real terms (from $70 billion to about $142 billion) between 1998 and 2014.

It will be tempting for policymakers to avoid the politically difficult decision to rein in benefits by a temporary fix, like raising payroll taxes or shifting “assets” from the regular Social Security trust fund to the DI component. These short-term fixes would worsen the Social Security system’s long-term structural imbalance, while inflicting damage on the US economy.