- | Government Spending Government Spending

- | Data Visualizations Data Visualizations

- |

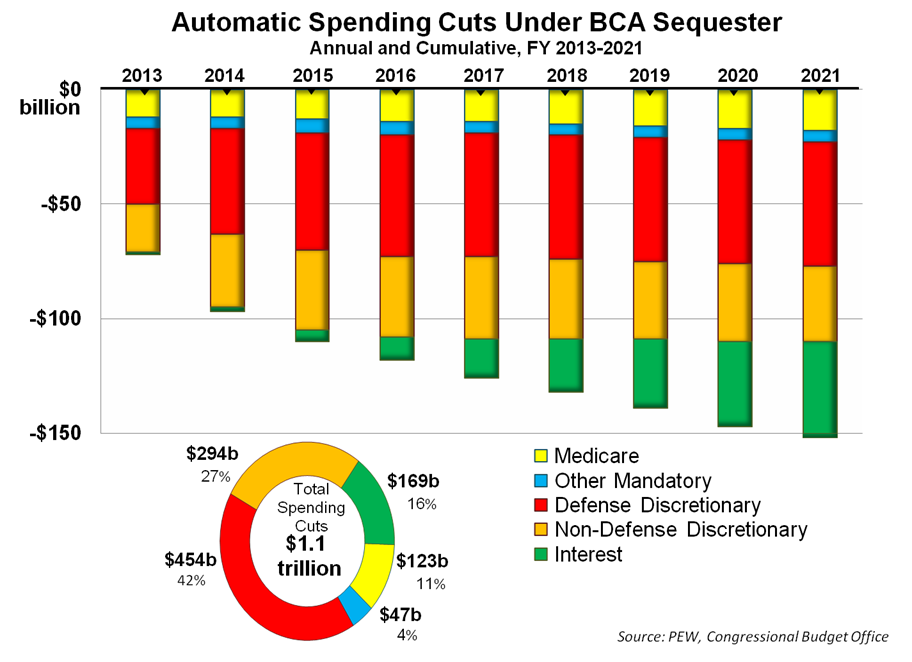

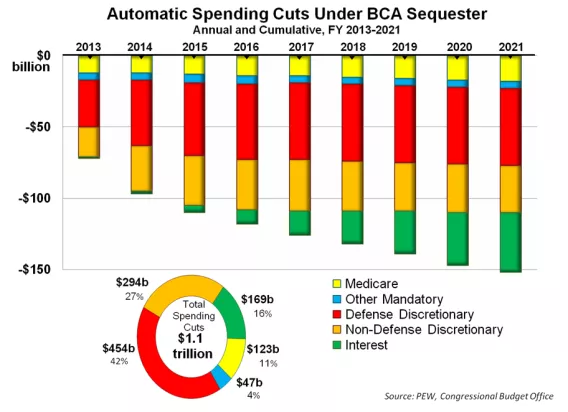

What Happens if the U.S. Super Committee on Deficit Reduction Fails?

This chart examines the annual and cumulative spending cuts under the $1.2 trillion Budget Control Act (BCA) sequester.

This week, Mercatus Center Research Fellow Veronique de Rugy examines the annual and cumulative spending cuts under the $1.2 trillion Budget Control Act (BCA) sequester. Data from the Congressional Budget Office (CBO) and PEW Research estimates the budget cuts in discretionary and mandatory spending that would occur if the automatic enforcement mechanisms were triggered.

With a month to go before its November 23 deadline, the Joint Select Committee on Deficit Reduction (JSC) has left all sides speculating for striking a $1.2 trillion deal. Failure to strike a far-reaching plan will result in automatic cuts.

Under sequestration, an amount of money equal to the difference between the cap set in the Budget Resolution and the amount actually appropriated is “sequestered” by the U.S. Treasury and not handed over to the agencies to which it was originally appropriated by Congress. Since the Gramm-Rudman-Hollings Act of 1985, the number of exempted programs from sequestration has tended to increase. Today, Congress has chosen to exempt certain high-spending programs from the sequestration process: Social Security, veteran’s benefits, Medicaid, the Children’s Health Insurance Program, unemployment insurance, food stamps, and a host of other programs are all exempt from the sequester. Additionally, the cut to Medicare is capped at 2 percent.

As PEW research explains: “The CBO estimates that about 70 percent of mandatory spending would be exempt from sequestration, virtually all of it in non-defense mandatory spending, such as Social Security and Medicaid. Most of Medicare would be limited to a two percent annual cut. About 42 percent of the savings from the automatic sequester, or about $454 billion over the next decade, would fall on defense discretionary spending. Another 42 percent would come from non-defense discretionary and mandatory spending, and the remaining 16 percent would result from lower interest costs.”

Unfortunately, CBO’s analysis can only approximate the ultimate results; the Administration’s Office of Management and Budget would be responsible for implementing any such automatic reductions on the basis of its own estimates. Although significant budgetary savings by sequestration is better than no plan, let us not forget the sole purpose of the JSC, and the many political failures that led up to this.

Veronique de Rugy blogs about "Sequester vs. Surrender" at NRO’s The Corner.